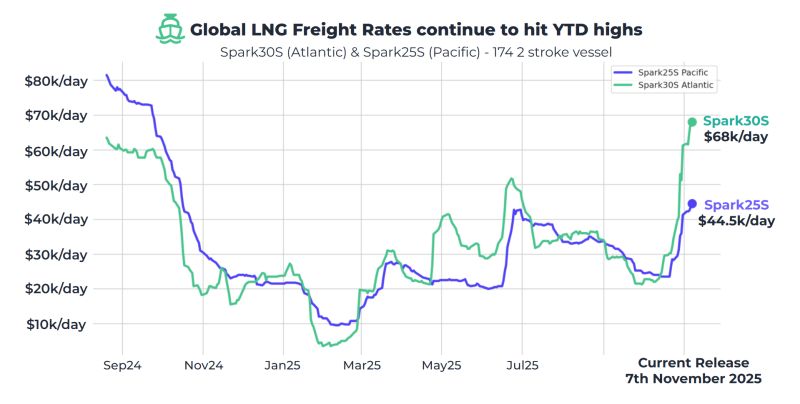

LNG: Global LNG Freight Rates at New Year to Date High: Spark

Global LNG freight rates continue to rise this week to reach new year to date highs, according to Spark Commodities.

- Spark30 (Atlantic) rate rose another $6.75k on the week to the highest since August 2024 at $68k/day.

- Spark25S (Pacific) rates rose $4.25k on the week to the highest since October 2024 at $44.5k/day

- Q4 2025 rates for both basins are now the highest priced quarter of the year and no longer mirror the winter seasonal low seen last year.

- A spike in LNG charter rates has been driven by a cold snap in Asia, tied with an increase in floating LNG storage across the globe amid a sudden rise in vessels ‘slow-steaming, according to Timera Energy.

- The JKM - TTF Dec25 spread has narrowed slightly since reaching the highest since mid-Sep. at $0.32/mmbtu on Nov. 5 and back to around $0.2/mmbtu today, according to Bloomberg data.

Source: Spark Commodities

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

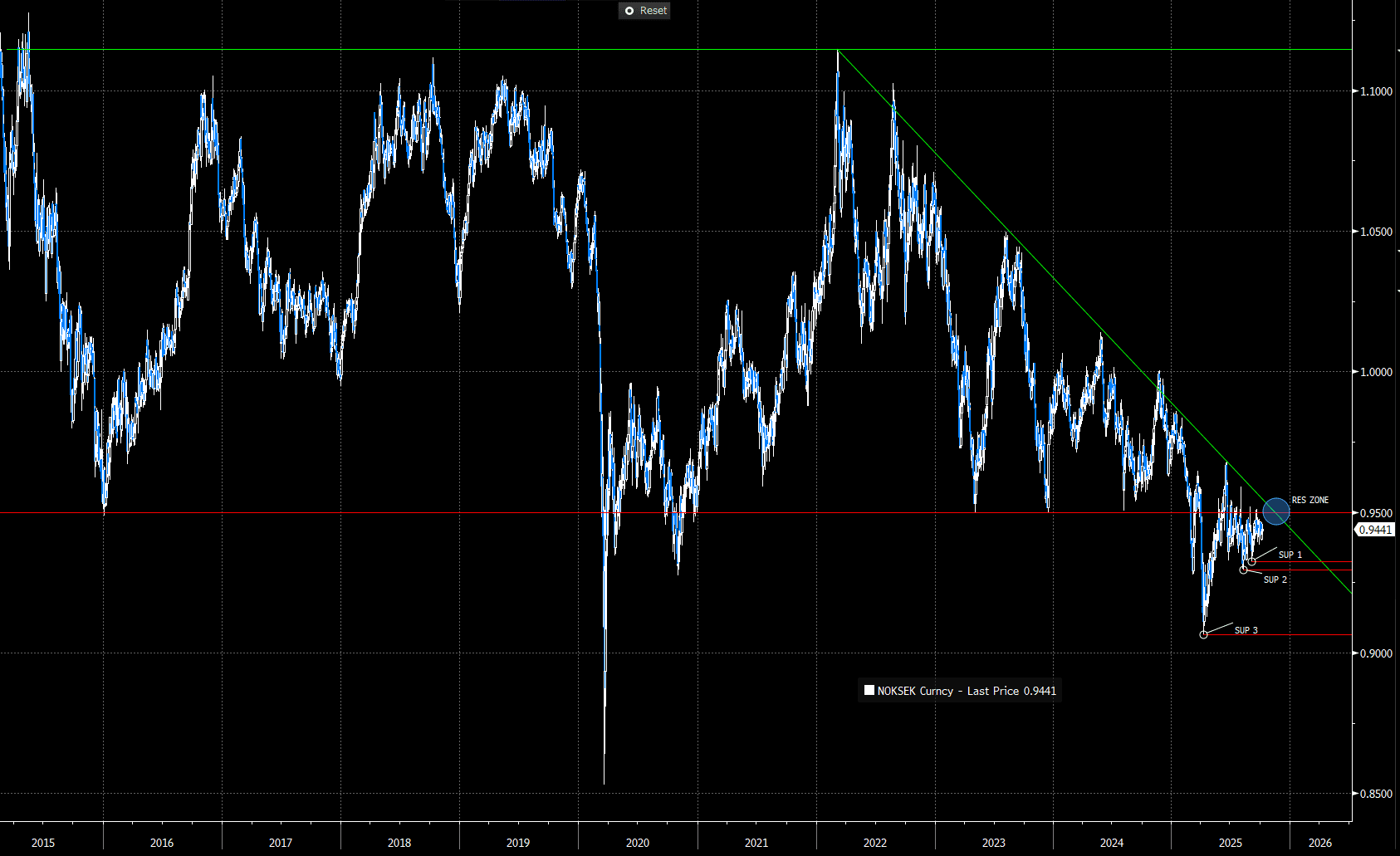

SCANDIS: Trendline Resistance May Set The Tone For NOKSEK In Coming Months

The sideways trend in NOKSEK since the start of July has narrowed the gap to medium-term trendline resistance drawn from the March 2022 high. Interaction with this trendline will be key for the direction of the cross over the next few months, particularly as it now closely aligns with 0.9500. The cross has failed to close above this level for three months, and 0.9500 has historically been an important pivot support going back to 2016.

- Relative growth arguments may support SEK outperformance versus NOK in the coming months: The monetary policy stance in Sweden is more accommodative than in Norway, the Government’s expansionary 2026 budget is focused on stimulating household consumption, and Sweden may stand to benefit more from German/European defence spending spillovers (i.e. perform as a high beta Euro).

- However, Norwegian growth has held up well this year, and next week’s 2026 budget announcement is likely to reaffirm an expansionary fiscal stance. There’s not yet a clear consensus around the policies expected, but PM Store’s reliance on more left-leaning parties following September’s election may set the stage for higher taxes on high earnings to fund increased welfare spending. Nominal rate differentials should also remain in favour of NOK for the foreseeable future following Norges Bank’s hawkish September cut. Friday's inflation reports presents the immediate risk event for NOK.

- In Sweden, some analysts also caution that the recycling of persistent current account surpluses into foreign assets are a structural net negative for the currency. We have sympathy with this argument, and note that in recent months the reallocation/repatriation of domestic equity fund flows back into Sweden has stalled.

- Initial support in NOKSEK is the September 5 low at 0.9324 (SUP 1 on chart), which shields the August 11 low of 0.9295 (SUP 2). Clearance of these levels would expose the April low of 0.9065 (SUP 3).

- SEB believe Q4 weakness may present a buying opportunity in NOK. They think the krone is likely weaken into year-end “on falling oil prices, negative seasonal patterns, and shifting drivers from domestic to global factors”. However, they see next year’s outlook as more supportive owing to “rebound in oil prices, a weaker USD, seasonal strength, and potentially larger NOK purchases”

Figure 1: NOKSEK Since 2015 (Source: Bloomberg Finance L.P.)

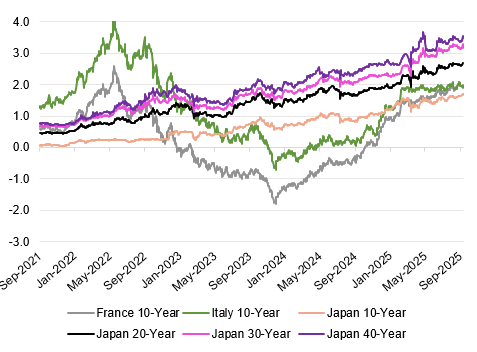

BONDS: BTP & OAT Yields Unlikely To Tempt Japanese Investors After Recent Sales

A little more on our earlier point re: Japan shedding French bond exposure in the month of August, as well as the extension of the recent Japanese selling of Italian paper.

- 10-Year BTPs & OATs (which trade at very similar levels) only provide a relatively slender 20-25bp FX-hedged yield pickup over 10-Year JGBs, while the long end of the JGB curve continues to provide meaningfully higher yields.

- This provides little incentive for Japanese investors to participate in those markets, given the ongoing French political and fiscal risks, along with already tight levels in the BTP/Bund spread.

- One caveat to this is that the Japanese long end may be subjected to greater volatility after the ascension of Takaichi to Prime Minister.

- However, she watered down her expansionary fiscal stance during her election campaign, and although the session of JGB trading immediately after her victory saw meaningful twist steepening of the curve, yesterday’s 30-Year JGB auction drew firm demand, which could suggest that domestic investors are not hugely worried about her fiscal stance, further lessening the need to seek out offshore exposure.

Fig. 1: JGB Yields & FX-Hedged 10-Year OAT & BTP Yields From The Perspective Of A Japanese Investor

Source: MNI - Market News/Bloomberg Finance L.P.

PIPELINE: Corporate Bond Roundup: $1B Kommunalbanken Norway Launched

- Date $MM Issuer (Priced *, Launch #)

- 10/08 $1B #Kommunalbanken Norway WNG 3Y SOFR+37

- 10/08 $Benchmark Federal Home Loan 2Y +4a

- 10/08 $Benchmark Mamoura 10Y +90a

- $7.85B Priced Tuesday