FED: Former Fed General Counsel Alvarez on BBG TV [2/2]

Aug-28 16:41

- Q: What’s your advice now to the other Fed Bank presidents and other Governors?

- A: It is very difficult to prepare for something like this. I was a little surprised that the FHFA released this data that is confidential, personal information. It would be one thing for the FHFA to recommend an investigation but it is anything thing for the agency to release publicly private information. I would advise other board members and presidents to pay attention to what they are doing and if they are in a situation where they have multiple homes, that they make sure they have told the banks all about it so the banks have the opportunity to make adjustments if appropriate. I do not know how you otherwise prepare for something like this.

- Q: Hypothetically, suppose there is some evidence of a deliberate or inadvertent action on Lisa Cook’s part. Would you advise her to resign?

- A: That is a really difficult question. Inadvertent action I do not think is cause under the Federal Reserve Act. People make mistakes all the time. The real question is was the bank deceived in a material way? That depends on all the information, not just what is on the application. In a mortgage process, an application gets filed but the banks take many months to make decisions about loans and circumstances change but the application remains the same. As long as the bank knows what is going on, and has a view of the facts and can make an honest decision about the credibility/ability of the person to pay, then there isn't fraud.

- Q: Which would be worse for the institution, if Cook stayed on even if there was some fraud because it did not rise to the "for cause" level or if Donald Trump would be able to fire people at will?

- A: It is definitely worse for the institution if the president can fire a member of the board at will, or based solely on an allegation that is unproven or undemonstrated. In that situation there really is no independence of the Fed and its ability to act. That’s got to make markets uneasy because they then do not know if the fed is acting on the basis of data and what the economy is really doing, or if they are acting on behalf of the president. Having no cause is really the worst thing that could happen.

- Q: Are there any legal measures the Fed should take -- could take -- to protect its independence as an institution and shield itself from presidential pressure?

- A: There has been presidential pressure in the vocal sense for the entire history of the Fed. Presidents always make, or often make their views known on what monetary policy should be. But as long as the president allows the Fed to make his decisions based on the data and its own explanation of why it is making those decisions, as long as that is happening, I think there is independence in the Fed. I'm not sure the Fed can do anything more to preserve itself. It really does require some respect on behalf of the rest of the government, the President and Congress, to allow the Fed to make its decisions.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC: MNI BoC Preview-July 2025: Data Calls For Further Patience

Jul-29 16:39

We've published our BOC preview for this week's meeting - Download Full Report Here

- Data developments since the June meeting mean the Bank of Canada will maintain the overnight rate target steady at 2.75% for a third consecutive meeting on Wednesday.

- Better-than-expected labour market data and stubbornly high core inflation, combined with continued uncertainty over the US-Canada trade dispute, give the BOC impetus to wait until its next meeting in September before committing to further moves.

- While the BOC is likely to retain its easing bias, judging from market pricing, the question now is whether the BOC’s easing cycle is at an end after 225bp of cuts through March.

- We note that while most analysts still expect at least one further cut, median expectations of the terminal overnight rate as tracked by MNI have crept up to 2.25% from 2.125% since prior to the June meeting.

- The latest Monetary Policy Report is likely to include two tariff-related scenarios as in the previous round, with a less negative estimate for Q2 GDP and slightly higher core inflation.

- The policy statement should reflect this better-than-expected economic activity evolution as well, but once again we do not expect any firm forward guidance.

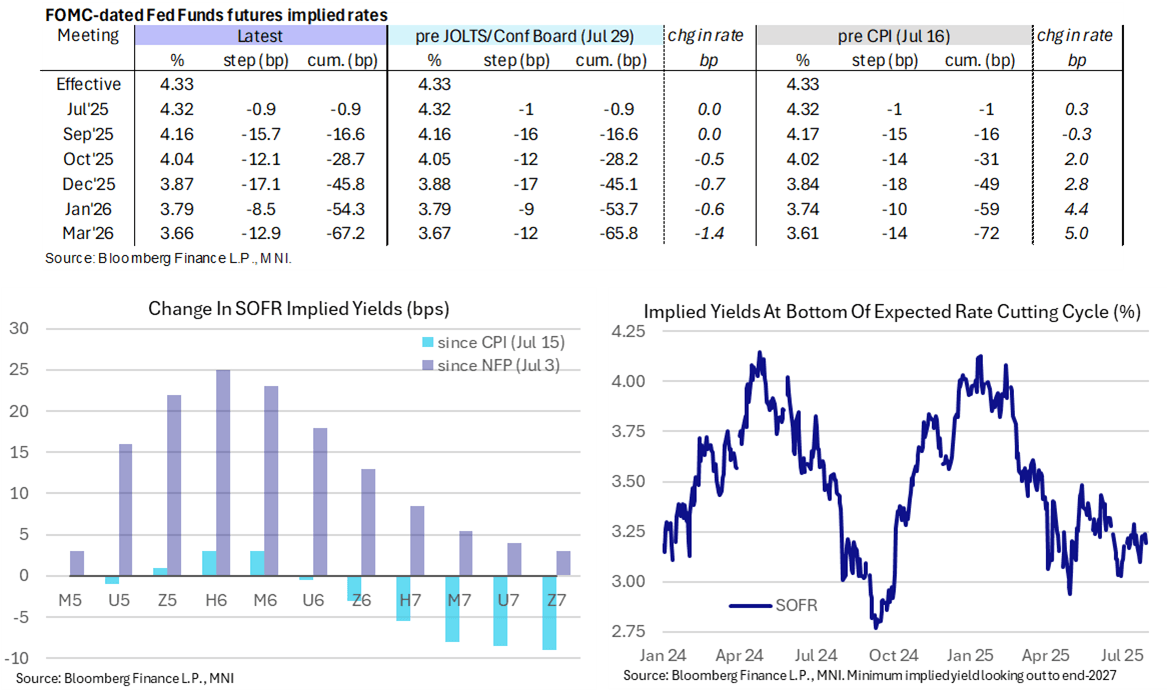

STIR: Soft JOLTS Report Mildly Adds To Day’s Dovish Shift Ahead Of FOMC Tomorrow

Jul-29 16:37

- Fed Funds implied rates continue to hold what was a marginally dovish reaction to a soft JOLTS report and mixed Conference Board consumer survey, which saw stronger than expected confidence but weaker labor differential).

- The Dec’25 implied rate is only 0.7bp lower post-1000ET data for -1.8bp on the day.

- Cumulative cuts from 4.33% effective: 1bp for tomorrow’s decision, 16.5bp Sep, 28.5bp Oct, 45.5bp Dec, 54.5bp Jan and 66.5bp Mar.

- The SOFR implied terminal yield of 3.195% (SFRH7) is 4.5bp lower on the day but only 1bp lower post the 1000ET data. It pushes it back towards the middle of the 3.1-3.3% range seen through July.

- Earlier in the day, trade and inventory data have left stronger GDP tracking for Q2 ahead of Thursday’s Q2 advance release (Atlanta Fed GDPNow revised up from 2.4% to 2.9%) but with soft domestic demand estimates (GDPNow sees PDFP closer to 0.7pp in Q2 after 1.6pps in Q1).

- MNI Fed Preview ahead of tomorrow’s decision: https://media.marketnews.com/Fed_Prev_Jul2025_With_Analysts_002622ac0e.pdf

OPTIONS: Expiries for Jul30 NY cut 1000ET (Source DTCC)

Jul-29 16:25

- EUR/USD: $1.1525(E765mln), $1.1550(E902mln), $1.1700-10(E1.1bln), $1.1800(E1.7bln)

- USD/JPY: Y147.50($878mln), Y148.25-30($989mln), Y148.65($945mln), Y149.00($853mln)

- AUD/USD: $0.6550(A$1.0bln), $0.6600-10(A$1.2bln)

- USD/CAD: C$1.3695-10($969mln), C$1.3770-75($1.7bln)