RIKSBANK: Hawkish comments from Ohlsson (but he is a hawk)

Mar-30 13:16

- Riksbank Deputy Governor Ohlsson is reported to have said that "everything we did in February is obsolete" and that "we are starting from scratch right now." (Source: Bbg)

- These comments are on the hawkish side, although recall that Breman said last week that "a rate hike in June can't be ruled out" and she also said that the decisions taken in February are "now a thing of the past".

- Ohlsson and Breman both hawkishly dissented in February, joined by Floden in what was a 3-3 vote with Governor Ingves breaking the deadlock and stopping reinvestments from being slowed.

- Against this backdrop its perhaps not too surprising that we are seeing these comments from the hawks but it is still Ingves' comments that remain the key to more hawkish action (with the Skingsley and Jansson both seemingly some far away from tighter policy - albeit they haven't spoken recently).

- Ingves' last commens on 16 March were that rate hikes would be needed sooner than 2024 (as the last MPR forecast) but that it was too soon to say what happens to the balance sheet. He also wouldnt be drawn on when he now expected the first hike to be.

- EURSEK hasn't really reacted to Ohlsson's comments today.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: EU Roll update

Feb-28 13:12

- Buxl: 16%

- Bund: 10% (way below pace)

- Bobl: 9% (below pace)

- Schatz: 13%

- BTP: 11%

- BTPS: 10%

- OAT; 15%

What to Watch:

Feb-28 13:08

Volatile overnight trade, heavy volumes as Russia/Ukraine crisis deepens, rates well bid but off initial gap-bid highs.

- Headline watching: Russian nuclear forces placed on enhanced combat duty rattling mkts. Piling on sanctions: US, EU, France, Germany, Italy, UK and Canada agreed to bar select Russia banks access to SWIFT network Saturday. Several EU countries close airspace to Russia flights. Meanwhile: US SENDING DELEGATION OF FORMER SENIOR DEFENSE AND SECURITY OFFICIALS TO TAIWAN ON MONDAY, Rtrs.

- Economic data at 0830ET:

- Advance Goods Trade Balance (-$100.5B rev, -$99.3B)

- Wholesale Inventories MoM (2.2%, 1.2%)

- Retail Inventories MoM (4.4%, --)

- At 0945ET: MNI Chicago PMI (65.2, 62.0)

- At 1030ET: Dallas Fed Manf. Activity (2.0, 3.5)

- Fed speak at 1030ET: Atlanta Fed Bostic, moderated virtual discussion on U.S. economy hosted by Harvard, no text but will have audience Q&A

- US Tsy bill auctions at 1130ET: $60B 13W, $51B 26W

- Later in week: Fed Chair Powell semi-annual mon/pol testimony to House Financial Services Comm on Wed, Senate Banking Comm Thu both 1000ET

- Feb nonfarm payrolls Friday (+467k, +400k)

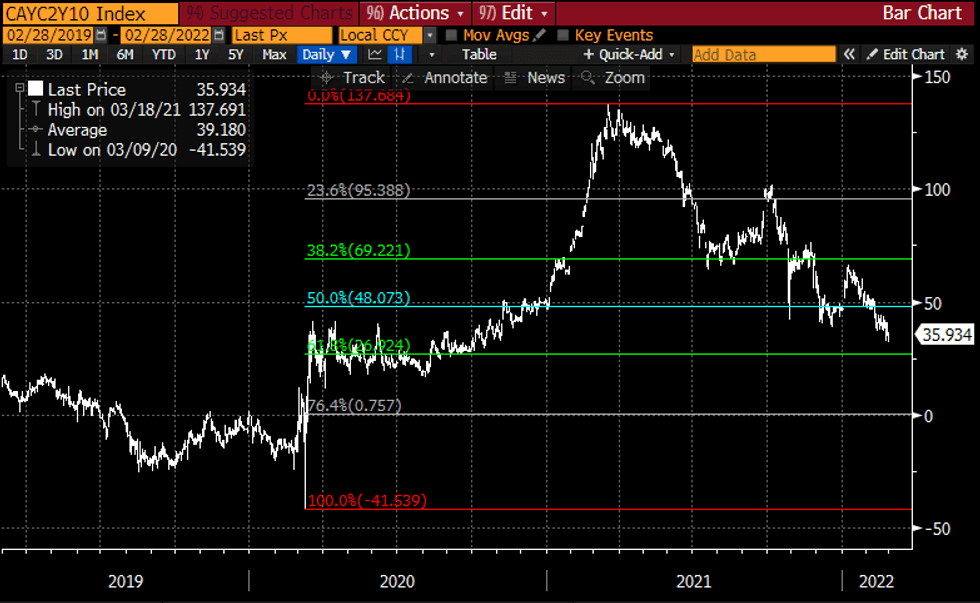

CANADA: Modest Version Of Rally In Treasuries Continues

Feb-28 13:06

- GoCs have re-gathered their strength after opening firmly, with front end belly yields 3-4bps lower and long end yields down 1.5-2.5bps.

- The slope of the yield curve remains historically close to that of Tsys, with the 2YY of 1.504% near parity and the 10YY only 5bp lower at 1.868%.

- Coming ahead of the BOC on Wed, GoCs have provided some recent easing in financial conditions with 10YY 11bps off highs.

- The 2s10s of 36bps is just off recent flats though, last seen in Nov-2020, highlighting the difficulty in controlling high inflation without weighing excessively on medium-term growth.

Canada G0C 2s10s Source: Bloomberg

Canada G0C 2s10s Source: Bloomberg