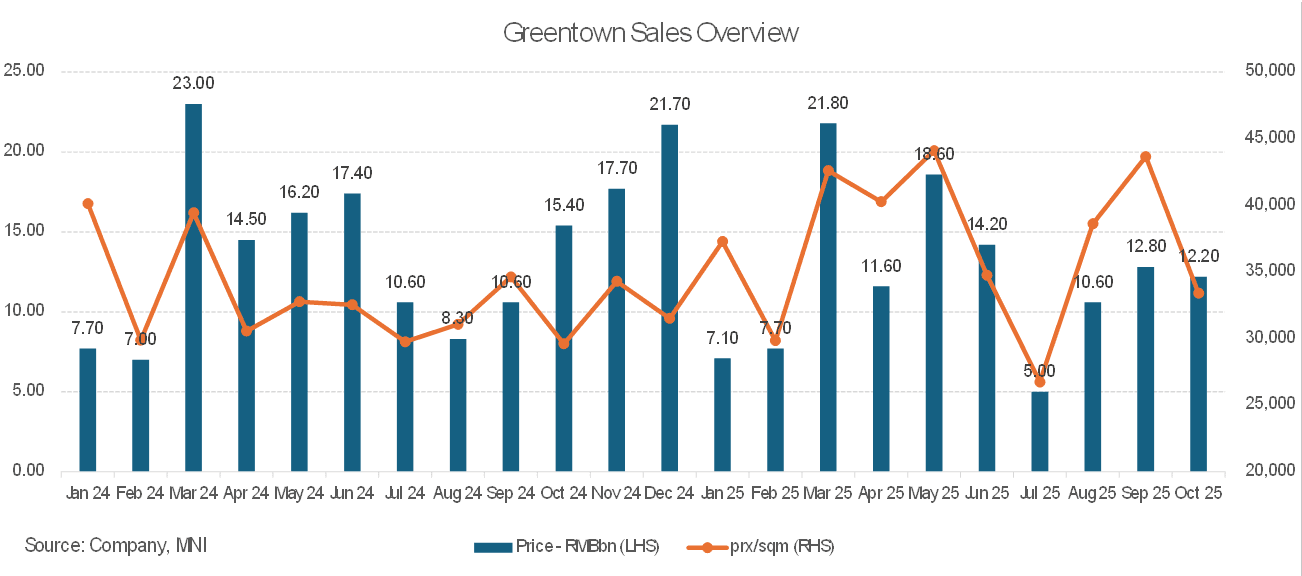

EM ASIA CREDIT: Greentown China: Monthly sales weak

(GRNCH, B1/BB-/NR)

"*Greentown China Holdings October Contracted Property Sales CNY12.2B"- BBG

Monthly property sales statistics are out for October. Sales reached around RMB12.2bn (-21% YoY), with an approximate average selling price of RMB 33,396 per sqm (+13% YoY). As shown in the attached chart, year to date end October sales are around 7% lower YoY, though we note the average selling prices over the same period are +12% YoY. Overall negative for spreads.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

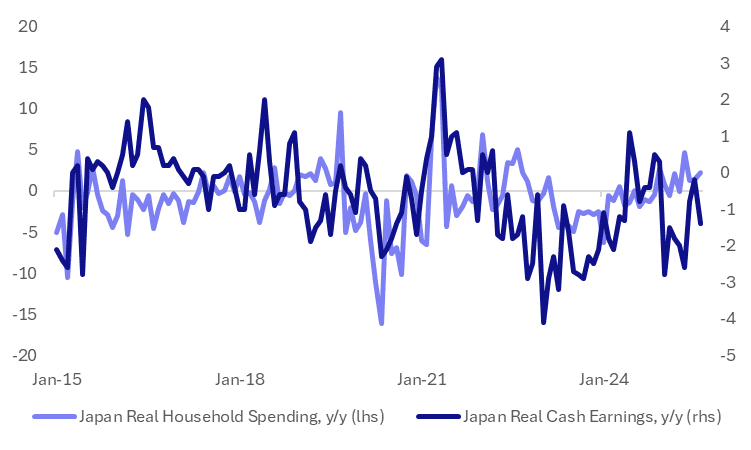

JAPAN DATA: Aug Labor Earnings Notably Sub Forecasts, BoJ Likely Holding In Oct

August labour earnings data in Japan was comfortably below market expectations. Headline earnings rose 1.5%y/y (against a 2.7 forecast and 3.4% July outcome), while real earnings dipped back to -1.4%y/y (-0.5%) was forecast. Real earnings have not been in positive territory (in y/y terms) so far in 2025. This will reinforce expectations of the BoJ likely remaining on hold at the Oct policy meeting. Japan's new political regime had already noted that Oct is too soon for a rate hike. BoJ Governor Ueda also noted recently that the risk was low for the central bank to fall behind the inflation/policy curve( with today's data supporting this theme).

- The chart below updates the household spending versus real labour earnings trend post today's data. Recall yesterday that household spending was stronger than forecast but today's real earnings data re-opens a modest wedge between the two series. This may create uncertainty around the extent which the positive trend in household spending can be maintained.

- Bonus payments were down notably in y/y terms, off -10.5%y/y, versus a 6.3% gain in July, so this provides some offset to the softer headline results. We can often bounce back after negative months.

- On a same sample base, cash earnings printed at 1.9%, versus 2.7% forecast. Scheduled full time pay on the base y/y was 2.4% against a 2.5% forecast. Special payments fell -5.7%y/y (against a 4.7% rise in July).

- This may help offset the weaker than expected headline outcomes, but still the BoJ and authorities are likely to want to see stronger underlying earnings momentum.

Fig 1: Real Earnings Struggling For Positive Momentum

Source: Bloomberg Finance L.P./MNI

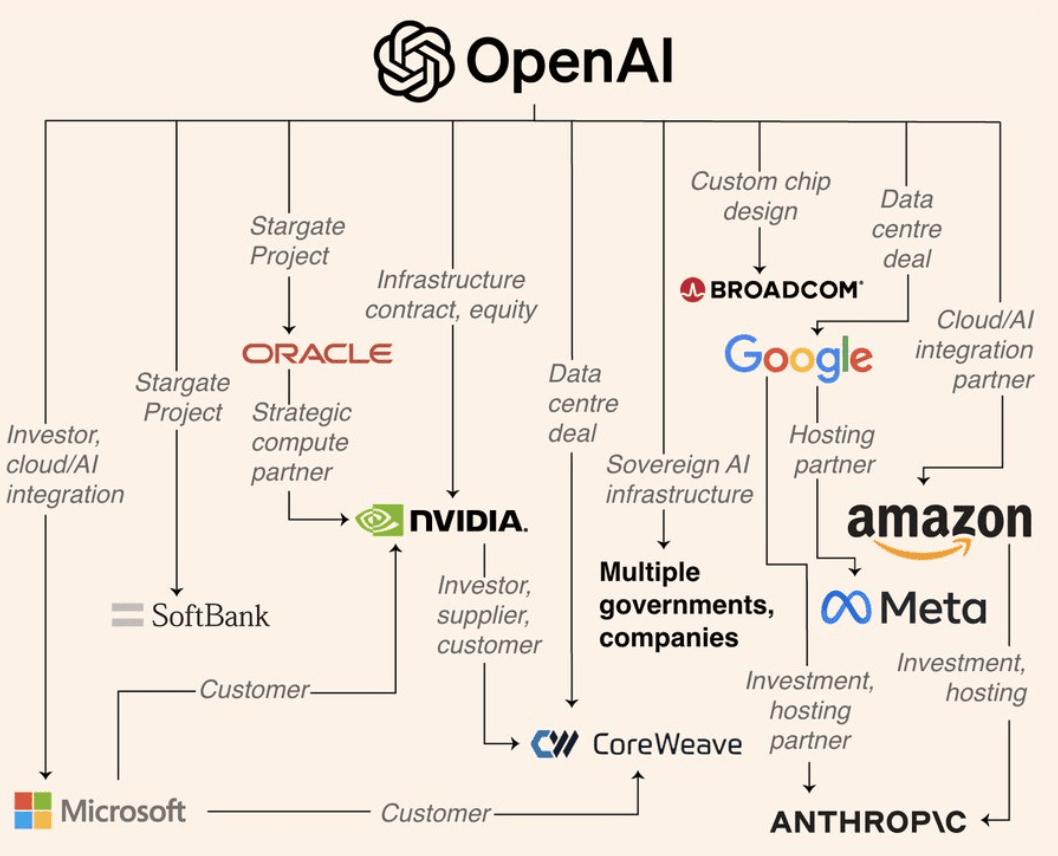

US STOCKS: S&P(ESZ5) - Corrects Lower After Multiple Failures Around 6800

The S&P(ESZ5) overnight range was 6747.25 - 6802.75, SPX closed -0.32%, Asia is currently trading around 6760. The E-mini’s had a quick look above 6800 and then dropped pretty quickly from there as we see the first signs of the move becoming exhaustive. This morning US futures have opened pretty muted, E-minis(S&P) -0.02%, NQZ5 -0.01%. The stock market continues to look way overdone but has brushed off every hurdle thrown at it. It is clearly still in a very strong uptrend but is starting to show some signs of the move potentially stalling. First support is now back towards the 6600 area.

- Lance Roberts on X: “The market continues to advance in a slow-motion melt up driven by virtually asset class hitting record highs. From Large caps, to small caps, most-shorted, lowest quality, gold, and bitcoin, whatever asset you own is rising. Which also suggests that when the run eventually ends, the selloff will be broad."

- “The OpenAI deal framework is very concentrated into a few companies recycling, and counting, the same investment dollars. What could possibly go wrong! - h/t @FT”

- Bloomberg - “A wave of deals involving Nvidia and OpenAI is escalating concerns that an increasingly complex web of transactions is artificially propping up the trillion-dollar AI boom.”

- Jim Bianco on X: “The AI boom/bubble now has the S&P 500 and the Nasdaq 100 (QQQ) with the same eight largest stocks (table). These two indices are merging into the same thing.”

- Daily Chartbook on X: "Equities have been scaling new highs, but positioning while overweight is not yet stretched (0.45sd, 70th percentile)" - Deutsche Bank via @neilksethi.

Fig 1: AI Deal Recycling

Source: MNI - Market News/@LanceRoberts/@FT

AUSSIE BONDS: ACGB Mar-36 Supply Faces Higher Yield But A Flatter Curve

The Australian Office of Financial Management (AOFM) will today sell A$1200mn of the 4.25% 21 March 2036 bond. The line was last sold on 6 August 2025 for A$900mn. This new line was sold by syndication on 5 February 2025 for A$15.0bn. Bidding at today’s auction is likely to be shaped by several key factors:

- The outright yield is roughly 10-15bps higher than the previous auction level and about 20bps below the late February peak.

- However, the 3/10 yield curve is slightly flatter than the previous auction level and sits around 30-35bps flatter than its recent high.

- Sentiment toward longer-dated global bonds remains uncertain.

- This bond is also included in the XM futures basket, which may support demand.

- Overall, firm pricing is still anticipated at today’s auction, given the higher yields and other favourable factors.

- Results are due at 0100 BST / 1100 AEST.