JGBS: Futures Lagging Tsys, 20yr Debt Auction Digested Smoothly, BoJ Speech Thur

Futures sit at 136.29, -0.4 versus settlement levels, little changed in the post lunch break period at this stage. We remain close to recent highs, with US Tsy futures trading with a positive bias (all eyes on the 10yr yield and whether we can break under 4.00%), imparting some positive spillover (although JGBs are lagging). The 20yr auction was digested relatively smoothly by the market. Domestic political uncertainty continues, with lack of agreement on holding the PM election on Oct 21, although this isn't weighing on JGB sentiment at this stage.

- The current rally in futures comes in the context of the firm downtrend that’s dominated prices since mid-September. Key short-term resistance has been defined at 137.30, the Sep 8 high. The latest sell-off, however, resulted in a break of support at 136.19, the Sep 4 low and a bear trigger.

- We would expect JGB futures to lag US moves. The US-JP 10yr government bond yield spread is down a further 2bps today to +235bps, close to recent lows.

- The outright 10yr JGB yield is little changed at 1.66%, while the 20 and 40yr tenors are off 2bps, the 30yr off 3.5%. The 20yr yield is just under 2.70%. The auction saw a bid to cover ratio of 3.56 versus a 12 month average of 3.25.

- Political uncertainty continues around who will be the new PM, with headlines crossing a short while ago that the parliamentary committee has failed to agree to hold the new PM election on Oct 21 (which was speculated on yesterday). Meetings between the LDP and minor parties are continuing today.

- Looking ahead, Aug core machine orders print tomorrow. Note we also hear from BoJ Board member Tamura.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NZD: Asia Wrap - NZD/USD Doing Some Work Below 0.6000

The NZD/USD had a range of 0.5947 - 0.5966 in the Asia-Pac session, going into the London open trading around 0.5965, +0.20%. US Equities traded sideways as the market turned its focus towards the FOMC this week and what the potential upcoming cutting cycle could look like. The NZD topped out just below 0.6000 as momentum higher stalled. The USD though is still looking vulnerable, which continues to support the NZD. A close back above 0.6000 would negate any semblance of the downward pressure it was exhibiting, but for those that have a bearish view this remains a decent entry point to express that. We might have to wait for the FOMC to get some clarity as CFTC Data shows positions are light with conviction obviously low.

- (Bloomberg) -- New Zealand’s services industry contracted for an 18th straight month in August, suggesting that an economic rebound in the third quarter could be more sluggish than expected. Reserve Bank Governor Christian Hawkesby said last week that early indicators of third-quarter activity gave him confidence of an economic rebound, and he reiterated that policymakers’ central projection is that the Official Cash Rate will be cut to 2.5% by the end of the year

- "NZ TREASURY SEES UNCERTAINTY OVER PACE OF 2H ECONOMIC RECOVERY, NZ TREASURY COMMENTS IN FORTNIGHTLY ECONOMIC UPDATE" - BBG

- China Weak Property Data Continues: Property Investment YTD YoY and Residential Property Sales YoY declined more than expected in August. Property Investment YTD YoY fell -12.9%, its largest monthly decline. It has not recorded a positive monthly result since March 2022. Residential Property Sales YoY declined -7.0% in August, the worst result for 2025. It has not recorded a positive monthly result since July 2023.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5825(NZD1.01b Sept 17), 0.5900(NZD860m Sept 17), 0.6250(NZD427m Sept 17) - BBG

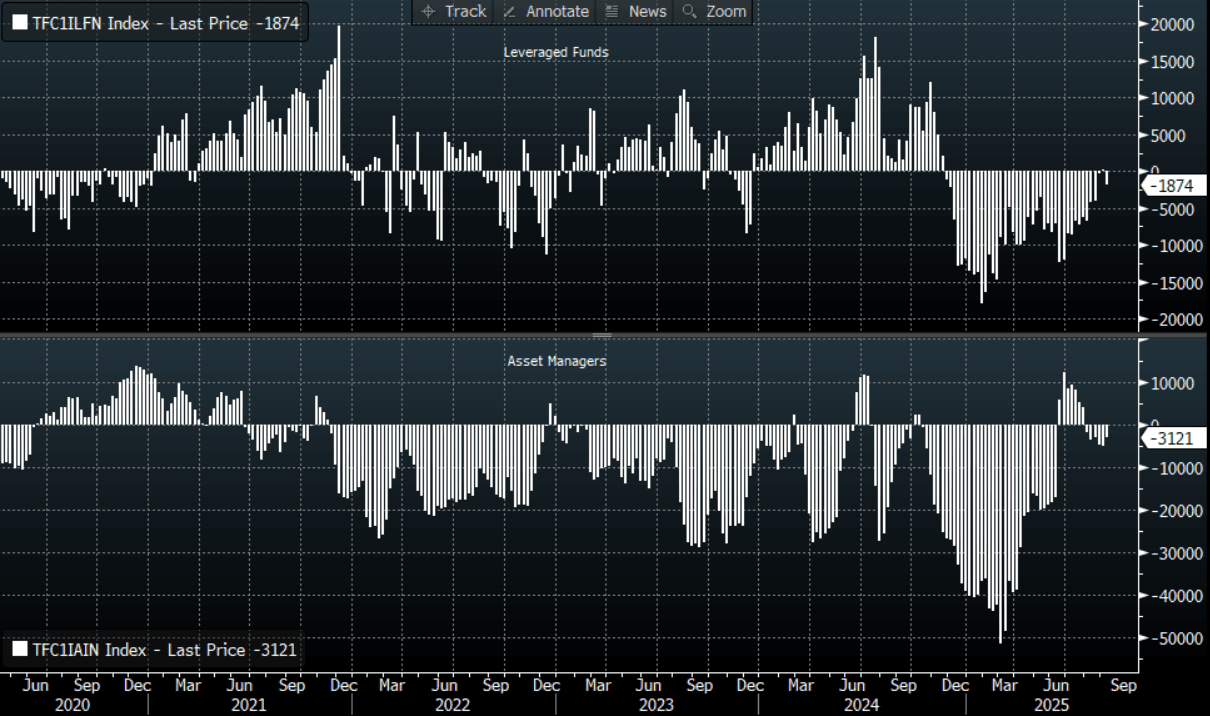

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -5127(Last -4743), the Leveraged community have completely exited their short and have turned a fraction long +285(Last -225)..

- AUD/NZD range for the session has been 1.1150 - 1.1176, currently trading 1.1175. The Cross is consolidating above 1.1100, dips back towards 1.1000/1.1050 should be supported now. A break above the multiple highs towards the 1.1200 area is needed to regain the momentum higher.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Closed Cheaper Ahead Of A Busy Week Of Local Data

NZGBs closed 2-4bps cheaper, with the 2/10 curve steeper.

- Swap rates closed 1-3bp higher.

- (Bloomberg) “Economic activity is expected to pick up over the second half of 2025 but there is uncertainty surrounding the pace of recovery, the Treasury Dept. says in its Fortnightly Economic Update released Monday in Wellington.”

- The focus of the week will be on Thursday’s Q2 GDP data release. Bloomberg consensus is in line with the RBNZ’s August forecast of -0.3% q/q bringing the annual rate to flat after declining 0.7% y/y in Q2. 25bp rate cuts are expected at both the October 8 and 26 November meetings.

- August monthly price series including food, electricity, rent, petrol and travel print on Tuesday. Food price inflation has been picking up. There is a risk that Q3 CPI inflation exceeds the 3% top of the RBNZ’s target band. The bank is forecasting 3% for the quarter.

- On Wednesday, Q3 current account data is out and the deficit is expected to narrow to 4.8% of GDP but with it widening to $2.7bn from $2.32bn in Q2.

- There is also Westpac Q3 consumer confidence on Wednesday.

- RBNZ dated OIS pricing closed little changed across meetings. 22bps of easing is priced for October, with a cumulative 40bps by November 2025.

CHINA: Bond Futures Rise Monday

- China's bond futures higher Monday, with the 10-Yr leading.

- Up +0.10 the 10-Yr is at 107.78, below the 20-day EMA of 107.90.

- The 2-Yr future is lower by -0.01 at 102.35, to remain below the 20-day EMA of 102.38.

- The 10-Yr CGB is lower by -1bp at 1.79%