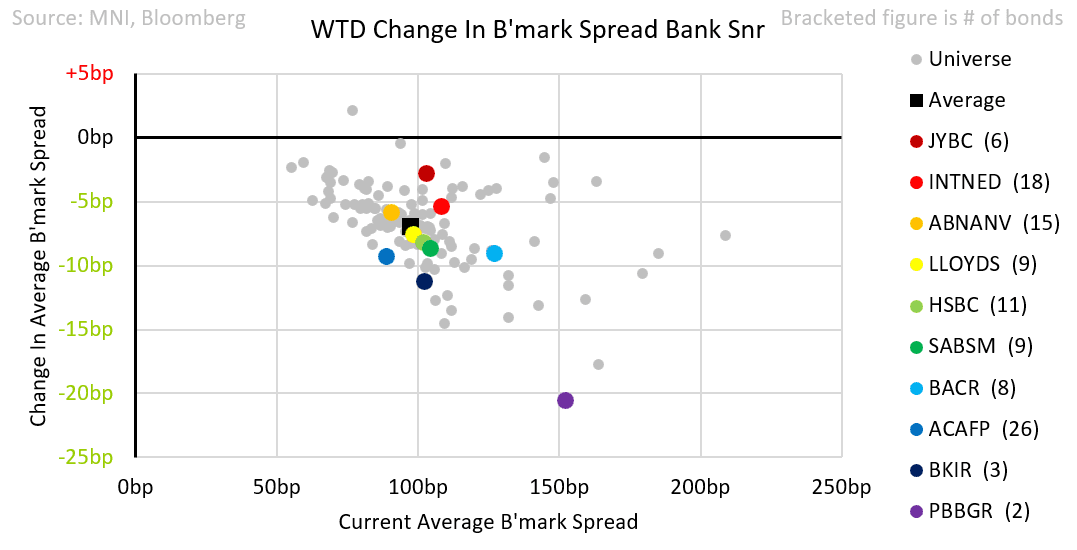

EU FINANCIALS: Financials - Week in Review

Financials performed strongly in a relatively heavy week for issuance. Sr banks and insurers were -7 & -6bps tighter respectively. In Tier 2 space both were -10bps.

Results

Our banks earnings tracker showed that this quarter Standard Chartered and SOCGEN bonds spread tightened following positive results. Unicaja bonds lagged, despite beating expectations. https://mni.marketnews.com/3FbGT3E

- We preview Banco Commercial Portugeus results. We highlight upgrade risk and relatively wide trading tier 2s. https://mni.marketnews.com/3H6MYyQ

- UniCredit earnings were good. Management sounded patient regarding potential M&A. https://mni.marketnews.com/3F9B8Dw

- ABN Amro results were in line.

- KBC earnings were in line. Top line growth remains healthy.

- Deutsche Pfandbriefbank earnings were slightly positive, normalisation of provisions continue, although this was helped by an FX tailwind from the weaker Dollar. Management noted US new business would halt and an exit would be considered. Bonds reacted by rallying. https://mni.marketnews.com/4mjpTcx

SMFC disappointed due to weak performance from international and global markets units.

- Aviva earnings beat expectations slightly. Direct line acquisition remains on track.

- Allianz had their best ever quarter of revenue, an 11.5% increase on a pretty good Q1 24. https://mni.marketnews.com/3ZjWFjG

- Reinsurance profits that were affected by LA wildfires

- Hannover Re missed slightly, by results were still solid

- Munich Re beat expectations, but net income was down meaningfully from Q1 24.

- Swiss Re new income held up well, despite wildfire losses

- III revenue fell short of expectations. Management note that deal activity was subdued due to US trade policy affected market environment.

- Grenke results confirmed what we know from pre-release, higher provision driven net income weakness

Ratings

- Banco Montepio was upgraded by Moody's and their Sr prefs become IG. Bonds are BB+ stable at Fitch so IG index inclusion is still some way off. https://mni.marketnews.com/3SEcGNL

New Issues

We saw value in several new issued most new issues this week, especially in the AT1's and GBP bonds issued later in the week.

AT1

- Sabadell issued a € AT1 at 6.5%, we saw FV at 6.25%. The bond has gained 1.3pts since issue, currently yielding 6.38%. https://mni.marketnews.com/44HBVpU

- Barclays issued a £ AT1 at 8.375% vs our FV of 8.125%. Currently trading at 101.2 or 8.21%. https://mni.marketnews.com/43ooB7z

- Erste Bank issued a € AT1 a 6.375%, at where we saw FV.

Tier 2

- ING Issued a tier 2 bond at MS+180, we saw FV at MS+173. It is currently trading at Z+174.

- Credito Emiliano issued a tier 2, pricing at MS+215, where they remain. Coverage of 7.5x the 200m WNG size allowed them to come through our MS+220 FV.

- Credit Agricole issued a £ tier 2 bond, pricing at UKT+190 vs our FV at UKT+175. Trading UKT+183. https://mni.marketnews.com/4dmcuwi

- Matmut issued a debut tier 2 at MS+215, through our FV of MS+220 - we saw medium term value in the name should M&A execution risks be overcome https://mni.marketnews.com/4k37IpW

Sr non-preferred / Sr bail-in

- HSBC issued a £ sr bail-in bond, we have FV at UKT+125, but it came at UKT+145. Trading UKT+138.5. https://mni.marketnews.com/3GZV0tC

- BKIR issued a € sr bail-in bond, we had FV at MS+122, it priced at MS+127, trading Z+121. https://mni.marketnews.com/4dlITTG

- DNB issued a € sr non-preferred debt at MS+90 where it is currently trading, we had FV at MS+95.

- Jyske Bank issued a € sr-non preferred, we had FV at MS+119, it priced at MS+127 where it remains.

- SBAB issued a € sr non-preferred bond at MS+110, a shade inside our FV of MS+112.

- Lloyds issued £ sr-bail in bonds at UKT+125 vs our FV range of UKT+120-125.

Sr Preferred

- Achmea issued a € sr pref at MS+62, we had FV at MS+55. It is trading Z+54.

Sr Unsecured

- Amex issued € senior unsecured bonds at MS+105, at FV.

- IG Group issued debt at UKT+210 vs our UKT+190 FV. Trading at UKT+206.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Moderate GOP Reps Won't Back Reconcilliation Bill Including Medicaid Cuts

A dozen moderate House Republicans have issued a letter to GOP leadership warning they won’t back a reconciliation package that includes major cuts to Medicaid. The letter is the opening salvo in what is expected to be a bitter dispute between Republican moderates and deficit hawks over how deeply to cut government spending to fund President Donald Trump’s tax agenda.

- Punchbowl notes: “Remember, House Republicans’ reconciliation plan includes cutting $880 billion under the House Energy and Commerce Committee’s purview, much of which will likely have to come from Medicaid.”

- The letter reads: “We support targeted reforms to improve program integrity, reduce improper payments, and modernize delivery systems to fix flaws in the program that divert resources away from children, seniors, individuals with disabilities, and pregnant women — those who the program was intended to help. However, we cannot and will not support a final reconciliation bill that includes any reduction in Medicaid coverage for vulnerable populations.”

- Notus reports that the same fissures are evident in the upper chamber: "Senators have already been clear that they won’t tolerate those kinds of [Medicare] cuts. Even Sen. Josh Hawley wanted assurances from Trump that Medicaid wouldn’t be touched in the final product — a promise that other senators also wanted and contradicts concessions that Freedom Caucus members extracted from House leaders."

CHINA: Sell-Side Analyst Views After Q1 GDP

- Commerzbank expects the Chinese economy to come under significant pressure in the coming quarters. They have lowered their growth forecast for 2025 from 4.3% to 3.8% and for 2026 from 4.0% to 3.6%. To counter the tariff impact, they expect Beijing to frontload its stimulus measures, with more concrete policy steps probably announced after the Politburo meeting later this month.

- Goldman Sachs expects sequential GDP growth to drop significantly in Q2 and remain low in H2 on the back of severe external shocks from increased US tariffs despite the ongoing easing measures. They believe that the urgency for more policy stimulus is on the rise, with fiscal expansion to do most of the heavy lifting towards stabilising growth.

- HSBC says that the strong Q1 sets a good foundation for the year, but it's clear that more will need to be done to help offset the increased external headwinds. They see accelerated fiscal policy rollout, ongoing monetary easing as well as more policies to boost consumption to help support growth.

- JP Morgan have reduced their China GDP growth forecast further, reflecting the additional tariff shock and Q1 GDP data. They lower their Q3 GDP growth forecast to 0.4% q/q saar (from 1.8%q/q saar) and the Q4 GDP growth forecast to 2.0% q/q saar (from 3.0%). Their 2025 full-year growth forecast now stands at 4.1%, down from 4.4% previously.

- Nomura cut their annual GDP growth forecast from 4.5% to 4.0%, given the strong headwinds to growth. They expect quarterly y/y GDP growth to drop to 3.7%, 3.6% and 3.6% in Q2, Q3 and Q4, respectively. They take into account a larger and faster stimulus package from Beijing but believe that the gap might be too large for Beijing to meet its “around 5.0%” growth target.

- SocGen lower their 2025 and 2026 GDP growth forecasts to 4%, assuming additional stimulus of 2.5% of GDP, and now expect more sustained deflationary pressures this year and next. The short-term impact on the labour market is likely to be extremely hard to deal with. They believe a near-term RRR cut is possible to ease liquidity constraints and expect consumption and housing to be prioritised at the late April Politburo meeting.

US DATA: Strong First Quarter For US Industry, But Slowdown Looming

March industrial production was largely as expected, with headline IP growing contracting by 0.3% M/M (-0.2% survey) but prior upwardly revised by 0.1pp (+0.8%). Manufacturing production rose by 0.3% (0.2% survey 1.0% prior upwardly revised from 0.9%). Capacity utilization fell slightly (77.8% vs 78.2% prior).

- Dragging on IP was the utilities sector's 5.8% drop in output, "as temperatures were warmer than is typical for the month" (per the Fed report), a second consecutive month of contraction (-1.5% prior) - but this volatile category still posted 4.4% growth on a Y/Y basis (compared with 1.3% for IP as a whole). Mining also slowed in March, to 0.6% after 1.7% prior.

- Within the major final products categories, consumer goods saw a strong pullback (-1.0% M/M after 0.5% prior), and has barely grown in the past year (0.3% Y/Y), though business equipment fared better (1.7% M/M after 1.8%).

- Despite the March contraction, IP posted annualized growth of 5.5% in the first quarter of the year, the best 3M reading since May 2022. Overall manufacturing rose 5.1% for the quarter (annualized), led by durables (7.9%). There were some idiosyncrasies here, with motor vehicles and parts production jumping by 9.2% in February (likely tariff front-running) with the aerospace index rising 65% after contractions in previous quarters, potentially reflecting the end of a work stoppage at Boeing in Q4.

- Looking ahead to Q2, core durable goods orders have slowed since late last year while ISM Manufacturing has returned to contractionary territory (joining multiple other indicators in pointing to a tariff-related retrenchment), suggesting that the best may be behind the sector which could a pullback in activity in Q2.