AUSSIE BONDS: Hawkish Global Central Banks Drive Yields Higher, Light Local Calendar

ACGBs are weaker (YM -4.0 & XM -2.5) as central banks take centre stage and push global yields higher. The BoE and Norges Bank surprise with 50bp hikes and maintain their tightening biases. The BoE hike to 5.0% brings the total tightening this cycle to 475bp, with market pricing pointing to a 6%+ policy rate before the end of the year.

- During Fed Chair Powell's second day of policy testimony to Congress, he reiterated the prevailing view that if the economy continues to perform as expected, it would be appropriate to raise rates again this year.

- The BoC published the June Minutes, revealing the underlying strength of the Canadian economy and concerns regarding the trajectory of inflation was likely to deliver more tightening.

- Cash ACGBs opened 3-4bp cheaper with the AU-US 10-year yield differential at +20bp.

- Swap rates are 3-4bp higher with the 3s10s curve flatter.

- Bills are weaker across the strip with pricing -3 to -7.

- RBA dated OIS are 3-11bp firmer for meetings beyond October with December leading. Terminal cash rate expectations return to 4.60%.

- The local calendar sees Judo Bank PMI Preliminary data as the highlight.

- The next major data is the release of the CPI Monthly next Wednesday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: CNH Remains On The Backfoot Amid Equity & Yield Headwinds

USD/CNH was mostly range bound post the Asia close on Tuesday, finding selling resistance above 7.0700, but unable to break back sub 7.0600 in a meaningful way. CNH lost 0.25% for the session, following Monday's 0.32% loss. The CNY NEER (J.P. Morgan index) edged down a further 0.09% to 123.53, fresh lows back to Nov 2022.

- Highs in USD/CNH from early last Friday around 7.0750 remain intact, but the pair has recovered strongly from recent lows sub 7.0200, which came about following increased rhetoric from the authorities and reported onshore activity from state owned banks to curb depreciation pressures.

- Equity and yield headwinds persist for CNH, while the fixing mechanism doesn't show strong pushback on CNY weakness.

- The Golden Dragon index lost 2.4% in US trade on Tuesday, after onshore equities continued to track lower, with the CSI300 back to early January levels. Yields are biased lower, albeit with the 10yr unable to sustain a move 2.70%.

- Economic headwinds are weighing on the yield backdrop, while economic decoupling, particularly in the tech space, is a clear equity headwind. Yesterday saw just under 8bn yuan of Northbound stock connect outflows.

- The local data calendar remains quiet today.

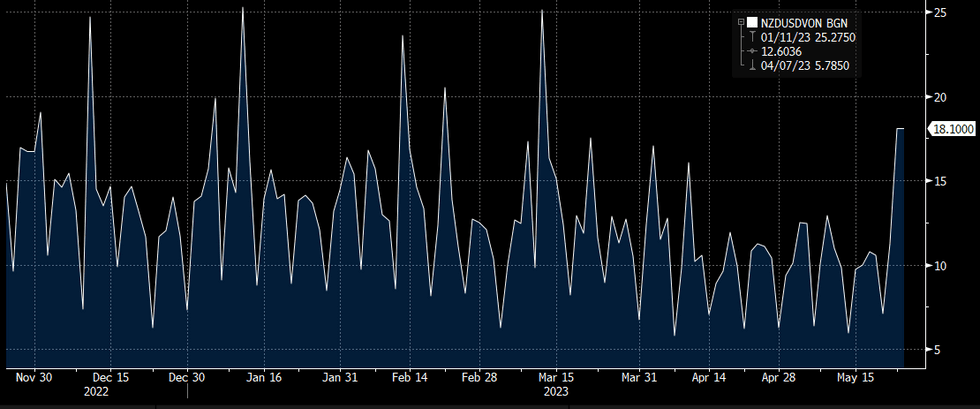

NZD: Overnight Volatility Elevated Ahead Of RBNZ, Q1 Retail Sales

NZD/USD overnight implied volatility sits at 18.10% as option markets price in a $0.6183-$0.6315 range in the aftermath of today's RBNZ meeting.

- Overnight implied volatility is at its highest level since the SVB crisis (~25%) in mid-March.

- Overnight risk reversals are skewed to the downside, however we sit well above levels seen pre-SVB crisis and within the yearly range.

- Bulls target the high from 19 May at $0.6306 a break through here opens the high from 11 May at $0.6385. On the downside bears first look to break the low 12 May $0.6182.

- On the wires shortly we have Q1 Retail Sales ex Inflation, a rise of 0.2% is expected.

- The MNI Preview of the RBNZ is here.

Fig 1: NZD/USD Overnight Implied Volatility

Source: MNI/Bloomberg

AUD: A$ Underperforms On Debt-Ceiling Driven Risk Pullback

The Aussie underperformed the G10 as risk sentiment deteriorated following no progress at the latest Biden-McCarthy debt-ceiling meeting. AUDUSD fell 0.6% and is currently trading around 0.6611. The USD index is 0.3% higher.

- AUDUSD continues its softer tone and key support lies at 0.6565, the March 10 low. A breach of this level would confirm the resumption of the bear cycle started February 2. A break of 0.6818 would reinstate a bullish theme.

- Aussie is steady against the kiwi ahead of today’s RBNZ meeting, where another 25bp hike is expected. It is currently around 1.0575. AUDJPY is down 0.6% to 91.62. AUDGBP is down 0.5% to 0.5324 and AUDEUR -0.2% to 0.6138.

- Equity markets were weaker with the S&P down 1.1% and the Eurostoxx -1%. The VIX was over a percentage point higher to 18.5%. Despite the pullback in risk, oil prices rose strongly. WTI is up 2.2% to $73.65/bbl. Cooper is 1.2% lower and iron ore fell below $100/t and is around $99.

- Today the Westpac leading index for April prints and then at 1710 AEST the RBA’s Jacobs, Head of Domestic Markets, speaks at the Australian Government Fixed Income Forum in Japan.