CHINA: Headlines from NPC : Issuance May Point to RRR Cut

- As headlines start to trickle out of the NPC, a reduction in growth target is one of the key changes.

- 2025 growth target was 'around 5%' with 2026 now 4.5% - 5.0%; whilst keeping 2026-2030 in 'reasonable range.'

- CPI growth target is 'around 2%' (currently 0.2%)

- Aims are to create 12m urban jobs in 2026.

- Budget deficit of 4% of GDP - no change from last year.

- Bonds issuance: CNY4.4tn of new special local government bonds and CNY1.3tn of ultra long special sovereign bonds.

- China plans the slowest rise in defence spending since 2022 at 7%.

- Investment from investment from Central Government budget CNY755bn

The news particularly around the new bond issuance likely predicates the RRR cut of 50bps to absorp the issuance

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

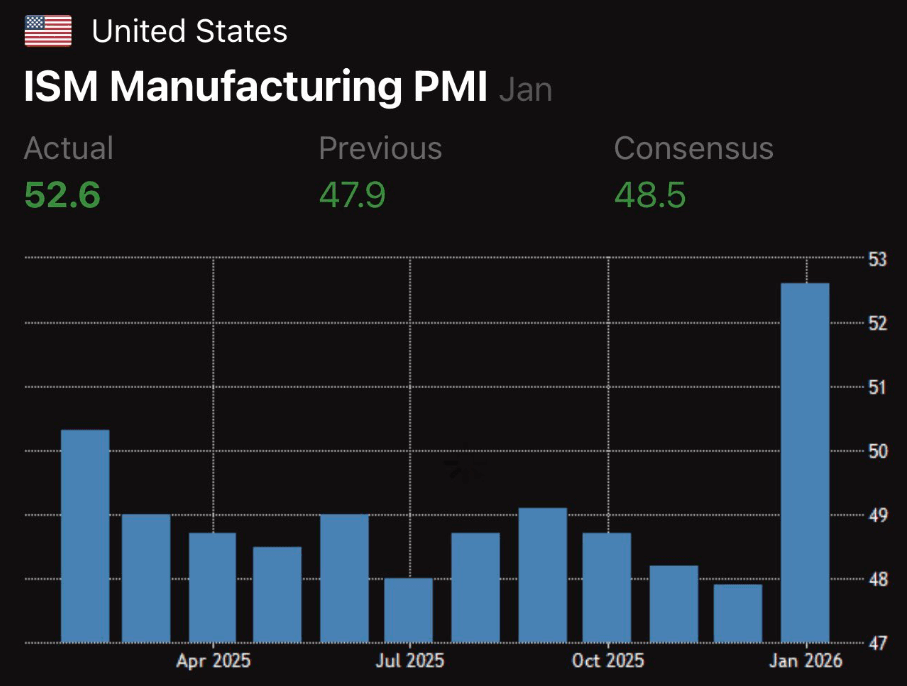

US STOCKS: S&P(ESH6)-Big ISM Beat Sees Stocks Reverse, Eyeing A Move Above 7050

The S&P(ESH6) overnight range was 6874.75 - 7017.25, SPX closed +0.54%, Asia is currently trading around 7015. The S&P looked to be potentially in some trouble as it tested its first support but a huge rebound in the US ISM manufacturing PMI saw it do a complete reversal from almost 1.3% down. Stocks continue to confound any who think it might be overdone up here. Even with clear smoke signals coming from the recent back and forth between Nvidia and OpenAI, as well as Oracle looking to raise another $50 to help finance AI projects while its stock and CDS plummet as a result. For the moment it's tough to argue with the price action as dip remains well supported. This morning futures have opened higher again, E-minis(S&P) +0.20%%, NQZ5 +0.40%. On the day, the first support is back toward the 6930-6960 area and then 6820-6870 as the market is again looking to make new highs and looking to potentially regain its upward momentum.

- MNI INTERVIEW: US Manufacturing Rebound Not Yet A Trend - ISM. U.S. manufacturing activity is still on shaky ground despite the first month of expansion in a year and a sharp rebound in new orders that could be temporary, Institute for Supply Management manufacturing chair Susan Spence told MNI.

- Ed Zitron on X: “Oracle needs to raise funding to complete the data centers so that OpenAI can raise funding to pay for the data centers. The annual revenue of AWS is like $110bn and the oAI/Oracle contract is $300bn over five years. How does OpenAI afford this/Oracle pay its debts?”

- Fejau on X: The economy is re-accelerating .” See Fig.1

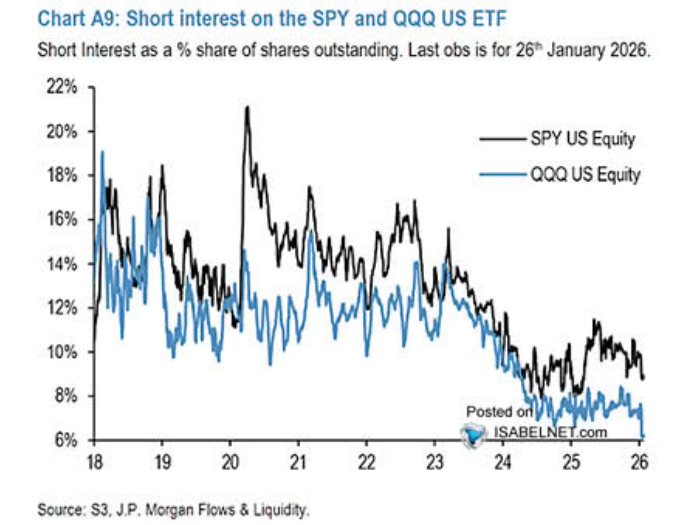

- Lance Roberts on X: “Bears are all but extinct in the current market. Short interest in both SPY and QQQ are at extremely low levels.” See Fig.2

- The S&P 500 Index Average True Range(ATR) for the last 10 Trading days: 71 Points

Fig 1: ISM Manufacturing PMI

Source: MNI - Market News/@fejau_inc

Fig 1: Short Interest

Source: MNI - Market News/J.PMorgan/ISABELNET.com

JGB TECHS: (H6) Bottom In?

- RES 3: 140.08 - High Jun 13

- RES 2: 139.05 - High Aug 4

- RES 1: 137.30 - High Sep 8 and key short-term resistance

- PRICE: 131.53 @ 15:55 GMT Feb 02

- SUP 1: 130.94 - 2.0% Lower Bollinger Band

- SUP 2: 130.66 - Low Jan 19

- SUP 3: 130.12 - 1.0% 10-dma envelope

JGBs came under intense selling pressure last week on the back of weak demand at a 20y JGB auction and increased scrutiny of Japan’s fiscal health. Resultantly, prices traded to new pullback and cycle lows. This affirms the firm downtrend that’s dominated prices since mid-September, and prices will need to challenge resistance before signaling any broader reversal. The break below the Lower Bollinger Band at 130.94 was brief, with 130.12 envelope support below.

JGBS: Futures Cheaper Overnight, 10Y Supply Due

In post-Tokyo trade, JGB futures closed sharply weaker, -28 compared to settlement levels, after a heavy session for US tsys. US tsys finished 4-5bps cheaper across the curve, reversing early Monday gains after a surge in ISM data.

- The ISM data was far stronger than expected in January as it jumped 4.7pts to 52.6 for its highest since Aug 2022, significantly above even the highest analyst estimate of 51.0. New orders and production both surged to their highest since early 2022 - unlike the final PMI survey released shortly beforehand, it doesn’t look linked to an inventory build.

- For the Jan-Mar quarter, Treasury expects to borrow $574B (prior estimate was $578B; MNI's expectation was $575B) with a financing need of $530B.

- Judging from the BLS's communications yesterday, nonfarm payrolls will be postponed from Friday until an unknown future date (known only once the government is back open).

- Today, the local calendar will see Monetary Base data alongside 10-year supply.