IDR: FTSE Russell HLines Ignored by Broader Strength, USDIDR Down Again

Feb-10 02:33

- Late yesterday FTSE Russell stated that it will postpone a review planned for March following feedback from an investment advisory committee considering "adverse turnover and the uncertainty in determining the accurate free float percentages of Indonesian securities." The postponement will result in a freeze of any new inclusions of stocks into its indexes, or any alteration to existing holdings. This comes following the announcement from MSCI of similar actions.

- MSCI and FTSE indexes are widely used as benchmarks for investors and are tracked by billions of dollars in passive funds, meaning their decisions can drive capital flows.

- Markets haven't reacted to this headline, given broader equity strength in the region. The JCI is up +0.70%, as the NKY climbs +2.5% and the HSI up +1.2%

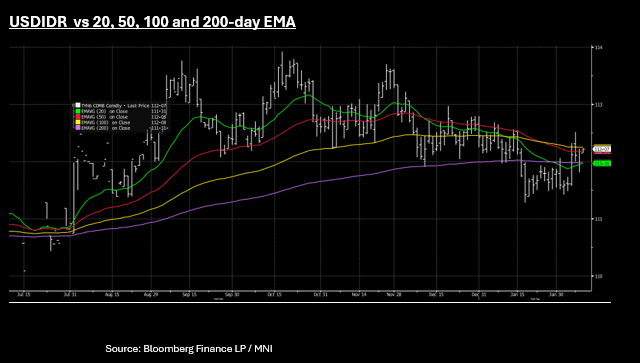

- USDIDR is lower for a second consecutive day and back below the key resistance level of 16,800. USDIDR is down -18 Tuesday at 16,787 for Rupiah gains of +0.9%.

- This takes USDIDR back below the 20-day EMA of 16,808. Downside resistance comes from the 50-day EMA at 16,774 with momentum indicators are broadly neutral.

- The volatility in February has seen INDO 5-Yr CDS higher, though the moves have been modest relative to the falls in equity. From the January lows of +67bps, INDON 5-Yr CDS reached a February high of +80bps, but has moderated back to +76bps since and in line with the 1-Yr average.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

Jan-10 22:45

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.890 @ 16:40 GMT Jan 9

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

MNI: MNI TEST 02, Please Ignore

Jan-09 23:36

Test Test TEST

MNI: MNI Test, Please Ignore

Jan-09 23:30

Test, ignore