OIL: High Seaborne Oil Levels & Expected OPEC Output Rise Pressure Crude

Oil continued normalising on Tuesday following the 24 October high driven by news of increased US/EU sanctions on Russia. The fall in the Dallas Fed services index pressured prices. The market is refocusing on supply/demand fundamentals with OPEC’s monthly meeting on Sunday and another output increase probable while the IEA revised the expected 2026 market surplus higher in its October report. This is likely to provide a headwind to oil prices for some time.

- WTI fell 1.8% to $60.18/bbl after breaching $60 a number of times but breaks below were brief. It reached a low of $59.76, just above support at $59.64, 23 October low. It is now 2.9% lower in October and almost 4% off Friday’s high.

- Brent was down 1.8% to $64.47/bbl to be 2.4% lower this month. It touched $64.00 after the Dallas Fed data and then settled around $64.50. It held above initial support at $63.86, while the bear trigger is at $60.07. The expiry of contracts around $65 could add to market volatility, according to Bloomberg.

- OPEC increased its output target 137kbd at the last 2 meetings and another one is likely at the 2 November meeting as the group continues to unwind its previous 1.66mbd reduction.

- According to data from Vortexa there are currently 1.4bn barrels of seaborne oil, which the market is concerned will add to inventories. This is the highest since 2016 (Bloomberg).

- Bloomberg reported that US oil inventories fell a larger than expected 4mn barrels last week, after declining the previous week, according to people familiar with the API data, which may support crude when it resumes trading. Gasoline and distillate were both lower down 6.3mn and 4.4mn respectively. The official EIA data is out on Wednesday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

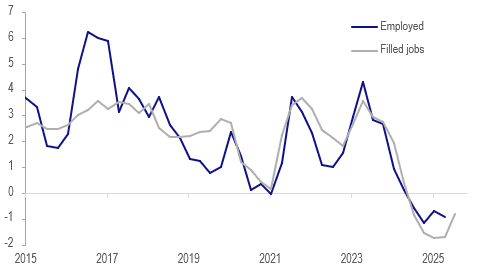

NEW ZEALAND: Labour Market Weak But Turning

August filled jobs rose 0.2% m/m after a downwardly revised flat July. This is the first increase in hiring since January and while the labour market appears to have stabilised conditions remain weak with filled jobs down 0.7% y/y. On a positive note, the August increase was across sectors with the good-producing industries the strongest. The next RBNZ decision is on October 8 and it is expected to ease again but it remains uncertain if it will be by 25bp or 50bp.

- The Q3 average to date filled jobs are up 0.1% q/q, which if sustained would be the first positive after 5 quarterly contractions. September filled jobs are published on 28 October and Q3 labour data on 5 November.

NZ filled jobs vs employment y/y%

Source: MNI - Market News/LSEG/Statistics NZ

- Good-producing industries increased filled jobs by 0.6% m/m in August with the primary sector up 0.2% and services +0.1%. Over the last year construction has been the weakest down 5.1% y/y followed by professional, scientific and technical services -2.7% y/y, while healthcare and education were both up 1.7% y/y.

- The weakness in the jobs market has been concentrated in the under 35s with 15-19 years -8.2% y/y, 20-24 years -3% y/y and 25-29 years -3.5%. Due to this many people have stayed in education.

- Another tentative sign of a stabilisation in the jobs market is the SEEK new job ads index which was up 4.4% y/y in August after contracting since November 2022. The index is at its highest since May 2024.

AUD: AUD/USD - Finds Buyers Towards 0.6500 As The USD Move Stalls

The AUD/USD had a range overnight of 0.6521-0.6552, Asia is trading around 0.6550. US stocks found some support and the USD’s bout of strength stalled as the data on Friday came in as expected. The AUD found some demand back towards the 0.6500 area and is trying to bounce. Price is back in the range and the market will be turning its attention towards Fridays Payroll number if it is released. The AUD outperformance continues to be better expressed in the crosses for the time being.

- MNI RBA WATCH: On Hold, Eyeing Further Labour, CPI Data. The Reserve Bank of Australia board is likely to hold the cash rate at 3.6% tomorrow as it considers the floor of its easing cycle and awaits clearer signals on inflation and labour market tightness, making a November cut a possibility. Former RBA officials argue that a tight labour market, weak productivity, and strong wage growth could limit the Bank to just one or two more cuts, with the risk tilted toward one. They agree labour market performance will be central to the Bank’s next steps.

- Bloomberg - “Trump will meet the top four congressional leaders at the White House Monday as an Oct. 1 shutdown looms. The US will still continue to collect tariff revenue and pursue its immigration crackdown if the government closes.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AUD405m), 0.6625(AUD1.29b), 0.6725(AUD1.19b). Upcoming Close Strikes : 0.6600(AUD943m Oct 1), 0.6600(AUD1.57b Oct 2), 0.6700(AUD1.64b Oct 1) - BBG

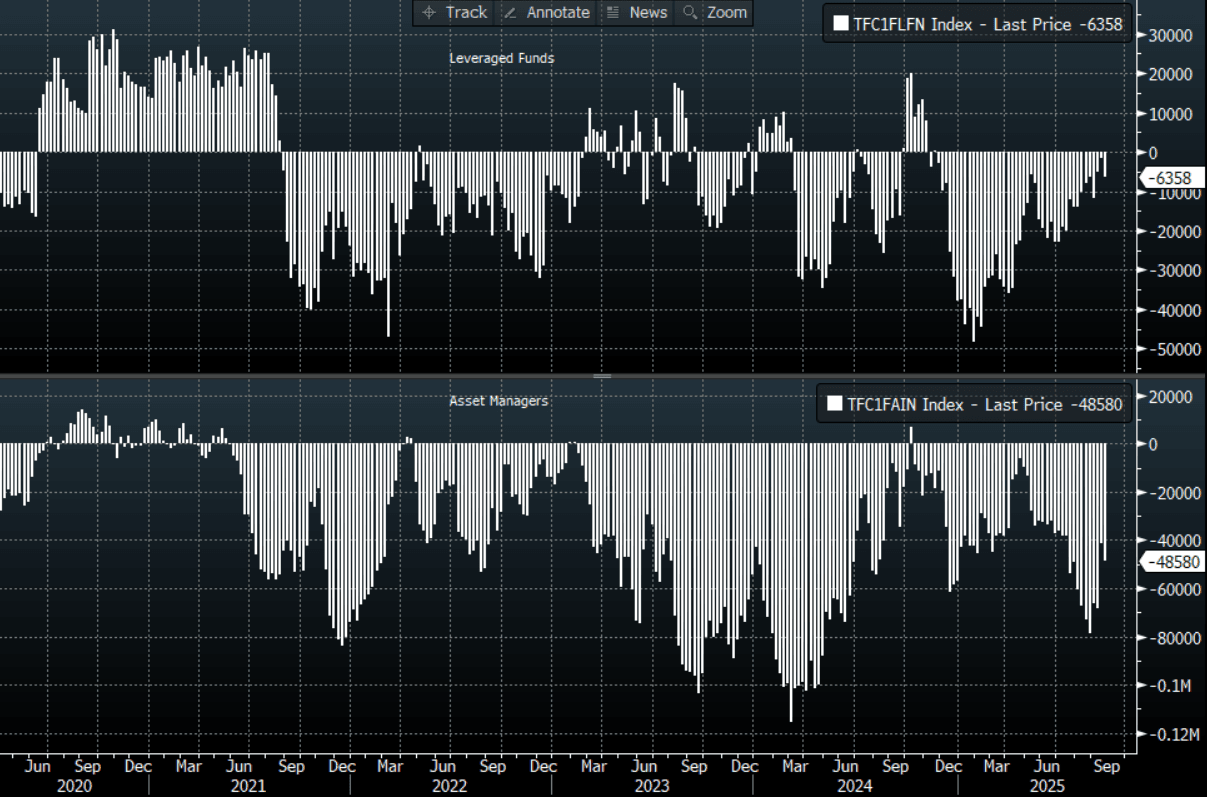

- CFTC Data last week shows Asset managers added back to their recently reduced shorts, -48580(Last -41095). The Leveraged community did likewise, -6358(Last -1519).

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

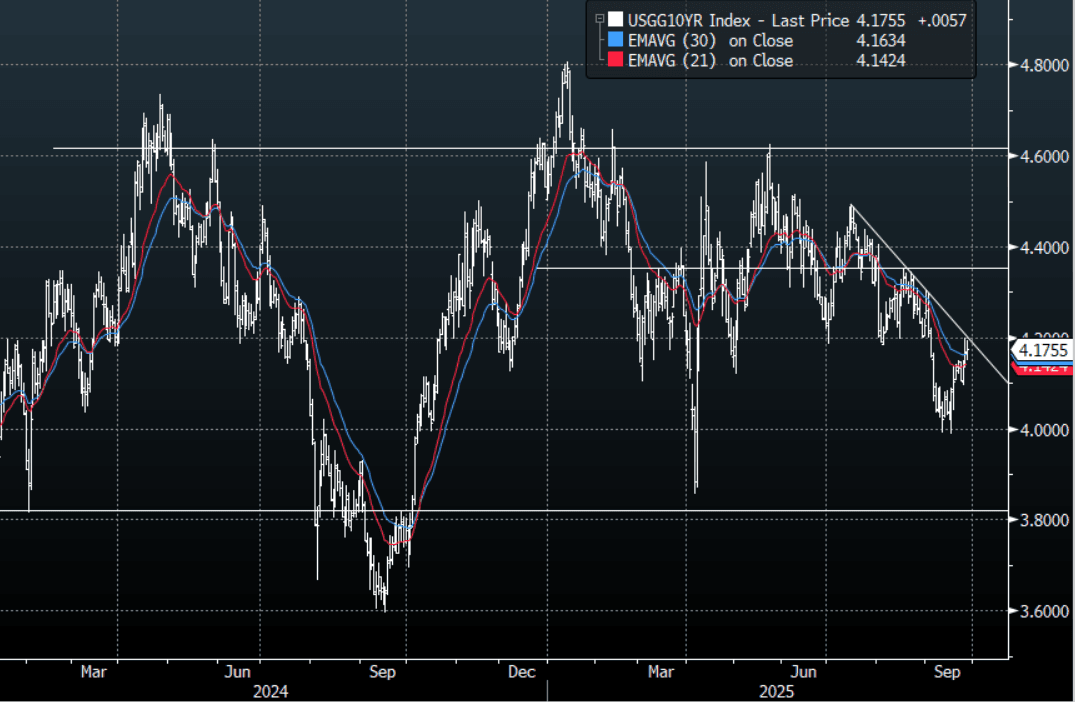

US TSYS: Yields End Mixed, Attention Turns Toward Payroll Data This Week

TYZ5 reopens at 112-10+, up 0-02 from closing levels in today’s Asia-Pac session.

- Friday night the US 10-year yield had a range of 4.1503% - 4.1949%, closing around 4.175%.

- Treasury yields ended mixed on Friday night; (2s10s +1.80 at 53.048, 5s30s -4.55 at 98.616).

- 10-Year yields persisted with its probe of the 4.20% area, I suspect buyers continue to be should be around 4.20% initially and look to fade the move higher. The jobs data if released will be key this week. A move back above 4.35%/4.40% is needed to negate the downtrend.

- MNI FED: Bowman Advocates Fed Take More Forward-Looking Approach.Federal Reserve Governor Miki Bowman on Friday said the Fed should place more emphasis on a proactive forward-looking approach and down-weight the latest data points, repeating that the Fed must act "decisively and proactively" to address increasingly fragile labor market conditions.

- MNI US DATA: Core PCE Inflation Steady In August, Supercore M/M Stays Elevated. August's core PCE reading of 0.227% M/M was basically exactly in line with expectations (0.22% MNI median), and came with a downward revision to July's figure (now 0.235%, was (0.273%). That marks the slowest monthly M/M print in 4 months.

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P