NATGAS: Gas Prices Follow Oil Lower On Hopes Of US-Iran Deal

Natural gas sold off on Wednesday in line with oil prices as hopes again grew that there would be a ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

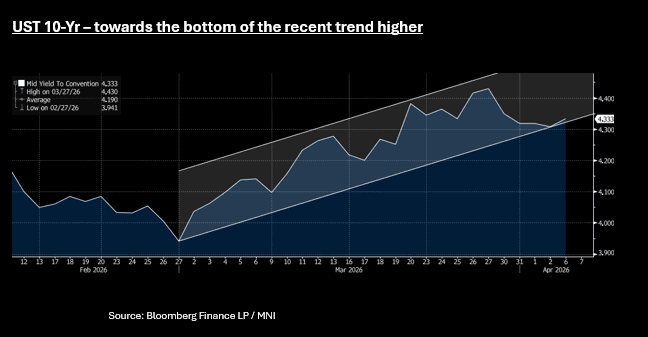

US TSYS: Yields Maintain Recent Ranges Ahead of Trump Deadline

Bonds are seemingly in a holding pattern ahead of the Trump Tuesday deadline with Iran. The yield movements were modest with the long end down 1-2bps on low volumes.

- The 2-Yr was up +.08bps at 3.851%

- The 5-Yr was up down -.03bps at 3.984%

- The 10-Yr was down -1.3bps at 4.333%

- The 30-Yr was down -2.1bps at 4.888%

The 10-Yr has is towards the bottom end of the recent up trend, seemingly treading water ahead of 'what happens next'. Instinctively, the inflationary build in data hasn't begun yet and has the potential to show up meaningfully in the next month.

March's ISM Services survey was mixed, with the headline PMI index decelerating just slightly more than anticipated at 54.0 (54.9 expected, 56.1 prior), but large divergences in subcomponents including worryingly high price pressures and weak employment amid some impact from the conflict in the Middle East apparent overall.

The Employment reading was substantially weaker than consensus at 45.2 (51.0 expected, 51.8 prior. It was the poorest since December 2023, and looks to be at odds with the strong gains in Marchs' employment report across multiple services categories. Prices paid meanwhile saw their biggest jump since August 2012, by 7.7 points to 70.7 (67.0 expected, 63.0 prior), to the highest since October 2022.

Two overnight auctions (US$89bn 13-week and US$77bn 26-week) both saw a modest tick up in the Bid to Cover.

The 10-Yr US bond future has opened in Asia up just +01 at 110-27, as momentum indicators continue be broadly neutral.

MNI: MNI JAPAN FEB HOUSEHOLD SPENDING -1.8% Y/Y; JAN -1.0%

- MNI JAPAN FEB HOUSEHOLD SPENDING -1.8% Y/Y; JAN -1.0%

- JAPAN FEB HOUSEHOLD SPENDING +1.5% M/M; JAN -2.5%

AUSSIE BONDS: Futures Higher After Break, Iran Deadline To Overshadow Data Today

The early bias in Aussie bond futures is higher, after the Easter break (onshore markets were out last Friday and yesterday). 10yr (XM) are up 94.98, +4.5bps firmer. 3yr (YM) futures are +3.5bps to 95.31. Broader ranges are still holding, recent lows in the 10yr just under 94.80, while the early April spike stopped just short of the 50-day EMA resistance point, which now rests near 95.10. Market focus is firmly on the US Tuesday evening Iran deadline (8pm ET), where Trump has stated if a deal is not reached Iranian energy infrastructure will be hit.

- US Monday trade saw oil prices finished up, which has continued in the first part of Tuesday trade (although WTI is sub recent highs above $115/bb). US equity sentiment was firmer in Monday trade. US Tsy futures edged a little higher (TY1 tracking near 110-27 currently), but remained with recent ranges, likewise for US Tsy yields. There was some yield support on Friday post the NFP beat.

- ACGB yields sit lower, down around 4.5-6bps, with the front end slightly leading in the first part of Tuesday trade. The 3yr is back to 4.66%, while the 10yr is near 4.98%.

- On the data front today we have the final S&P Global Services PMI print for March, while the Melbourne Institute inflation measure for March is also out. March ANZ-Indeed job ads also print, along with Feb household spending. The spending outcome is expected to be similar to Jan, with a 0.2%m/m and 4.6%y/y rise projected. Consumer sentiment measures plunged during March as the Iran conflict unfolded, but the Feb data will be too early to show any meaningful impact.