US 10YR FUTURE TECHS: (H6) Bullish Phase

- RES 4: 113-04 76.4% retracement of the Nov 25 - Jan 20 bear leg

- RES 3: 112-31 High Dec 18 and key short-term resistance

- RES 2: 112-25 61.8% retracement of the Nov 25 - Jan 20 bear leg

- RES 1: 112-20 High Feb 11

- PRICE: 112-10+ @ 11:18 GMT Feb 12

- SUP 1: 112-01 20-day EMA

- SUP 2: 111-26 Low Feb 9

- SUP 3: 111-13+ Low Feb 3

- SUP 4: 111-09 Low Jan 20 and the bear trigger

Treasuries continue to trade closer to their recent highs and the current bull cycle remains intact. This week’s gains have strengthened the short-term uptrend, signalling scope for a move towards 112-25 next, the 61.8% retracement of the Nov 25 - Jan 20 bear leg. Clearance of this price point would open 112-31, the Dec 18 high. Initial support to watch is 112-01, the 20-day EMA. A break of this level would highlight a potential reversal.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Tuesday Data Calendar: CPI, ADP Weekly, New Home Sales, 30Y Re-Open

- US Data/Speaker Calendar (prior, estimate). All times ET

- 01/13 0600 NFIB Small Business Optimism reported 99.5 vs. 99.0 prior

- 01/13 0815 ADP Weekly NER Pulse

- 01/13 0830 CPI MoM (0.3 est), YoY (2.7%, 2.7%)

- 01/13 0830 Core CPI MoM (0.3% est), YoY (2.6%, 2.7%)

- 01/13 0855 Redbook Retail Sales Index

- 01/13 1000 New Home Sales (715k est), MoM (-10.6% est)

- 01/13 1000 StL Fed Musalem outlook, Q&A event hosted by MNI

- 01/13 1130 US Tsy $75B 6W bill auction

- 01/13 1300 US Tsy $22B 30Y Bond auction re-open (912810UP1)

- 01/13 1400 Treasury Budget

- 01/13 1600 Richmond Fed Tom Barkin moderated discussion

- Source: Bloomberg Finance L.P. / MNI

SWAPS: Some Of Yesterday's Flattening Is Retraced, Dutch Pensions Still Dominate

Bear steepening seen on the EUR swaps curve after yesterday’s aggressive bull flattening move, with swap rates 1.5-3.0bp higher on the day alongside a move higher in core global FI yields.

- 50s are threatening a clean break back above 3.00%, paring around half of yesterday’s decline.

- Markets are seemingly reconsidering the scale of yesterday’s moves (which saw long end swap rates register multi-year lows, with the EUR30s50s curve printing the lowest close since April) given the structural upside/steepening risk to long end EUR swap rates over the medium-term (stemming from the Dutch pension transition).

- Sell-side comments surrounding yesterday’s receiver-side move & flattening of the curve generally chime with our own colour.

- They have attributed the move to the update from Dutch pension Fund PFZW (the second largest such fund, with AUM of ~EUR250bln), outlining the fund’s intention re: hedging interest rate risk exposure after the transition.

- The interest rate hedging outlined in the document was larger than the market expected but still represents a meaningful reduction vs. current levels, presenting steepener risks to the EUR curve over the medium-term (as related pay-side flows materialise).

- Still, any such move is unlikely to come in a straight line owing to already heavy positioning in steepener positions and the potential for further “disappointment” when it comes to updates from individual funds, with yesterday’s move underscoring market sensitivity to related headline flow.

- When it comes to yesterday’s announcement, ING estimate that “a 10ppt increase in hedging ratio for PFZW translates to increased demand for fixed receiver swaps of ~EUR40mln DV01”.

FRANCE: OAT/Bund Marginally Wider; State Budget Second Reading This Evening

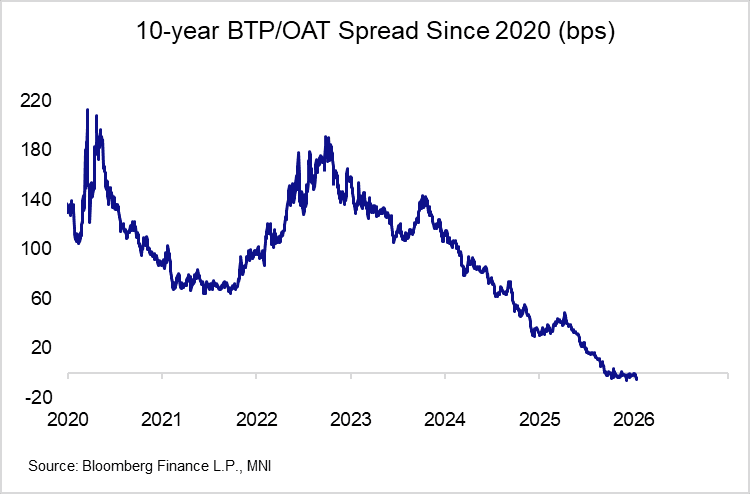

The 10-year OAT/Bund spread was able to move below the 70bp figure last week due to a Bloomberg 10-year Bund benchmark roll, but political risks remain in focus. The National Assembly will hold a second reading of the 2026 state budget this evening, but prospects of finding a compromise appear bleak. This increases the risk of PM Lecornu having to resort to Article 49.3 to pass the budget. OATs lightly underperform peers this morning, with the 10-year BTP/OAT spread close to -5.0bps.

- Via Le Parisien, spokesperson for the executive, Maud Bregeon, noted that "there are still some equations that we cannot solve," ... "the question of large companies and this additional corporate tax " or "the contribution of local authorities " for which the gap is "significant (...) between what the government proposes and what the Senate proposes."

- France has issued a mandate for a new 20-year benchmark transaction, which we expect to take place tomorrow with an E8-10bln size. The mandate came a little earlier in the month than expected, but this was only worth a ~0.5bps rise in the 10/20/30s OAT fly.