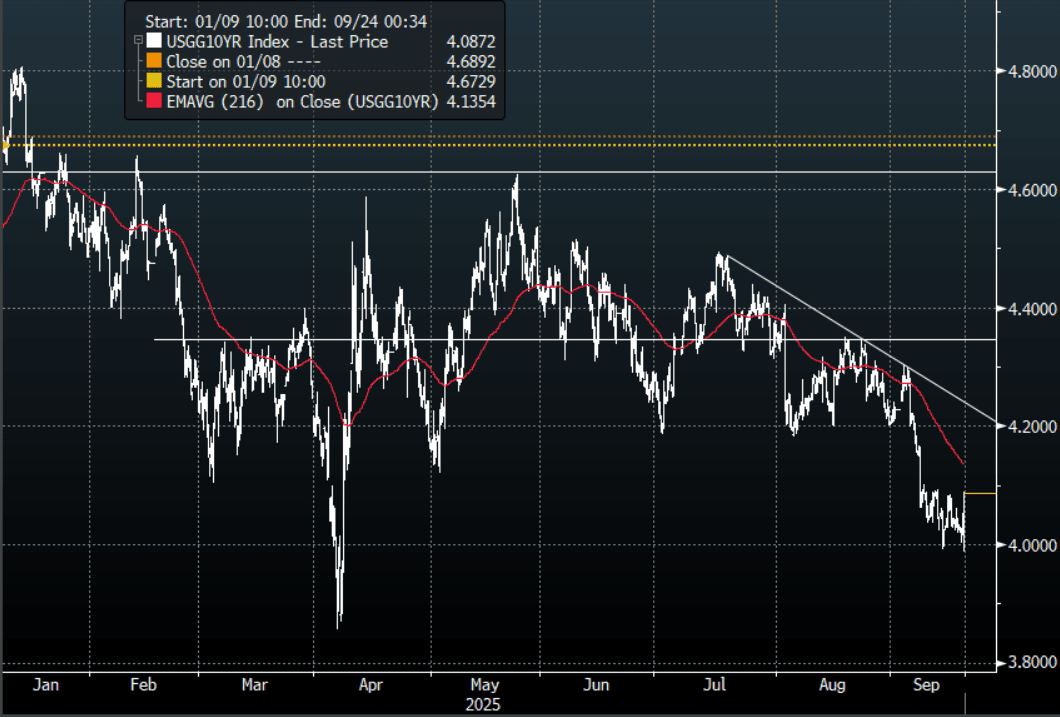

US TSYS: FOMC Dovish, But Not Dovish Enough

TYZ5 reopens at 113-01, down 0-03 from closing levels in today’s Asia-Pac session.

- Treasury yields ended higher after a whippy session overnight;(2s10s +0.94 at 53.193, 5s30s -2.80 at 103.415).

- Overnight the US 10-year yield had a range of 3.9879% - 4.0891%, closing around 4.087%.

- 10-Year Yields could not extend below 4.00% and have bounced as the Fed could not meet the markets very dovish expectations. The first buy-zone is now back towards the 4.15%/4.20% area where I suspect demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area.

- MNI FOMC BRIEF: The Fed resumed its easing cycle with the first cut of the year on September 17, of 25bp to a range of 4.00-4.25%. That decision was expected, but the lack of conviction on the FOMC about the rate path forward was a key theme of the September meeting’s release materials, as well as Chair Powell’s press conference.

- Despite a lower rate path signalled in the new Dot Plot, a seeming lack of clarity on delivering those future rate cuts saw an early dovish market reaction subsequently reverse.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

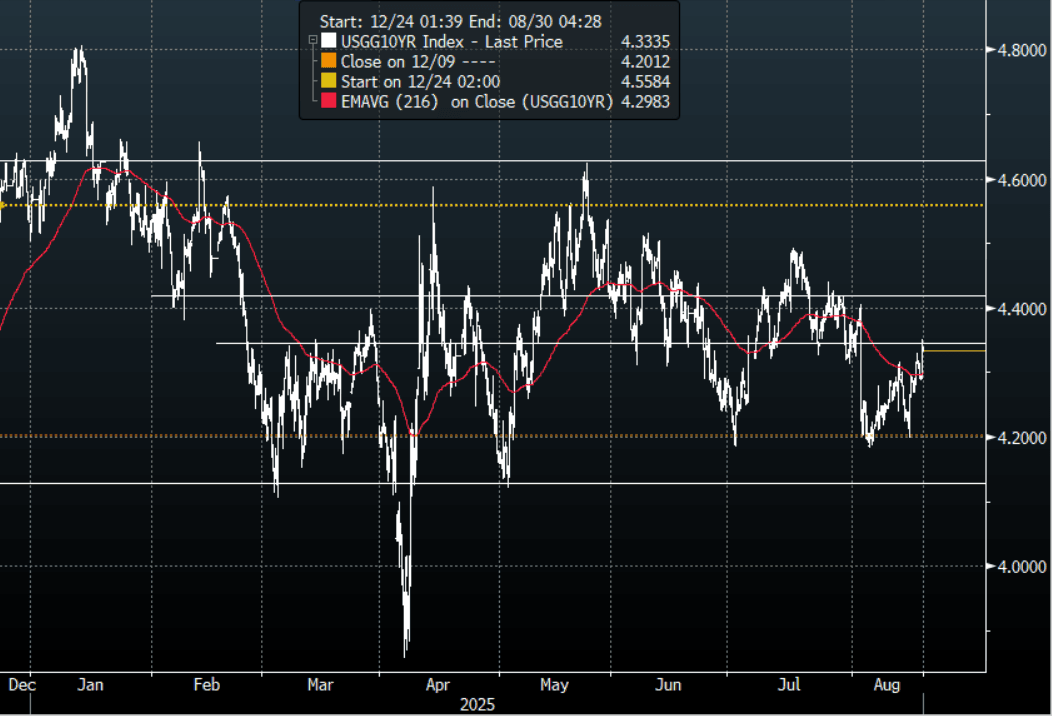

US TSYS: Yields Extend Higher Looking Towards Jackson Hole

TYU5 reopens at 111-18, up 0-01+ from closing levels in today’s Asia-Pac session.

- Overnight the US 10-year yield had a range of 4.22868% - 4.3511%, closing around 4.334%.

- Treasury yields extended higher overnight; led by the long-end which saw the yield curve steepen(2s10s +0.52 at 56.852, 5s30s +0.49 at 108.523).

- (Bloomberg) -- US Treasuries slipped for a third day ahead of a speech by Jerome Powell later this week that traders will monitor for signals on whether the Federal Reserve is poised to cut interest rates. Gennadiy Goldberg, head of US rates strategy at TD Securities, says "The big risk for markets is if he sounds very non-committal" regarding Powell's speech, and notes that markets are trading as if a rate cut is secured.

- MNI US DATA: Homebuilder Sentiment Still Historically Weak, Boding Ill For Activity. August's NAHB/Wells Fargo Housing Market report showed little improvement in the homebuilding sector, with present sales weakening modestly and selling prospects steady/moderately better. The headline index fell 1 point to 32 - reverting back to June's level which is around post-2022 lows, and dashing consensus expectations for a slight improvement to 34. Likewise, present sales reverted 1 point to June levels (35).

- Yields extended higher overnight, probing the pivotal resistance area within the greater 4.10%-4.65% range. The 4.35% area in 10-Year yields should still see demand initially, but the way the market keeps bouncing off levels just below 4.20% will be disconcerting for longs.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

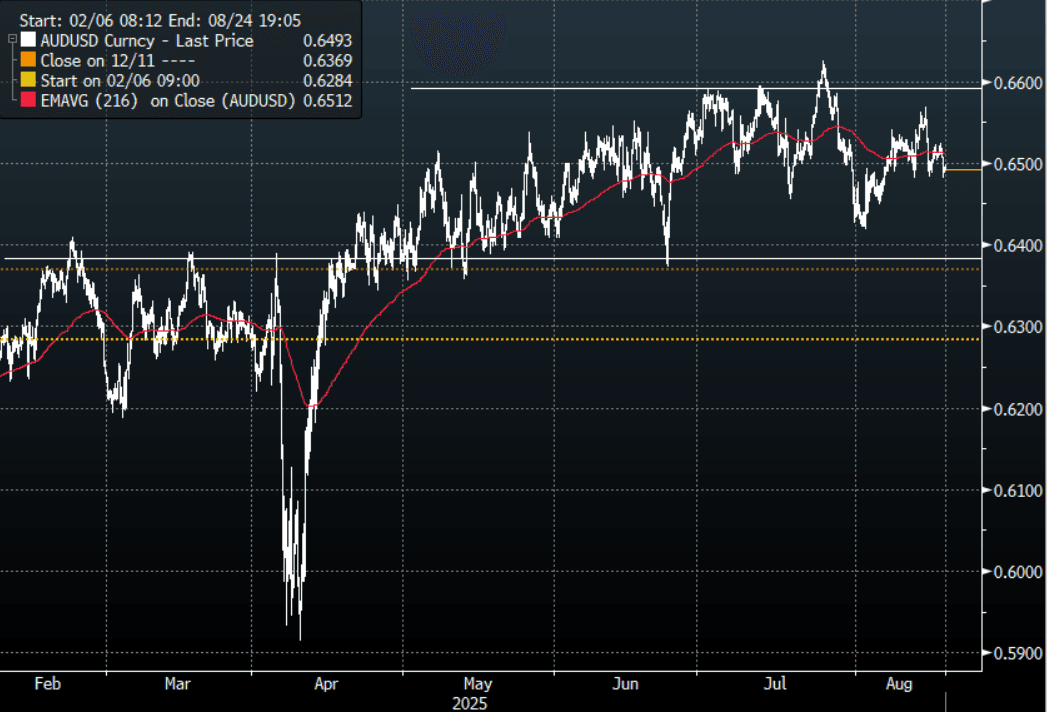

AUD: AUD/USD - Probes Below 0.6500 As USD Shorts Pare Back Into Jackson Hole

The AUD/USD had a range overnight of 0.6482-0.6521, Asia is trading around 0.6495. US rates extended higher looking towards Powell's speech at Jackson Hole later in the week, this has seen the USD see some demand return as the market pares back risk going into it. The AUD continues to consolidate around 0.6500, firmly in the middle of its 0.6350-0.6650 range with no clear direction. Perhaps risks slightly skewed towards more USD short covering as we approach Jackson hole with the risk Powell is not as Dovish as the market.

- (Bloomberg) -- Australia’s property sector is set for a boost as interest-rate cuts drive confidence that the housing cycle has bottomed, according to Lendlease Group’s chief. “There’s a level of appetite that now everyone feels that we’ve bottomed, and if anything, we’ve started to see a bit of an uptick in the real estate cycle.”

- “China’s exports of rare earth products reached their highest since January, with overseas volumes rising 69% to 6,422 tons in July. The nation is ramping up shipments months after it curbed supplies as leverage in the US trade clash.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6515(AUD744m), 0.6390(AUD380m). Upcoming Close Strikes : 0.6500(AUD454m Aug 21), 0.6600(AUD1.34b Aug 21) - BBG

- CFTC Data shows Asset managers added to their shorts -67449(Last -60729), the Leveraged community though reduced their own shorts -10121(Last -13997).

- Data/Event: Westpac Consumer Confidence

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

CNH: USD/CNH Tracking Familiar Ranges, Local Equities Aided By Switch From Bonds

Spot USD/CNH tracks near 7.1870 in early Tuesday dealings, after posting little net change for Monday's session. Broader USD sentiment was firmer, with the DXY up 0.30%, while the BBDXY gained 0.20%. The USD was initially assisted by softer sentiment for major equity benchmarks, and US yields turning higher across the US Monday session then provided further support. Spot USD/CNY ended Monday trade at 7.1849, while the CNY CFETS basket tracker edged down by 0.10% to 96.07. The index remains within recent ranges.

- For spot USD/CNH, little has changed from a technical standpoint. Current levels are very close to the 20 and 50-day EMA levels. The 200-day EMA resistance point is around 7.2175, while renewed downside in the pair is likely to see 7.1681, the August low, eyed.

- China equities have outperformed global equity trends in recent sessions, but the China to global equity ratio is still just under late July highs. BBG noted firm inflows China ETFs. "China recorded the biggest inflow across emerging-markets in the week — $623.8 million — led by iShares MSCI China. That ETF alone, known by the ticker MCHI, accounted for $215 million of the investment." The CSI 300 closed just short of Oct 2024 highs yesterday.

- The rotation out of bonds and into equities is helping. Bond yields were firmer across the board yesterday, with the 10yr up above 1.78%, fresh highs back to early April. Still, US-CH government bond yield differentials sit within recent ranges, the 10yr spread around +255bps.

- We still await July FDI figures, while loan prime rate outcomes are due tomorrow. No change is expected.