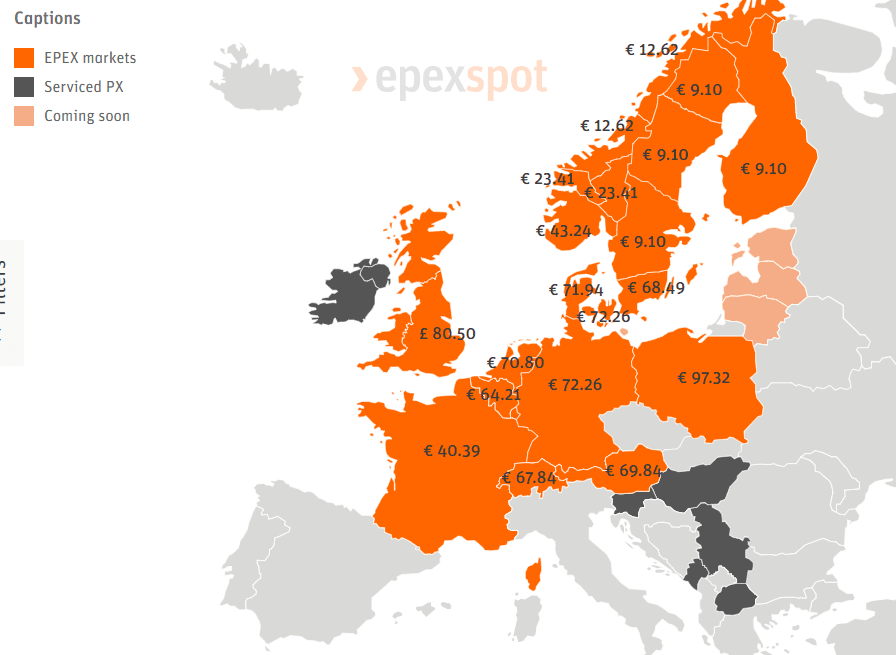

POWER: German-French Day-Ahead Premium Widens on Low Wind, Stable French Nuclear

May-24 11:07

CWE day-ahead base-load contracts fell on the day amid reduced power demand over the weekend – with France-German baseload contracts widening on the day. Wind output over the weekend and next week in Germany is expected to be low, with solar output remaining firm – possibly limiting upside movement on delivery.

- The German day-ahead spot settled at €72.26/MWh, down from €102.19/MWh in the previous day.

- The French day-ahead spot closed at just €40.39/MWh from €71.41/MWh in the previous day.

- This placed the German-French baseload premium at €31.87/MWh from €30.78/MWh in the previous session.

- German wind output is expected between 2.44-4.09GW, 4-6% load factors over 25-26 May, before rising slightly 7%, or ~ 4.4GW over 27-28 May, according to Spot Renewbales.

- This Monday, German wind output is forecast to peak at 7.41GW at 2am, compared with a high of 7.50GW at 11pm on Friday: Bloomberg model.

- But German solar output is forecasts 22-25%, or 12.47-13.99GW over 25-26 May, with output between 7.2-12.41GW over 27-28 May.

- German solar output on Monday is seen peaking at 36.94GW at 1pm, compared with a high of 28.63GW at 2pm on Friday: Bloomberg model.

- German power demand is forecast to average between 35-53GW over 25-26 May, down from 41-64GW on Friday, data from Entso-E show. Demand will then increase between 37-63GW over 27-28 May.

- Warmer-than-normal temperatures are still expected across Europe over the next two weeks.

- France’s nuclear reactors were operating at 71% of full capacity on Friday – unchanged on the day, according to Bloomberg.

- French utility had 40 reactors available with a combined output of 41.76GW as of 8 a.m. in Paris.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OAT: Tested Monday's low

Apr-24 11:07

- French OAT has also tested Monday's low of 125.54, so far printed a 125.56 low.

- This was a new 2024 high in 10yr Yield on Monday.

Looking further out, reference 125.64:

- 3.14% = 124.71 (61.8% retrace of Oct/Dec fall).

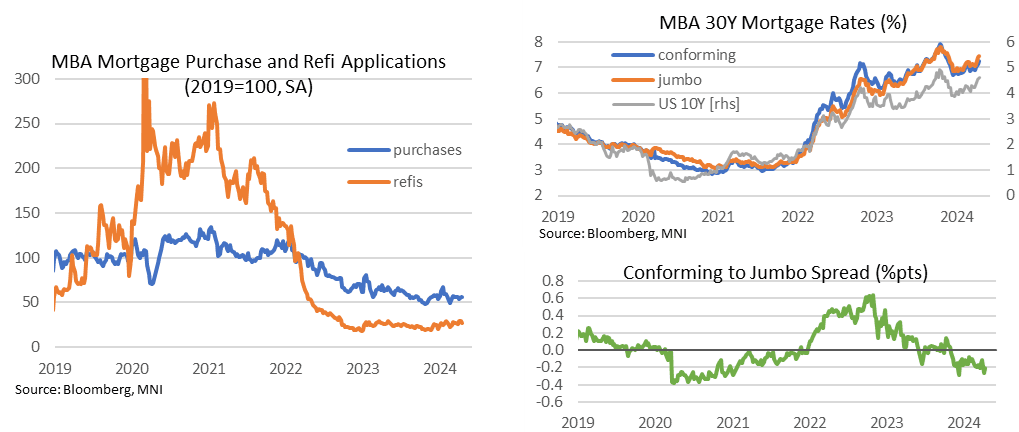

US DATA: Mortgage Applications Shrug Off Further Increase In Rates

Apr-24 11:07

- MBA mortgage applications fell a seasonally adjusted 2.7% M/M last week after increasing 3.3% the prior week.

- Declines were led by refis (-5.6% after +0.5%) whilst purchases dipped -1.0% after +5.0%.

- The 30Y conforming mortgage rate increased a further 11bps on the week to 7.24%, its highest since late November.

- Mortgage rates have increased 33bps since late March yet composite applications are surprisingly 0.6% higher over that period (albeit still less than 50% of 2019 levels).

EGB SYNDICATION: 30-year Jun-54 GGB: Final terms

Apr-24 11:05

- Size: E3bln (larger than the E1.5-2.5bln MNI expected)

- Books closed in excess of E33bln (inc E1.8bln JLM interest)

- Spread set at MS+165bp

- (Guidance was MS+175bp area then revised to MS+170bp +/-5bps (WPIR)

- Coupon: Annual, act/act, short first

- Maturity: 15 June, 2054

- Settlement: May 2, 2024

- ISIN: GR0138018842

- Bookrunners: BNPP, BofA, DB (B&D), GS, JPM, PIRAEU

- Timing: Allocations and pricing later today

From market source