UKRAINE: Flurry Of Calls Expected Amid Talks Around US-Russia 28-Point Plan

A flurry of calls between President Volodymyr Zelenskyy and international leaders is expected to take place today amid the ongoing talks and speculation regarding the US-Russian 28-point peace plan that was presented to the Ukrainian president on 20 November. First, Zelenskyy will talk with German Chancellor Friedrich Merz, French President Emmanuel Macron, and British Prime Minister Sir Keir Starmer. Bild reports that Zelenskyy and Merz will then have a call later today with US President Donald Trump.

- European leaders have warned that they, and more importantly Kyiv, should not be excluded from the peace process, as appears to have been the case with the drafting of the 28-point plan.

- The major concessions that would be forced on Ukraine, combined with some of Russia's most maximalist demands being accepted by the US, has led to criticism of the deal both in Europe and by Russia hawks in the US. However, it appears the Trump administration is paying little heed to this, with its main focus being a rapid end to the war by any means necessary.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

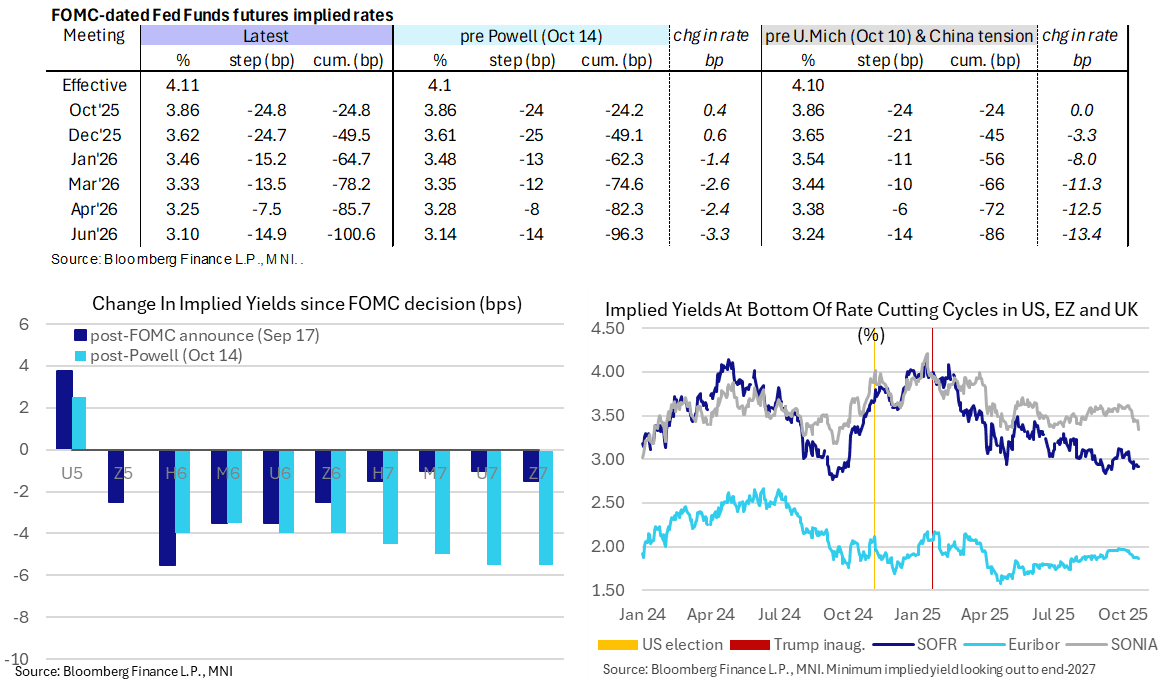

STIR: Back-to-Back Fed 25bp Cuts Still Eyed, Only Mild Impact From Soft UK CPI

- Fed Funds implied rates are little changed overnight, with back-to-back cuts seen for next week and December meetings before a quarterly pace thereafter to mid-2026.

- Cumulative cuts from 4.11% effective: 25bp Oct, 49.5bp Dec, 64.5bp Jan, 78bp Mar, 85.5bp Apr and 100.5bp Jun.

- SOFR futures are little changed on the day, with only small intraday spillover from a sizeable rally in UK rates on softer than expected UK CPI inflation.

- The SOFR implied terminal yield of 2.915% (SFRH7) is unchanged on the day, close to last week’s lowest close of 2.89% in risk-off moves on regional bank fears. For context, cycle lows were 2.77% back in Sep 2024 in anticipation of an aggressive start to the Fed’s easing cycle at the time.

- It’s a particularly thin data docket today, with just MBA mortgage applications. More notable releases for the week are state-level jobless claims to be released from Thursday afternoon and then the highlight being the delayed September CPI report on Friday.

LOOK AHEAD: Wednesday Data Calendar: 20Y Bond Re-Open

- US Data/Speaker Calendar (prior, estimate)

- 10/22 0700 MBA Mortgage Applications (-1.8%, --)

- 10/22 1130 US Tsy $69B 17W bill auction

- 10/22 1300 US Tsy $13B 20Y Bond re-open (91210UN6)

- 10/22 1600 Pres Trump meets w/ Secretary General of NATO (closed Press)

- Source: Bloomberg Finance L.P. / MNI

US 10YR FUTURE TECHS: (Z5) Bull Cycle Intact

- RES 4: 115-00+ High Oct 1 ‘24 (cont)

- RES 3: 114-21+ 1.00 proi of the Aug 18 - Sep 11 - 25 price swing

- RES 2: 114-10 High Apr 7 (cont) and a key resistance

- RES 1: 114-02 High Oct 17

- PRICE: 113-24 @ 11:15 BST Oct 22

- SUP 1: 113-03+ 20-day EMA

- SUP 2: 112-30 Low Oct 13

- SUP 3: 112-22 50-day EMA

- SUP 4: 112-06 Low Sep 25 and a reversal trigger

Bullish conditions in Treasuries remain intact. The recent breach of key resistance at 113-29, the Sep 11 high, confirms a resumption of the medium-term uptrend. Moving average studies are in a bull-mode position and this set-up highlights a dominant uptrend. Sights are on 114-10, the Apr 7 high (cont) and the next key resistance. Firm support lies at 11303+, the 20-day EMA.