POWER: French Hydro Stocks See Sharpest Fall Since March

Nov-17 15:56

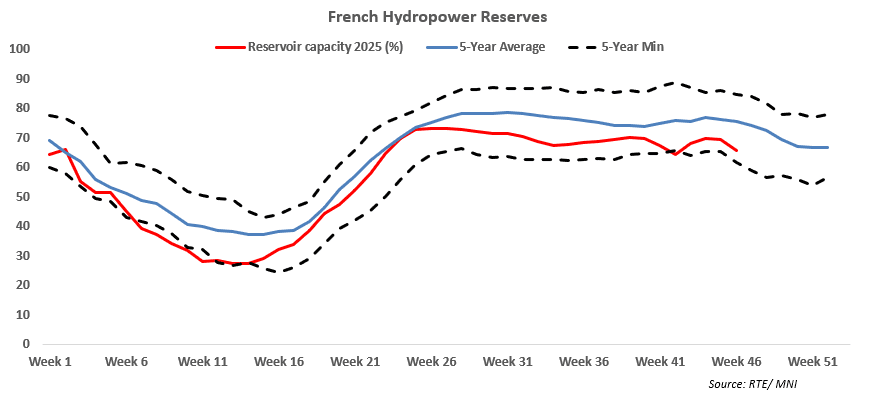

French hydropower reserves last week – week 46 – declined by 3.5 percentage points to 65.8% of capacity, marking the sharpest decline since late March, RTE data showed.

- The sharp decline was despite lower power demand and high precipitations last week. Stocks declined by 0.2 points the week prior.

- The deficit to last year’s level widened to 12.9 points, from 12.1 points the week before.

- The deficit to the five-year average widened sharply to 9.8 points, from 7 points the week before.

- Power demand in France declined sharply by 2.98GW to 46.26GW.

- Hydropower generation from reservoirs last week declined by 685MW to 2.27GW while output from pumped storage was stable at 1.02GW. Run-of-river generation declined by 918MW to 3.87GW.

- Nuclear generation in France last week edged up by 180MW to 43.86GW.

- Combined onshore and offshore wind generation increased by 1.56GW to 788GW.

- Precipitation in Grenoble near France’s hydro-intensive region last week totalled 93mm, well above the seasonal average of 25.5mm.

- Looking ahead, the latest weather forecast for Grenoble for this week suggests precipitation to ease to 7.2mm, below the seasonal average of 22.9mm.

- The latest two-week ECMWF weather forecast for Paris suggests mean temperatures between -0.5C and 7C, below the seasonal normal.

- France’s hydro balance is forecast to end this week at -278Wh. The balance is forecast to widen to 162GWh as of 2 December.

- Wind output in France for the remainder of this week (Tues-Sun) is forecast at 3.68GW to 9.75GW during base-load hours, according to SpotRenewables.

- French nuclear availability was at 84% of capacity as of Monday morning.

- French nuclear reactor capacity is forecast at 52.33GWh/h this week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: US Week Ahead Headlined By Delayed CPI Report On Friday

Oct-17 20:51

- The September US CPI report will be released on Friday, delayed amidst the government shutdown but with the BLS making a special exception on social security payment considerations.

- Bloomberg consensus looks for headline CPI inflation at a rounded 0.4% M/M after 0.38% back in August and for Y/Y inflation to firm two tenths to 3.1% for what would be its highest since May 2024.

- Core inflation is seen at a rounded 0.3% M/M after 0.35% in August (exceeding the median unrounded estimate of 0.31%) and 0.32% in July. It’s expected to see core CPI inflation hold at 3.1% Y/Y having in August increased to its highest since February.

- Core details should see focus on both goods and services angles: underlying goods inflation has clearly firmed in recent months on tariff pressures although the median increase has currently seen a peak back in June, whilst services will be watched for any spillover after some strong recent non-housing readings.

- The report will come within the FOMC blackout period ahead of the Oct 28-29 decision, with a 25bp cut fully priced and likely needing a large surprise to alter this.

- As for broader inflation details, Fed Chair Powell this week confusingly suggested that we will have the September PPI report but the BLS had previously said “No other releases will be rescheduled or produced until the resumption of regular government services”.

US DATA: Latest Jobless Claims Estimates During The Shutdown

Oct-17 20:30

As noted earlier, MNI estimates initial jobless claims at a seasonally adjusted 218k in the week to Oct 11 and continuing claims at a seasonally adjusted 1929k in the week to Oct 4.

- To give a better idea of sensitivity around these estimates, which rely on estimates for some missing states, we note the below analyst estimates:

- Goldman Sachs have a central estimate of 217k for initial claims in a range of 211-225k, whilst they see continuing claims at 1917k in a range of 1885-1930k.

- JPMorgan meanwhile also see 217k for initial claims whilst they see continuing claims as having held constant at 1927k.

NATGAS: Venture Global in Talks with Ukraine for more LNG Deliveries, Reuters

Oct-17 20:28

Ukraine is seeking more cargoes from Venture’s Plaquemines facility as the embattled nation approaches the winter heating season, according to Reuters sources

- Venture is in talks with Ukraine’s DTEK to procure more LNG cargoes after a year of gas infrastructure attacks by the Russians.

- Venture Global CEO Michael Sabel met with President Volodymyr Zelenskiy on Thursday October 16.

- DTEK signed an agreement in 2024 for an undisclosed amount of LNG from the facility, as well as 2 mtpa from Calcasieu Pass Phase 2 currently under construction.

- Plaquemines currently has spare capacity to deliver more cargoes to Ukraine on the spot market, per Reuters.

- Plaquemines now sends out the second highest LNG volume in the US, with feedgas demand averaging 3.45 bcf/d according to MNI figures.