US OUTLOOK/OPINION: Goldman: Softer AHE On Negative Calendar Effects

Jun-01 19:27

- Goldman see NFP growth at a seasonally adjusted 175k in May. Job growth tends to slow in May when the labor market is tight, and Big Data also indicate a deceleration. We also assume a roughly 25k drag from reduced credit availability, for example in the leisure and hospitality and other services industries.

- One offsetting positive factor is that the May seasonal factors have evolved favorably in recent years.

- Elsewhere they see the u/e rate unchanged at 3.4%, reflecting a modest rise in household employment and unchanged labor force participation (at 62.6%).

- AHE seen at 0.25% M/M sa after +0.5%, lowering the year-on-year rate to 4.3%, reflecting negative calendar effects and waning upward wage pressures.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Only Modest Paring Of Gains Post JOLTS & Regional Banks Pressures

May-02 19:23

- Cash Tsys have seen a bid re-emerge in recent trading, more notably so for the long-end, but remain off highs seen after JOLTS data showed further labor market moderation. Coming on day one of the two day FOMC meeting, it has also seen WTI slide by than 5% and regional banks under pressure.

- Debt limit back and forth continues, with Schumer most recently saying they can only debate spending after the clean debt bill is passed, with a full two-year debt-limit extension required. McConnell will be at the May 9 meeting that was earlier reported that Biden will have with McCarthy.

- 2YY -16.7bp at 3.974%, 5YY -17.6bp at 3.459%, 10YY -14.0bp at 3.428% and 30YY -9.4bp at 3.714%.

- TYM3 trades +1-03+ at 115-19+, just within earlier highs of 115-21 with next resistance seen at 115-30+ (Apr 26 high).

- Aside of course from the FOMC decision, tomorrow includes ADP employment and ISM services.

US OUTLOOK/OPINION: Macro Developments Since March FOMC: Prices [2/2]

May-02 19:04

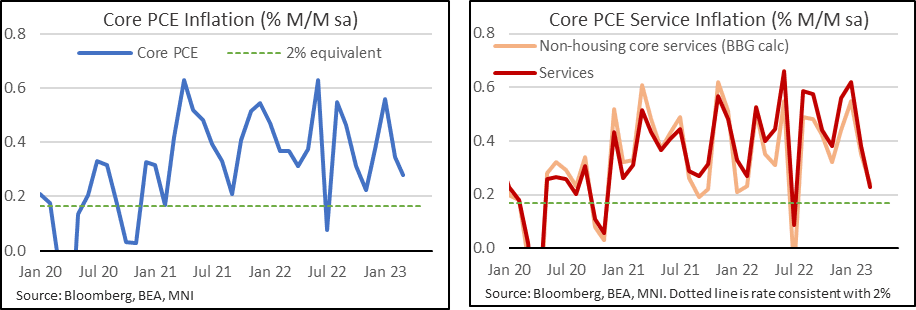

- Core PCE inflation meanwhile provided the greater surprise, with the Q1 advance coming in surprisingly strongly at 4.94% annualized (cons 4.7%) for the strongest quarter since 1Q22.

- The Fed can however take some consolation that the relative upward surprise was focused early in the quarter, which instead has seen the latest monthly rates slow from 0.56% M/M in Jan, to 0.35% in Feb and 0.28% in March data released Apr 28.

- This latest run rate was the softest since Nov’22 whilst more pleasingly for the Fed, Bloomberg’s calculation of the preferred non-housing core services series eased a tenth to 0.24% M/M for its softest since Jul’22 and prior to that Feb’22.

- This ‘supercore’ clearly remains too high seeing as July’s -0.09% M/M was the only time its been below the monthly rate consistent with 2% annualized inflation since Nov’20, but the latest moderation is at least in the right direction.

US OUTLOOK/OPINION: Macro Developments Since March FOMC: Prices [1/2]

May-02 19:02

- After a recent string of large surprises, core CPI was broadly as expected and didn’t move the dial.

- Landing mid-April, core CPI inflation eased from 0.45% to 0.385% M/M but remains stubbornly high as it marked the fourth month with a 0.4% reading to 1 decimal place.

- The main downside surprise came from a sharp slowing in rents for their softest monthly readings since Apr/Mar’22, generally coming a few months ahead of analysts expectations for the always hard to predict passthrough from softer new lease agreements.

- However non-housing core services saw only varying degrees of moderation, but perhaps of some comfort were propped up by volatile items that could reverse ahead whilst dispersion measures also generally retreated somewhat.

Trending Top

Mar-27 20:13