EU REAL ESTATE: Heimstaden (HEIMST: B/B*-): Upsized Guidance

- Guidance: €425m 5NC3 8.5%a (+/- 12.5) wpir

- Books >€925m

- IPT: Min €350m 8.75%a

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: Bund is testing the Immediate support

Bund look to test that immediate area of interest noted at the 2.263% Retracement Yield level and the tiny 134.41 gap, so far printed a 134.42 low and 2.261% high in Yield.

A clear break through the latter, would open to:

- 2.282% = 134.24.

2.300% = 134.04.

Underperformance In Germany has allowed for the Tnotes/Bund spread to trade tighter today, after seeing some interest in Fading off the 218.1bps high level Yesterday, this was the April high and widest print for 2024.

GILT TECHS: (H5) Impulsive Sell-Off Extends

- RES 4: 94.88 20-day EMA

- RES 3: 94.50 High Dec 16

- RES 2: 93.87 Low Dec 16 and gap high on the daily chart

- RES 1: 93.64 High Dec 16 and a gap low on the daily chart

- PRICE: 92.60 @ Close Dec 18

- SUP 1: 92.58 Intraday low

- SUP 2: 92.50 3.500 proj of the Dec 3 - 4 - 5 minor price swing

- SUP 3: 92.38 3.618 proj of the Dec 3 - 4 - 5 minor price swing

- SUP 4: 92.23 3.764 proj of the Dec 3 - 4 - 5 minor price swing

A strong bearish theme in Gilt futures remains in play and this week’s extension reinforces current conditions. The move down has resulted in a breach of key short-term support at 93.40, the Nov 18 low. The break of this level highlights a stronger reversal. Sights are on 92.50, a 3.50 projection of the Dec 3 - 4 - 5 minor price swing. Initial resistance is at 93.64, the Dec 16 high and a gap low on the daily chart.

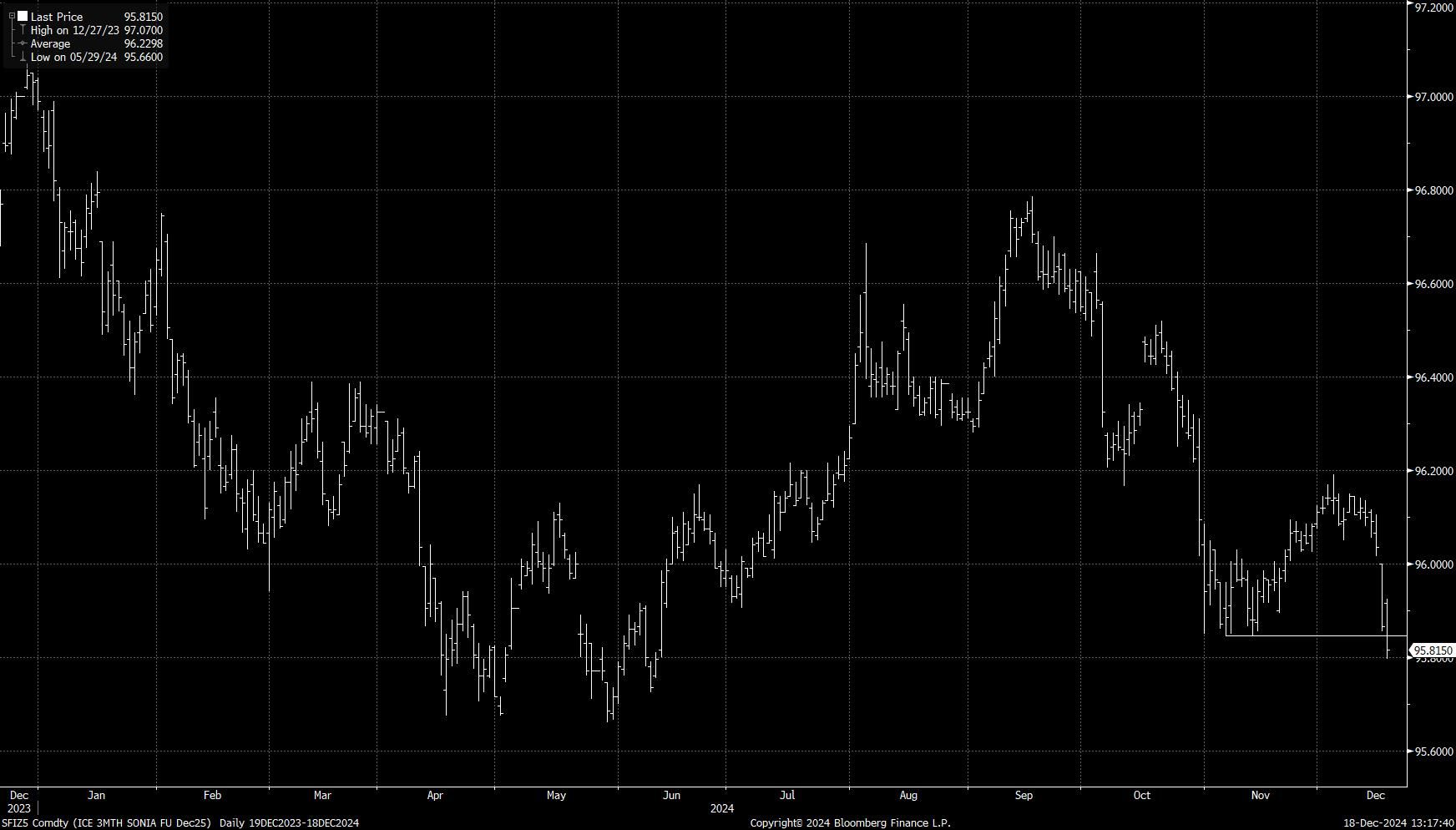

STIR: Only 50bp Of BoE Cuts Now Priced Through ‘25

GBP STIR pricing covering BoE meetings through ’25 has hit a fresh hawkish extreme today.

- December ’25 BoE-dated OIS is now showing only 50bp of cuts (compared to 75bp at Friday’s close), while SFIZ4 has broken the support area formed in November, hitting the lowest level seen since June.

- The market-implied rate cutting path is starting to look a little shallow, with the impact of yesterday’s firmer-than-expected wage data still being felt.

- Our macro team still looks for cuts in February and May. The evolution of data over that period will then give the Bank greater insight on how to proceed and adjust communication.

- Our full preview of tomorrow’s BoE decision can be found here.

Fig. 1: SONIA December '25 (ZH) Futures

Source: MNI - Market News/Bloomberg