GOLD: Gold Down On Fed/US GDP But Up Today As Tariff Deals Agreed

Jul-31 01:26

Gold fell 1.6% to $3275.18/oz on Wednesday driven by US Q2 GDP printing at a stronger-than-expected 3% saar and Fed Chair Powell noting that “we have made no decisions about September” which reduced the odds of a September rate cut. Non-interest bearing gold is buoyed by rate cuts and expectations of them. US yields rose and the BBDXY USD index was up 0.8%.

- Gold has started Thursday 0.5% higher at $3290.1 with the USD -0.1% after a number of trade deals with the US have been announced – some better than others. India is to face 25% tariffs plus an unspecified “penalty” for buying Russian oil and weapons, Brazil 50% for policies that threaten US security, while South Korea’s will be 15% in line with Japan and the EU.

- Prices reached a low of $3268.18 yesterday, below support at $3301.9 and $3282.8 thus opening the bear trigger at $3248.7. Bullion’s rally today though is shifting it away from this key level again with a high of $3291.1.

- Unlike gold, silver is steady at $37.14 today after falling 2.8% to $37.132 on Wednesday. It reached a low of $36.790 after the Fed decision, below initial support at $37.878, 20-day EMA, opening $36.521, 50-Day EMA.

- Equities were mixed with the S&P down 0.1% but futures have started today up 0.8% and the Euro stoxx rose 0.3% Wednesday. Oil prices continued to rally with WTI up 1.6% to $70.30/bbl. Copper sank 17.7%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

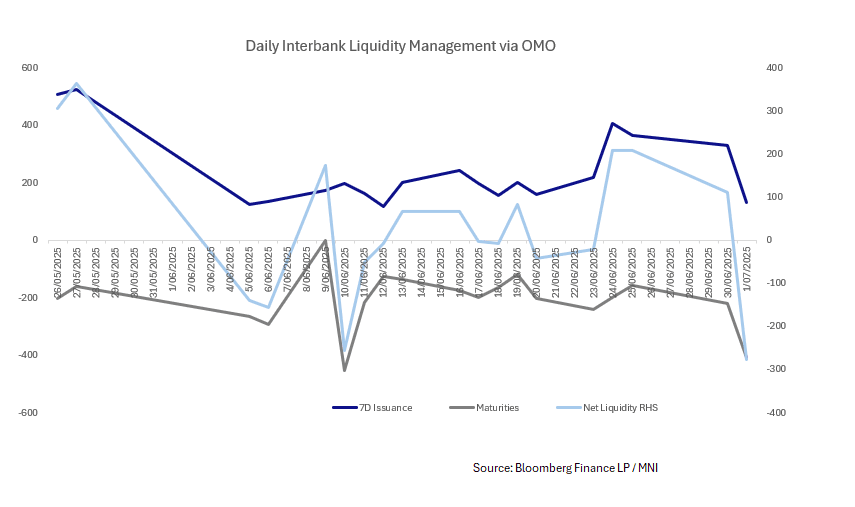

CHINA: Central Bank Withdraws CNY275.5bn via OMO

Jul-01 01:24

- The PBOC issued CNY131bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY406.5 bn

- Net liquidity injection CNY275.5 bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.41%, from prior close of 1.91%.

- The China overnight interbank repo rate is at 1.36%, from the prior close of 1.90%.

- The China 7-day interbank repo rate is at 1.60%, from the prior close of 2.30%.

JGBS: Futures Weaker After Tankan Delivers Upside Surprise

Jul-01 01:23

In Tokyo morning trade, JGB futures are weaker, -2 compared to settlement levels, after reversing the overnight session’s modest gains.

- The Q2 Tankan survey delivered some positive upside surprises. The large manufacturing index rose to 13, versus 10 forecast and 12 prior. The outlook for this segment was also better than forecast, printing at 12 (9 was forecast and 12 was the Q1 outcome). The all industry capex estimate was also stronger than expected, coming in at 11.5%, versus 10.0% forecast (3.1% was the prior outcome). For large non-manufacturing firms, the results were slightly less positive, with headline index at 34, in line with forecast, while prior was 35. The outlook printed at 27, below the expected 29 outcome (28 was recorded in Q1).

- President Donald Trump threatened to impose a fresh tariff level on Japan, citing the country's unwillingness to accept US rice exports, despite Japan's massive rice shortage. (per BBG)

- Cash US tsys are modestly richer, with a flattening bias, in today’s Asia-Pac session after yesterday’s bull-flattener.

- Cash JGBs are modestly cheaper across benchmarks. The benchmark 10-year yield is unchanged at 1.432% ahead of today’s supply

- Swap rates are flat to 1bp higher. Swap spreads are mixed.

MNI: CHINA PBOC CONDUCTS CNY131 BLN VIA 7-DAY REVERSE REPO TUE

Jul-01 01:22

- CHINA PBOC CONDUCTS CNY131 BLN VIA 7-DAY REVERSE REPO TUE