US BASIC INDUSTRIES: Freeport: 3Q25 Results

Modest credit positive - FCX will hold a call on 11/18/2025 to update on the GBC incident. A timeline on the restart of GBC will be crucial for FCX's profitability. In the interim, we expect that higher copper and gold prices will benefit sales from its Americas mines, mitigating margin and leverage deterioration.

• Revenue was ahead of street consensus at $7B ($6.7B est.), and was +3% YoY.

• Copper and gold sales were 1% and 4% below the company's July guidance.

• EBITDA increased by 5% YoY and margins increased by 1ppt to 41%.

• FCF was $392M compared to $454M in the prior year quarter and the company did not buy back any stock ($3B auth. remaining).

• Gross and net leverage ended the quarter at 0.9x and 0.5x (0.6x and 0.2x excluding PTFI debt), stable sequentially.

• FY25 pre-dividend FCF is expected to be $1B; assuming prices of $4.75/lb for copper, $4,000/oz for gold and $25/lb for molybdenum in 4Q25.

• The company reiterated restarting the Big Gossan and DMLZ mines in 4Q25 and a phased restart of GBC in 2026, having a 35% impact on estimated production for 2026.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

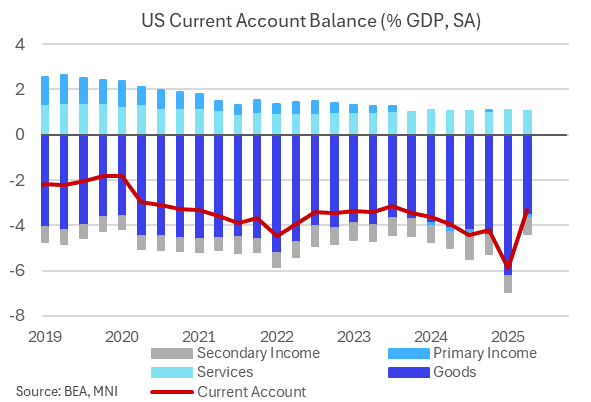

US DATA: Current Account Weighed By Trade Deficit, Weaker Net Investment Income

The US current account deficit was a little smaller than expected in Q2 2025, at $251B, vs $257B expected (prior revised to $440B from $450B - all figures rounded).

- This was the smallest deficit in nominal terms since Q4 2023, but comes after a record shortfall the prior quarter. The implied 3.3% of GDP deficit was the smallest since Q3 2023, after 5.9% in Q1. The swings were of course exaggerated primarily by tariff-related trade shifts, but when we average the two quarters out, the deficit comes out at $346B.

- That's wide by historical standards (the prior 8 quarters averaged $254B), with the difference again being the goods trade deficit of $368B on average the first half of the year ($284B 8-quarters prior average). The services trade surplus averaged $80B in H1, vs around $74B the prior 8 quarters, so a slight improvement there in line with the historical average, even as the primary and secondary income accounts showed slightly smaller deficits - see chart as % of GDP.

- We get August advance goods trade data on Thursday - it's expected to see a smaller deficit of $95B vs a surprisingly high $103B in July. Consensus for the current account sees a small narrowing over the coming quarters, from an average 4.6% of GDP in H1 to 4.0% by mid-2026.

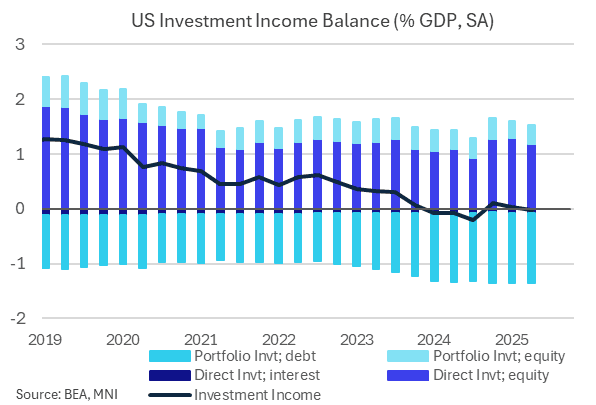

- One key to the current account outlook is portfolio income: as US yields have risen, the % of GDP paid out to the rest of the world has neared 2.0% (1.8% in the latest quarter) of GDP from 1.5% in 2022, while credits received have been static at 0.6%, reflecting the negative international portfolio investment position.

- While this has been offset by an improvement in net direct investment income, that widening in the portfolio category accounts for about 0.4-0.5pp of the current account deficit, and doesn't look likely to abate in the near future. The investment income balance used to represent a strong surplus for the US current account (+1% of GDP) but has been flat for the last couple of years.

EURJPY TECHS: Trend Needle Points North

- RES 4: 177.08 2.000 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 3: 175.43 High Jul 11 ‘24 and a key medium-term resistance

- RES 2: 174.86 1.764 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 1: 174.50 High Sep 19

- PRICE: 174.30 @ 20:15 BST Sep 23

- SUP 1: 173.14/171.93 20- and 50-day EMA

- SUP 2: 170.97 Low Aug 14

- SUP 3: 169.73/45 Low Jul 31 / 23.6% of the Feb 28 - Jul 28 bull leg

- SUP 4: 168.46 Low Jul 1

The trend set-up in EURJPY is unchanged, it remains bullish and price is trading at its recent highs. The cross last week breached resistance at 173.97, the Jul 28 high and a bull trigger. This confirms a resumption of the medium-term uptrend and maintains the price sequence of higher highs and higher lows. Sights are on 174.86, a Fibonacci projection. On the downside, first support to watch lies at 173.14, the 20-day EMA.

US TSYS: Off Lows, Little New From Fed Chair Powell Outlook

- US Treasuries look to finish near late session highs after holding lower/narrow range for much of the session.

- Tsys gained slightly after flash PMIs come out slightly lower than expected: flash US PMIs brought a 2-month low for Manufacturing at 52.0 (52.2 consensus, 53.0 prior) and a 3-month low for Services at 53.9 (54.0 consensus, 54.5 prior), but both readings were pretty much in line with consensus and suggest an economy in expansionary territory.

- Fed speak elicited muted reactions: Atlanta Fed Bostic's longer-run dot suggests limited impetus to cut further, while Chicago Fed Goolsbee calls current policy "mildly restrictive" and points to a neutral rate 100-125bp lower than current rates.

- Even Chair Powell's outlook didn't deviate much if at all from last week's FOMC press conference as "two-sided risks mean that there is no risk-free path." Treasuries gained after around Chairman Powell speech as block buy over 10k TYZ5 added impetus to move.

- Little reaction in Tsy futures after the latest $69B 2Y note auction (91282CPB1) comes out on the screws: 3.571% high yield vs. 3.571% WI; 2.51x bid-to-cover vs. 2.69x prior.

- Light data again tomorrow: New Home Sales and Building Permits scheduled. SF Fed Daly economic outlook, moderated Q&A after the close. Main focus is on Thursday's heavy data drop: Personal Consumption, GDP, Durables/Cap Goods, and weekly claims.