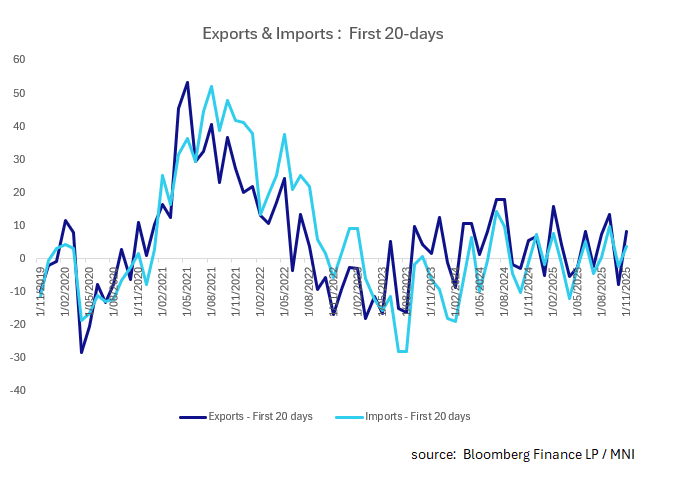

KOREA: First 20-day Trade Data Jump Supports Rates Hold

- Korea's first 20-days exports and imports were strong, rebounding from last month's decline. The main driver for the decline last month was the adjustment for working days differences.

- Exports rose +8.2% above the 5-Year average of +5.4%. Chip exports rose +26.5% YoY and exports to China were up +10.2% and US +5.7%

- Korea's first 20-days imports rose +3.7%, following a decline of -2.3% yet remains below the 5-Yr average of +5.5%

- Trade data has been impacted over the last two months by frontloading of shipments, particularly chips / electronics, ahead of the Trump Xi meeting yet the underlying trend is strong suggesting the worst of the trade war may be over and potential upside for the Korean economy.

- This comes at a time when rate expectations have moved away from cuts, with markets now suggesting an extended hold.

- The challenge remains with the Won which has lost ground by -2.7% in the last month, and is feeding into the higher PPI released this morning.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: ACGB Jun-35 Auction Result

The AOFM sells A$900mn of the 2.75% 21 June 2035 Bond, issue #TB145:

- Average Yield (%): 4.1047 (prev. 4.2953)

- High Yield (%): 4.1050 (prev. 4.2975)

- Bid/Cover: 2.9056x (prev. 3.300x)

- Allotted at Highest Accepted Yld as % of Bid at that Yld (%): 96.3 (prev. 36.1)

- Bidders: 31 (prev. 38), successful 10 (prev. 17), allocated in full 2 (prev. 10)

CNH: Outperforms USD Index Gains, CNH/JPY Uptrend Intact

USD/CNH was supported sub 7.1200 again yesterday and we track near 7.1270 in early Wednesday dealings. Little has changed from a technical standpoint for USD/CNH, with downside risks still in play if we can sustain a break into the 7.11/7.12 region. On the upside, the 50-day EMA is just above 7.1400, where selling interest should emerge given the CNY fixing bias.

- In aggregate we were little changed for Tuesday's session, outperforming broader USD index gains (which were supported by the weaker yen, post Takaichi's confirmation as PM, whilst slumping gold prices were also a factor). CNH/JPY got as highs as 21.3645, but sits back at 21.32 now. Upside focus rests on a renewed test of the 21.5000 region.

- Spot USD/CNY finished up at 7.1247, while the CNY CFETS basket tracker was little changed near 97.20 (but will be biased higher if the yuan continues to outperform on key crosses like CNH/JPY).

- Focus remains on US-China trade deal negotiations. Trump stated, via BBG: "“I have a great relationship with President Xi. I expect to be able to make a good deal with him,” Trump said Tuesday during a lunch with Republican lawmakers in the White House Rose Garden. “I want him to make a good deal for China — but it’s got to be fair.” However, he also raised the possibility a meeting may not happen. A short while ago Trump stated that as of Nov 1 a potential tariff rate of 155% would not be sustainable for China. Market odds of a 100% tariff rate hike (by Nov 1) sit back at 18.5 per Polymarket, so up from recent lows.

- Later we get FX settlements data for Sep.

OIL: Crude Off Support Levels Helped By SPR Purchases & US Stock Decline

Oil prices spiked and found some support from news that the US will buy 1mn barrels for the SPR but remained below initial resistance levels. The barrels for delivery in December and January are to be the start of refilling as the government takes advantage of lower prices but with the SPR still down 182 mn barrels since end-January 2022 it is only a small addition.

- WTI rose 1% to $57.58/bbl after reaching a low of $56.35, at initial support, followed by a high of $58.08 after the SPR news. It is currently around $57.54. Initial resistance is at $61.76, 50-day EMA.

- Brent spiked to $62.10/bll before finishing 1.1% higher at $61.66. It fell to $60.35 earlier, holding above psychological round number support at $60.00. The benchmark remains in a bearish trend. Initial resistance is at $65.35, 50-day EMA.

- The US SPR was run down through Biden’s term, especially following Russia’s invasion of Ukraine, reaching a low in July 2023 and was only 17% or 60mn barrels higher last week.

- After rising the previous week, Bloomberg reported US oil inventories fell 3mn barrels last week, according to people familiar with the API data. Product stocks were also lower with gasoline down 0.2k and distillate 1mn. The official EIA data is out Wednesday. With the IEA forecasting a record surplus in 2026, inventory data are being monitored closely.

- After news that the meeting between the US’ Rubio and Russia’s Lavrov was being postponed, talks between Presidents Trump and Putin will now not take place in the “immediate future” as Russia won’t accept holding the frontline in Ukraine where it currently is. A truce and easing of sanctions on Russian fuel remain elusive.