EU FINANCIALS: FINANCIALS: Generali (ASSGEN A3/NR/A Pos) - Q3 Results

Nov-15 07:44

Mixed operating result. Gross written premiums +18.1% represent strong demand, and pricing appears firm. P&C claims again above of expectations.

- Life was strong, €1,080m up €96m on Q2.

- P&C Q3 result was €481m. Q3 is often their weakest, was better than Q3 23, but worse than Q3 22.

- Both Asset Management and Banca Generali posted slightly weaker results QoQ, with the operating result 10% lower to €271m. Lower NIM likely the result of Baca Generali's revenue change but Opex has increased rapidly in these divisions over the last few quarters.

- Solvency II has fallen -11% to 209%. Divi, buy backs, bolt on M&A all weigh on solvency, although the level is still healthy enough for now. Underlying capital generation should be enough to stop the decline going forward.

Valuation - Generali bonds trade a little tight, although the rating is a little constrained by the sovereign.

Call at 11am UK time - https://services.choruscall.it/DiamondPassRegistration/register?confirmationNumber=1613081&linkSecurityString=327718a1e

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Threat To Outright & Cross-Market Technicals Heightened Post-CPI

Oct-16 07:37

Gilt futures pierce resistance at the 20-day EMA (97.68), before a fade back below.

- Fresh demand would target key near-term resistance at the September 2 low (98.11). A break there would pose greater threat to the bearish technical theme.

- 10-Year gilt yields extend yesterday’s move back below broken downtrend resistance drawn off the October ’23 peak, breaking a run of three consecutive closes above.

- Old resistance at the September 2 high (4.061%) presents initial support.

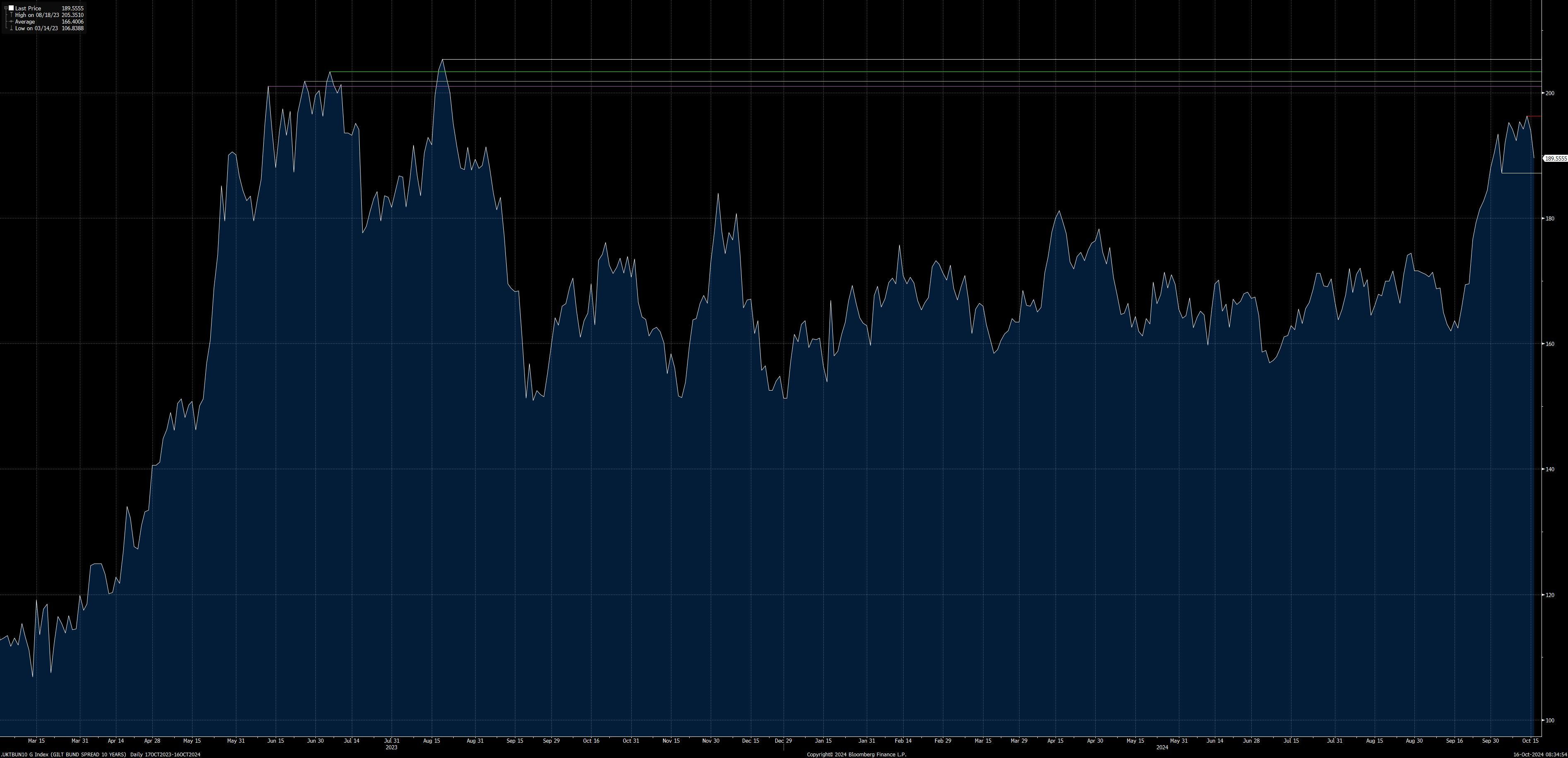

- The 10-Year Gilt/Bund spread is back below 190bp. The spread failed to test 200bp during the recent round of widening, despite registering fresh cycle wides.

- First support seen at the Oct 3 closing low (187.21bp).

- An extension of the dovish repricing covering BoE ’25 meetings could provide further tailwinds to today’s early moves, although we think that markets are likely to overreact (on the dovish side) to the data, at least in the short-term (thought process outlined in earlier bullets).

- Multi-week, the outcome of the Budget will be key for gilts, with the risk of increased issuance clearly contributing to the recent cross-market widening.

Fig. 1: 10-Year Gilt Yields (%)

Source: MNI - Market News/Bloomberg

Fig. 2: UK/Germany 10-Year Yield Spread (bp)

Source: MNI - Market News/Bloomberg

EQUITIES: BNP Option Vol trade

Oct-16 07:37

BNP Vol trade:

- BNP (19/12/25) 60^ sold at 13.73 in 1.8k.

EQUITIES: Santander Call Option

Oct-16 07:33

Single stock Bank Option, Santander:

- BDS2 (15th Nov) 4.7c, bought for 0.10 in 8k.