OIL PRODUCTS: Gasoline Cracks Pull Back from Previous Gains

Gasoline cracks are pulling back to reverse some of the recovery seen earlier this week. The Apr US gasoline crack is down from around 36$/bbl at the end of Jan to 32.9$/bbl but still above the lows around 31$/bbl seen on 17 Feb.

- Weak demand and healthy supplies are weighing on prices despite the strong US refinery maintenance season and ongoing concern for Russia product outputs. Russian oil output has maintained stronger than expected so far following on from EU and G7 sanctions which came in to effect on 5 Dec for crude and 5 Feb for products.

- US gasoline crack down -1.2$/bbl at 33.05$/bbl

- US ULSD crack down -0.3$/bbl at 40$/bbl

- EU Gasoline-Brent down -1.3$/bbl at 11.36$/bbl

- EU Gasoil-Brent up 0$/bbl at 25.32$/bbl

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Equity Roundup: Near Best Levels Since Mid-Dec'22

Major indexes continue to extend gains over last few minutes, eminis nearing last Wed's best levels since mid-December. Carry-over bid from Fri for Information Technology (general support following headlines of large, ongoing layoffs) and Communication Services and sectors. SPX eminis currently trades +34.5 (0.87%) at 4022.25; DJIA +203.43 (0.61%) at 33576.53; Nasdaq +149.9 (1.3%) at 11289.96.

- SPX leading/lagging sectors: Information Technology (+1.59%) outperforming, lead by semiconductor makers (AMD +7.59%, QCOM +4.57$, Micron +4.16%, Nvidia +4.09%). Communication Services (+1.2%) underpinned by interactive media and entertainment names: Netflix (NFLX) up another +3.1% after reporting huge subscriber addition in 4th quarter last wk (+7.66 million vs. 4.57 million est), TTWO +2.12, Warner Bros +1.73%.

- Laggers: Materials (-0.38%), Real Estate (-0.10%) and Utilities (+0.16%) sectors underperformed, metals and mining names weighing on the former: Freeport McMoran (FCX) -2.0%, Newmont Mining (NEM) -1.63%, specialized REITs weighing on Real Estate.

- Dow Industrials Leaders/Laggers: Salesforce (CRM) +4.88 at 156.13, Apple (AAPL) +2.55 at 140.42, Microsoft (MSFT) +1.80 to 242.02 after annc plan to lay off 10,000 employees last wk. Laggers: Visza (V) -0.32 at 223.99, PG -0.20 at 142.7, Verizon (VZ) +0.06 at 40.06.

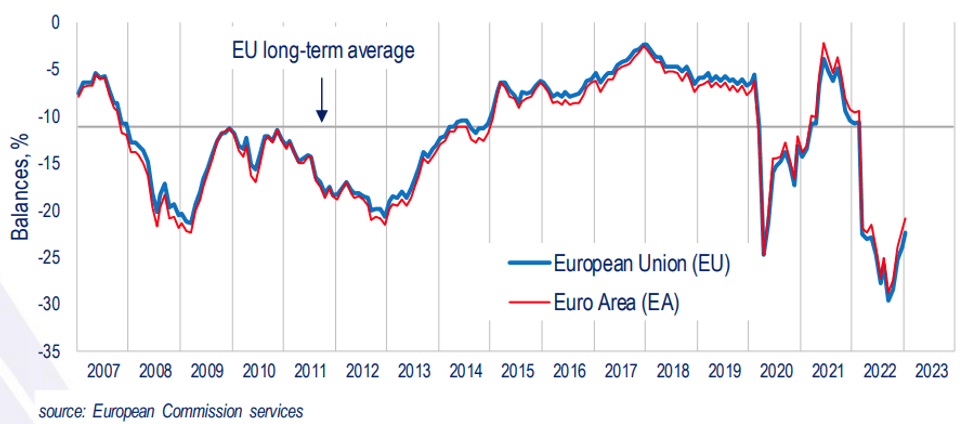

EUROZONE: Flash Consumer Confidence Higher as 2023 Outlooks Improve

EUROZONE JAN CONSUMER CONF (FLSH) -20.9 (FCST -20); DEC -22.0

- The eurozone January flash consumer confidence index ticked up to -20.9, up 1.1 points on December, remaining 0.9 points below expectations. This signals a fourth consecutive month of improvements after having collapsed to a record low of -28.7 in September 2022.

- Further details will be released in the final print and economic sentiment indexes released next Monday. Government energy bill support is driving the bulk of improvements in consumers' outlooks, yet whether this filters into higher consumer spending remains uncertain.

- This week's slew of sentiment data (Germany on Tues, Italy on Thurs and France on Fri) will add more colour to the eurozone outlook, whereby the propensity to buy subindices will carry higher significance.

- Flash PMI data is also set to see minor upticks across the board, signalling only mild contractions to kick off 2023. The eurozone index remains severely depressed and as such improvements in consumer confidence translating into recovery in demand remains yet to materialise.

MNI: EUROZONE JAN CONSUMER CONF (FLSH) -20.9 (FCST -20)

- MNI: EUROZONE JAN CONSUMER CONF (FLSH) -20.9 (FCST -20)