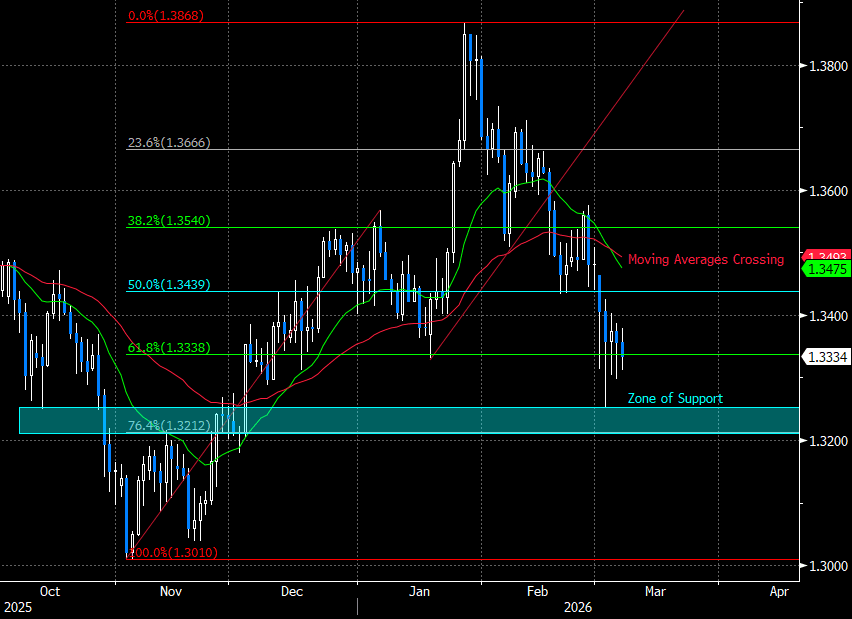

FOREX: GBPUSD at Inflection Point; NatGas Prices Key

On a purely technical basis, paradoxically GBPUSD remains inside a medium-term uptrend - largely due to the lagging nature of the moving average indicators used in defining the structure and the pace of the downleg this week. While these indicators are crossing, the pattern requires a further deterioration before changing the outlook. As such, the price finds itself at an interesting inflection point:

- If the price action doesn't reverse from here, moving average indicators will fail to recover. More consequentially, if these moving averages act as resistance, this would provide a strong signal that the medium-term cycle is turning. This raises the near-term importance of levels including the weekly low at 1.3253 and 1.3212, the 76.4% retracement for the upleg off the November low that is helping define the current structure.

- Conversely, a move toward mediation in Iran and relief via energy costs could prompt a spot rally. A move higher here would affirm the current bullish MA set-up, and confirm the short-term weakness phase as corrective, and not a fundamental trend switch.

Figure 1: Moving averages have crossed, but further weakness needed to trigger trend shift

Source: MNI / Bloomberg Finance L.P.

- GBP's sensitivity to higher energy prices is key here. UK electricity prices are uniquely tied to the natural gas price, even relative to Europe. UCL research found that in the UK "gas set the electricity price 98% of the time, whilst generating just over 40% of electricity", far higher relative to the European average of gas setting the price 58% of the time, whilst generating 34% of the electricity.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Early SOFR/Treasury Option Roundup: SOFR Puts, Tsys Paired

Overnight SOFR options lean toward downside puts, Tsy options more paired, all on lighter volumes. Underlying futures mildly mixed, inside narrow ranges w/ curves twisting flatter (2s10s -.223 at 69.160). Focus on ADP employment & ISM Services data this morning, Friday's NFP delayed to Monday at the earliest after the short US Gov shutdown ended late Tuesday. Projected rate cut pricing easing slightly vs. late Tuesday levels (*): Mar'26 at -2.6bp, Apr'26 at -6.1bp (-6.4bp), Jun'26 at -17.1bp (-17.9bp), Jul'26 at -24.6bp (-25.9bp).

- SOFR Options:

- 2,000 SFRJ6 96.43 puts, 2.5 ref 96.52

- -10,000 2QH6 96.37/96.50 put spds, 3.0 ref 96.605/0.10%

- 2,000 SFRK6 96.37/96.50/96.62 iron flys, 9.5 ref 96.52

- +2,000 SFRK6 96.43/96.50/96.56/96.62 call condors, 1.5 ref 96.525

- +1,000 SFRH6 96.31/96.37/96.50 2x3x1 broken put flys, 3.5 ref 96.36

- -2,000 SFRH6 96.37 puts, 3.75

- -7,750 SFRM6 96.43 puts, 5.0 ref 96.52

- +2,000 0QZ6 97.25 calls, 10.5 ref 96.65

- Treasury Options:

- +3,500 Wednesday wkly 111/111.5/112 call flys, 23 (exp today)

- 1,000 USH6 111/113 put spds ref 114-20

- 1,600 TYH6 110.75 puts, 5 ref 111-18

- +1,500 TYH6 110 puts, 2 vs. 111-12/0.05%

- -2,000 FVH6 109/110.5 1x2 call spds, 5.5 ref 108-22.75

- +2,000 TYH6 113/114.5 call spds, 3 ref 111-24/0.08%

- +3,000 Wednesday wkly 111.75/112 1x2 call spds, 2 vs. 111-23.5/0.08%

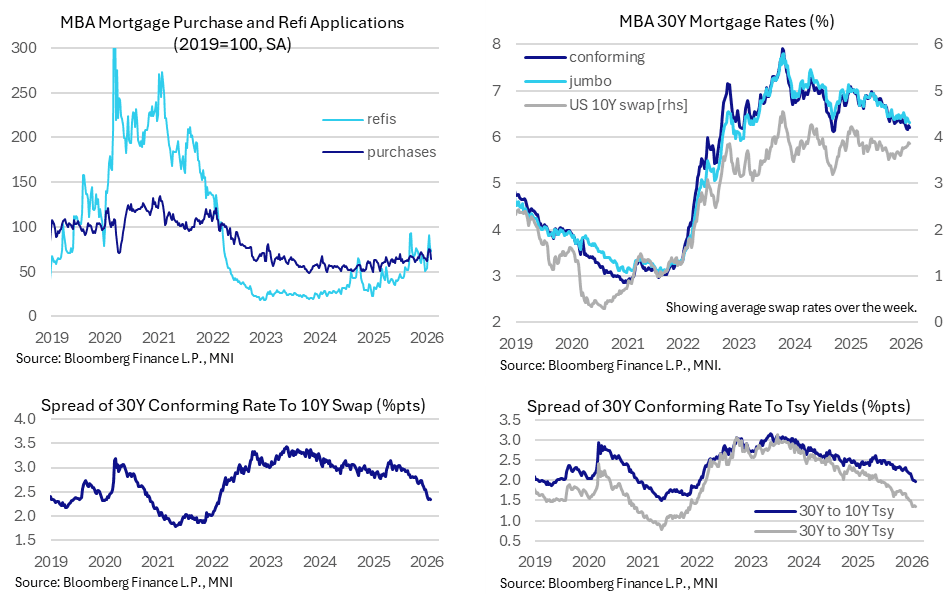

US DATA: New Purchase Mortgage Applications Fell Sharply Last Week

Hopes of higher new purchase mortgage activity as a sign that home sales could be set to pick up was dashed in latest mortgage application data, as new purchase applications saw one of the largest weekly declines in the past ten years.

- Composite mortgage applications fell -8.9% (sa) last week, extending the -8.5% decline in the previous week as they continued to reverse strong increases seen earlier in January to highs since Apr 2022.

- Having last week written on housing activity green shoots implied by a trend increase in new purchase applications, this sharply reversed with a -14.4% drop (largest decline since one week in Mar 2020 and before that 2015) in a reminder of how volatile the data can be.

- Refis meanwhile fell -4.7% after -15.7% following a 69% two-week increase before that.

- Levels relative to 2019 averages: composite at 69%, new purchases at 64% and refis at 73%.

- The 30Y conforming rate fell 3bps to 6.21% to chip away at an 8bp increase in the week prior. The 6.16% in the week to Jan 16 was its lowest since Sep 2024 and before that Sep 2022.

- Mortgage swap spreads reversed about half of the previous week’s widening and are back close to multi-year lows. The 30Y rate to the average 10Y swap rate over the week was 235bp vs a recent low of 233bp (it compares with a peak of 315bp in May in post-tariff disruption, an average 285bp in 1Q25 and 302bp in 2024).

- Compared to August when US Tsy Sec Bessent talked on wanting to see flat or lower mortgage spreads, this swap rate spread has narrowed nearly 60bp, or 43bps to 198bps for the 10Y Treasury yield equivalent.

- Narrowing has been supported by Fannie Mae and Freddie Mac increasing their retained portfolios ahead of a potential IPO, with MBS spreads then tumbling early in January after Trump ordered $200bn in MBS purchases.

OUTLOOK: Price Signal Summary - Bear Threat In Bunds Remains Present

- In the FI space, the trend outlook in Bund futures remains bearish and recent gains appear to have been a correction plus this week’s move down reinforces a bearish theme. Attention is on support at 127.51, the Jan 23 low, where a break would strengthen the bear theme and open 127.13 next, the Jan 6 low. Key short-term resistance to watch is 128.58, the Jan 19 high. For bulls, a breach of this hurdle would reinstate the recent uptrend.

- A bearish theme in Gilt futures remains intact. Recent weakness has resulted in a break of the 20-day EMA. Note too that price is trading below 91.31, a trendline support drawn from the Nov 19 low. The breach of the trendline undermines the recent bull theme and highlights potential for a deeper retracement with sights on the 90.00 handle next. Initial resistance is at 91.35, the 20-day EMA.