US TSY OPTIONS: FVX5 110.50 Calls Lifted

Sep-04 09:45

Recent trade in the FVX5 110.50 calls saw paper pay 0-19+ on 5K.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Tech Focus: USD Index at Key Inflection Point

Aug-05 09:41

The USD Index remains in a bear cycle and in July pierced a key long-term support at 96.55 - a trendline drawn from the May 2011 low. Trend signals highlight a number of important technical conditions.

- On a monthly, weekly and daily scale, an oversold condition has been highlighted .

- This does not mean that a trendline break (if confirmed) isn’t important and that the downtrend cannot extend.

- However, the oversold position does raise the possibility that either; a correction unfolds soon, or that the pace of the trend slows down.

- As is always the case in such situations, the momentum/oversold position is merely a warning sign for chartists. A reversal signal in price is required to highlight a base.

- July could prove to be a key month. Based on the close, a bullish engulfing candle pattern has developed.

- This is regarded as a strong reversal signal and the fact that it has occurred at the trendline, strengthens the importance of the pattern.

- Furthermore, it also suggests that the daily, weekly and monthly time scales are in sync - a bullish signal.

- Key support is at the July low of 96.38 and this price point represents an important pivot point.

BELGIUM T-BILL AUCTION RESULTS: TC Results

Aug-05 09:38

| Maturity | Nov 13, 2025 | Feb 12, 2026 | Jul 9, 2026 |

| Amount | E1.2bln | E903mln | E806mln |

| Target | E2.6-3.0bln | Shared | Shared |

| Previous | E1.2bln | E907mln | E1.801bln |

| Avg yield | 1.919% | 1.947% | 1.948% |

| Previous | 1.898% | 1.916% | 1.910% |

| Bid-to-cover | 2.28x | 2.71x | 2.62x |

| Previous | 2x | 1.67x | 1.82x |

| Previous date | Jul 08, 2025 | Jul 01, 2025 | Jul 08, 2025 |

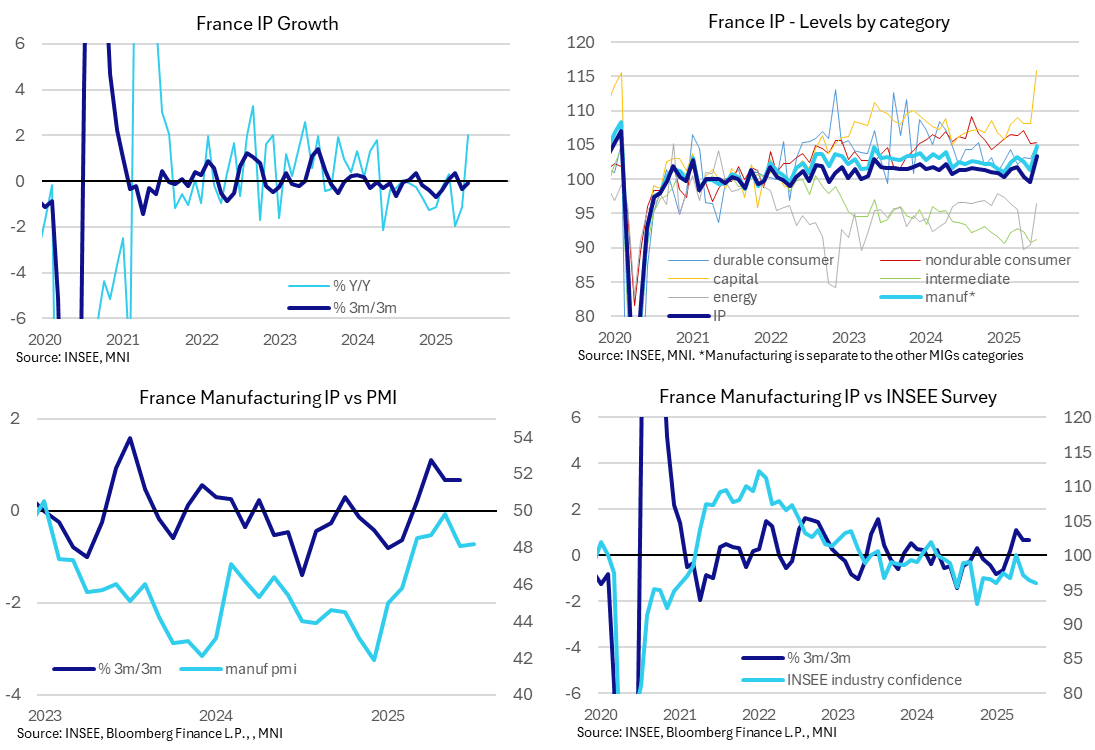

FRANCE DATA: June IP Surge At Least Partially Due To One-Offs; Weak Outlook

Aug-05 09:38

French industrial production was far stronger than expected in June as it surged 3.8% M/M driven in large part but not entirely by catch-up in aeronautical and space construction. Despite that jump, IP fell -0.1% Q/Q in Q2 after 0.1% in Q1 (admittedly with manufacturing at a stronger 0.7% Q/Q) and industrial indicators look soft ahead.

- IP surprisingly surged 3.8% M/M in June (cons 0.6) after -0.7% M/M in May (revised from -0.5%) and a heavy -1.4% M/M in April.

- It came as manufacturing production jumped 3.5% M/M in June (cons 1.2) after -1.2% in May along with a helping hand from the remaining category of "mining & quarrying, energy, water supply and waste management" (about 18% of total IP) rising 5.0% M/M after 1.7% in May.

- Explaining the former the press release added "The exceptional increase in [the transport] sector was mainly driven by the manufacture of "other transport equipment" (aircraft, shipbuilding, rail, etc.) " (+26.7% after +1.8%), and more specifically by aeronautical and space construction. This is explained by a catch-up over the month of delays accumulated over the quarter and the lifting of constraints on supply chains for certain companies in this sector".

- As such, manufacturing of transport surged 16.6% M/M after 0.3% but the separate category of manufacturing of machinery & equipment goods also increased a strong 4.2% M/M after -1.0% so it wasn't in isolation.

- For a slightly broader take, the alternate classification of capital goods production increased 7.2% M/M for its largest monthly increase since July 2020.

- Highlighting the weak backdrop seen in previous months, despite this (presumably largely one-off) strength in June, IP still fell -0.1% Q/Q non-annualised in Q2 after 0.1% in Q1. Manufacturing was at least stronger at 0.7% in Q2 after 0.2% in Q1.

- It clearly sees production heading into Q3 on better momentum, depending on the extent of the payback seen in July, although broader manufacturing prospects don't appear optimistic. The INSEE manufacturing confidence indicator fell for a third consecutive month to 96.0 in July and the manufacturing PMI was roughly unchanged at 48.2. The press release for the latter noted: "the lack of movement in the headline index masked a host of adverse signals seen in the survey's sub-indices. Most notable was a sharp and accelerated drop in new orders".

- A reminder when it comes to French IP however that France has the lowest industry share of GVA amongst the big five Eurozone countries. The 14% in 2024 compared with 23% in Germany (highest) and 19% in Italy (second highest).