NEW ZEALAND: Food Prices Down Again, Gains Elsewhere Led By Utilities & Travel

New Zealand Dec food prices remained soft. We fell 0.3%m/m, after a -0.4% decline in Nov. This brings the y/y pace back to 4%, off 2025 highs of 5%. Other detail in the Dec price update generally showed positive m/m gains, particularly for air transport. Today's Dec print comes ahead of next Friday's Q4 CPI print. There is no consensus for this print yet, but the RBNZ had penciled in +0.2%q/q (after a 1.0% Q3 gain), which would leave the y/y outcome at 2.7% (prior 3.0%). There is also likely to be focus on non-tradables, which rose 1.1% in Q3. Given signs of a firmer growth backdrop in Q4 last year this segment will be watched for any early domestic inflation pressures.

- In terms of the detail for Dec prices, rents edged up 0.1%, while and electricity and gas posted further solid m/m rises (+1.5% and 1.9% respectively). Petrol at +0.1% slowed compared to prior months, while domestic and international air travel surged (+15.8 and 32.9% respectively). Accommodation services rose 0.7%m/m (versus +1.1% in Nov).

- Y/Y trends were mixed, strongest for utilities, but accommodation services is now +12.1%y/y.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Little Changed Despite Modest Post-Data Rally By US Tsys

NZGBs are unchanged despite US tsys finishing moderately richer, but off post data bests. Focus turned away from the 4.6% unemployment rate with possible assistance from that heavy -105k in Oct NFP. Rounding and already known higher survey error saw retrace gains.

- Retail sales growth was flat in October after rising 0.1% prior, a little softer than the expected 0.1% gain - core sales were significantly stronger than expected, implying strong retail momentum at the start of Q4.

- No Fed speakers during yesterday's session. Focus on Wednesday in the US: several regional Fed economic measures, Fed speakers (Waller, Williams, Bostic) and $13B 20Y Bond re-open.

- NZ current account deficit was 3.5% of GDP in the 12 months through September, down from 3.7% in Q2.

- "RBNZ to Phase in New Bank Capital Requirements From Early 2026. The package includes reduced requirements for common equity, more granular risk weights, simplification of capital instruments, and greater alignment of instruments for the "big four" banks with Australian settings." (see BBG link)

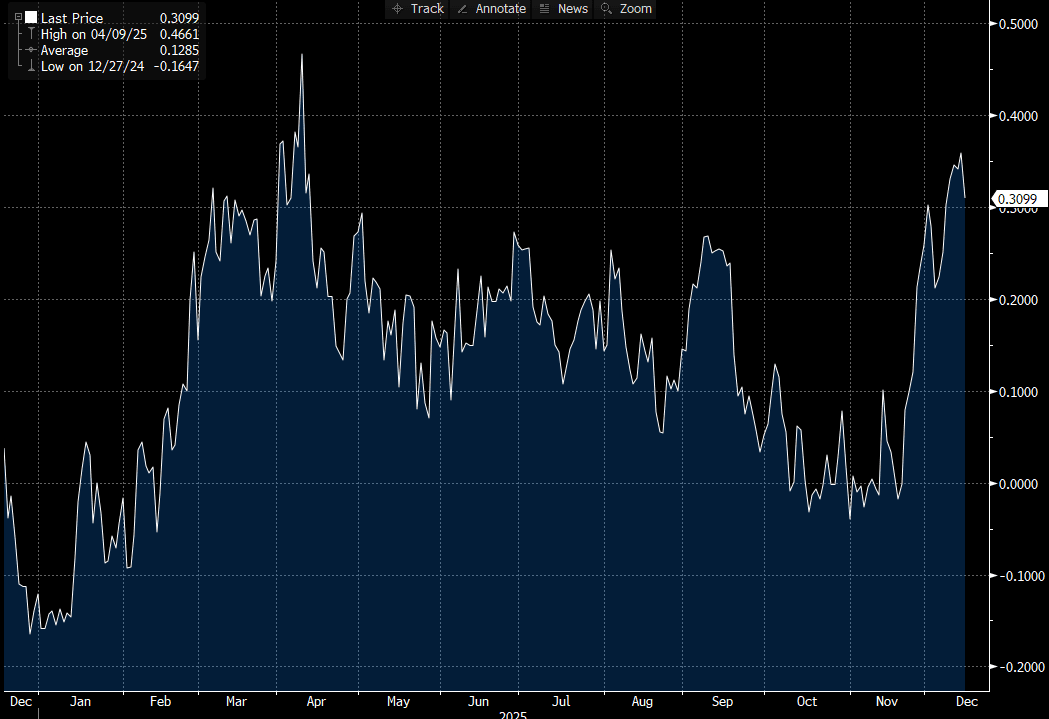

- NZ-US 10-year yield differential is 3bps wider at +31bps (see chart).

- Swap rates are little changed.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, while November 2026 assigns 44ps.

Bloomberg Finance LP

US INFLATION: MNI US CPI Preview: Handle With Care

We've just published our preview of the upcoming CPI report - Download Full Report Here

- The latest delayed CPI update from the Bureau of Labor Statistics (Thursday Dec 18, 0830ET) threatens to be messy in several regards, muddying the signal for markets and for monetary policy.

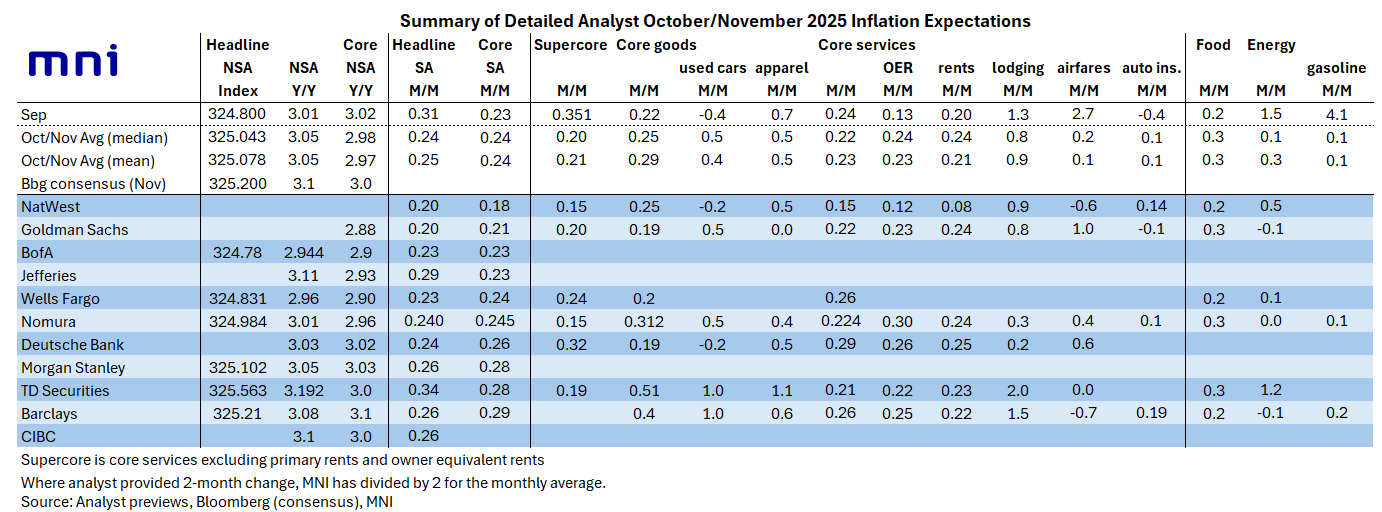

- The government shutdown precluded October data collection, meaning overall CPI aggregates will not be available for the month, and the inflation recorded for November is on a 2-month change basis from Sept.

- While the M/M data will never be officially available, MNI's usual aggregation of sell-side analyst expectations points to expectations of an average of 0.24% M/M core CPI monthly across October and November. This would mark a basically steady pace from September's 0.23% M/M.

- The BLS will provide data for a "small" number of subcomponents for October, potentially including several key components of core CPI that could be derived from internet and private data sources, but it's not clear which ones will be published and how this will be presented in the report.

- Consensus is for core goods to accelerate slightly vs September, partly reflecting expected continued tariff passthrough, with an MNI median of 0.25% M/M average for Oct and Nov (Sep: 0.22%).

- Core services prices are conversely expected to moderate very slightly, at an average 0.22% M/M (Sep: 0.24%), with softer travel-related prices seen offsetting a pickup in rents/OER (leaving Supercore softer).

- On top of this, data quality concerns had been deteriorating even prior to the shutdown, and some are concerned that the collection period for this report could downwardly bias November core goods CPI.

- We already have a sense of how markets may react erratically to a disjointed report: the delayed nonfarm payrolls release for November (which like CPI, also saw partial data for October) out Tuesday saw an initial dovish reaction on an elevated unemployment rate but with many complexities within the report, and some clear caveats, limiting the reaction.

- Fed rate pricing comes into the release showing the next cut only fully priced for the June meeting. We suspect the December CPI report will be more pivotal, with the BLS prioritizing its production and getting back to its original release schedule for Jan 13.

COMMODITIES: Oil Nears US$55 bbl on Supply Fears as Gold Steadies Above US$4,300

- WTI closed down -2.73% at US$55.13 bbl overnight reaching new lows.

- The ongoing concerns about supply continue to plague oil markets with signs that the proposed 2026 supply schedule is placing significant downward pressure on prices.

- Tuesday saw Middle Eastern crude prices reach contango (as per BBG). Contango occurs when spot physical prices are lower than future prices and are representative of rising supply. However longer term contango markets can negatively impact ETFs when existing futures contracts are rolled into new contracts with higher prices that erode returns over time.

- Weak non-farm payrolls overnight didn't help as investors agonize as to the outlook for global growth in 2026

- Additionally, as peace talks continue in Ukraine, markets fear that an agreement to end the war could see supply from Russia reaching markets, further adding to the downward pressure on prices

- Other news overnight all point at supply with Kuwait bring back online a previously halted mega refinery whilst Mexico's refineries are operating at 11-year highs (as per BBG)

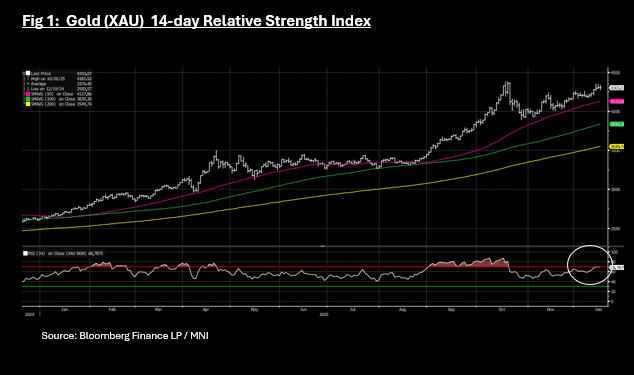

- Brent finished down -1.53% at US$58.85 bbl, the lowest since COVID times when global economic activity was severely interrupted. The move lower for Brent now sees it reaching oversold on the 14-day relative strength index.

- Gold prices did little overnight as bullion consolidated above US$4,300 and finished at US$4,303.33.

- Gold has reached overbought on the 14-day relative strength index, having spent much of September and October overbought.

- Weaker than expected non farm payrolls surprisingly didn't give gold a boost overnight given its correlations to interest rate expectations. Gold investors will look ahead to Thursday's inflation data as the next guide for the future direction of interest rates.