EUROPEAN INFLATION: France December HICP Expected To Moderate

France will kick off the main week for the Eurozone December flash inflation release today at 07:45 GMT / 08:45 CET, following Spain, Belgium and Portugal data from last week. Consensus for HICP currently sits at 0.7% Y/Y, down from 0.79% seen in November vs the initially reported 0.83%.

Analyst views:

- Goldman Sachs see France 0.7% headline; “core inflation to tick up to 1.3%yoy, reflecting broadly sideways services but higher goods inflation on a year-over-year basis. We expect a 20%mom nsa increase in airfares, a -5%mom nsa drop for package holidays, and broadly stable accommodation services. We see both garments and footwear stronger in sequential terms compared to last December. Outside of core, we look for energy inflation to fall to -6.0%yoy from -4.4% in November, processed food inflation to stay at 1.6%yoy and unprocessed food inflation stay unchanged at 1.3% as well.”

- Morgan Stanley see 0.8% headline as energy disinflation from lower pump prices offsets a modest rebound in services after weak airfares and accommodation in November.

The December flash PMI noted:

- “The latest survey data signalled an easing of cost pressures across France’s private sector economy. The rate of input price inflation eased on the month and was well below its long-term trend."

- "On the other hand, prices charged were virtually unchanged once again as strong competition for work reportedly restricted company pricing power. This was despite a renewed increase in factory gate charges, which rose at the quickest pace in 16 months.”

Bank of France December macroeconomic projections:

- Headline and core inflation seen at 1.2% and 1.4% in 2026 respectively, when factoring in government bills passed after the official projection deadline.

- “In 2027, headline inflation and inflation excluding energy and food are expected to remain unchanged at 1.3% and 1.6%, respectively. Inflation excluding energy and food should reflect private services prices, pushed up by growth in nominal wages. These projections also take account of the postponement until early 2028 of the introduction of EU ETS-2, leading to a downward revision of headline inflation for that year.”

- “The uncertainties surrounding inflation stem in particular from import prices (raw materials, exchange rates, increase in Chinese imports, etc.) in an uncertain international context.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Bull Channel Breakout

- RES 4: 1.4140 High Nov 5 and a key resistance

- RES 3: 1.4131 High Nov 21

- RES 2: 1.4051 High Nov 28

- RES 1: 1.3939/4016 Low Nov 28 / 20-day EMA

- PRICE: 1.3865 @ 16:35 GMT Dec 5

- SUP 1: 1.3853 Intraday low

- SUP 2: 1.3840 50.0% retracement of the Jun 16 - Nov 6 bull cycle

- SUP 3: 1.3812 Low Sep 23

- SUP 4: 1.3779 Low Sep 22

A bear theme in USDCAD remains intact and Friday’s strong sell-off reinforces a bear theme. The pair has breached an important support at 1.3942, the base of a bull channel drawn from the Jul 23 low. The break highlights a stronger bear cycle and signals scope for an extension towards 1.3840 next, a Fibonacci retracement point. Initial firm resistance to watch is 1.4016, 20-day EMA.

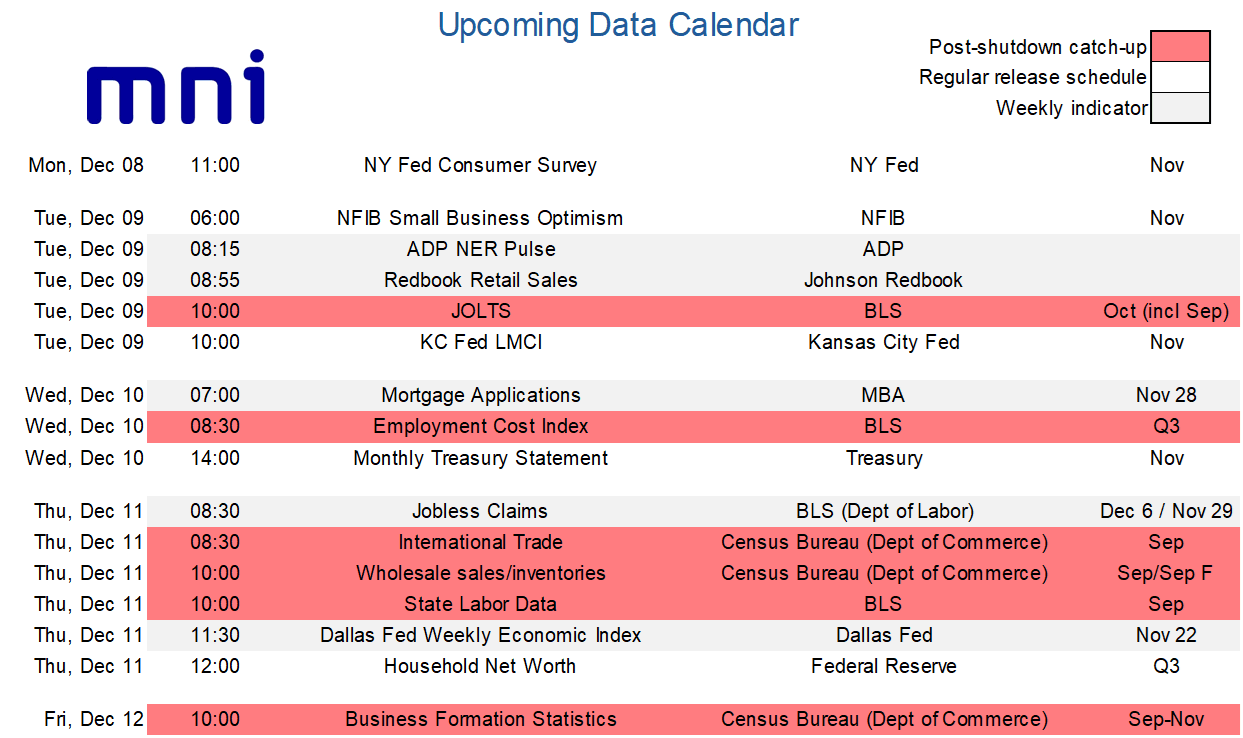

LOOK AHEAD: US Week Ahead: FOMC Decision Dominates, Post Shutdown Data Catch-Up

- Next week’s US calendar is dominated by the FOMC decision on Wednesday, with a third consecutive 25bp cut almost fully priced.

- Expect it to be a contentious meeting however, with many arguing for a pause not least whilst they’re still relatively in the dark on key official data releases following the government shutdown.

- Fed Chair Powell opted for a surprisingly hawkish tone at the late October press conference, highlighting a deeply divided committee on prospects for another cut in December.

- The “fog” had appeared to win out until NY Fed’s Williams, a senior permanent voter, gave unusually explicit guidance on still seeing room “for a further adjustment in the near term”. With no pushback from FOMC members or media briefings, it appears this message has approval from the core of the FOMC which should be enough to see a rate cut this month. The likely catalyst was the further increase in the unemployment rate to 4.44% back in September, although subsequent tracking suggests stabilization and jobless claims data don’t show any signs of deterioration.

- We’ll be looking for the number of hawkish dissents (we’d be surprised if anyone joins Miran dissenting for a 50bp cut) and expect a greater number to object to a cut in the 2025 dot plot, whilst the distribution of dots for 2026 should be in greater focus.

- As for the economic projections, we expect upward revisions to GDP growth but downward revisions to near-term core PCE inflation with tariff passthrough proving less severe than previously feared.

Aside from the Fed, we also receive two months worth of JOLTS data along with other delayed releases as the shutdown data backlog is slowly caught up.

AUDUSD TECHS: Bullish Impulsive Wave Extends

- RES 4: 0.6723 High Oct 21 ‘24

- RES 3: 0.6707 High Sep 17 and a key resistance

- RES 2: 0.6660 High Sep 18

- RES 1: 0.6649 Intraday high

- PRICE: 0.6630 @ 16:32 GMT Dec 5

- SUP 1: 0.6580/6533 High Nov 13 / 20-day EMA

- SUP 2: 0.6517 Low Nov 27

- SUP 3: 0.6466/21 Low Nov 26 / 21

- SUP 4: 0.6415 Low Aug 21 / 22 and a bear trigger

A strong impulsive bull wave in AUDUSD remains intact, having printed 10 consecutive sessions of higher highs. Recent gains have cleared a number of important short-term resistance points, strengthening a bull theme and highlighting scope for a continuation higher. Today’s rally has resulted in a breach of 0.6640, 76.4% of the Sep 17 - Nov 21 bear leg. This opens 0.6707, the Sep 17 high and key resistance. Key support to watch is at 0.6533, 20-day EMA.