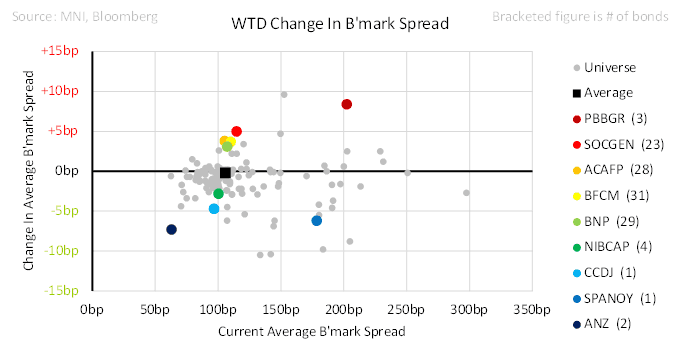

EU FINANCIALS: FINANCIALS: Financials - Week in review

On the surface a quiet week, with bank and insurance snr paper average spreads only moving -0.2bps and -0.4bps respectively. Underneath French banks were particularly weak as the threat of government collapse looms. https://mni.marketnews.com/3Z8CjsRas In addition, the spectre of downgrades hangs over several of the French banks, with Moody's and Fitch already on negative outlook. https://mni.marketnews.com/4fNSUcG S&P are due to comment this evening, viewing a negative outlook move as the most likely outcome (29/11).

M&A remains a key theme for European financials. Several large European banks and insurance companies have excess capital on balance sheets. Acquirers can both capture this excess capital at targets and shape their own balance sheets to be leaner very rapidly - much more so than years of steady share buybacks.

UniCredit continues to make headlines. Having apparently decided the its potential Commerzbank merger is on hold, pending the German election early in 2025, it made an all share offer from Banco BPM (BAMIIM). https://mni.marketnews.com/49fcYlJ This offer, assumed to be only an opening salvo, built in very little premium for BAMIIM and was rejected by management, but did cause meaningful tightening in BAMIIM bonds. https://mni.marketnews.com/41cyt4D There were also rumours that Credit Agricole, already a 9% owner in BAMIIM was increasing its stake through derivatives.

Aviva made a bid for Direct line, valuing the insurer at £3.3bn, or 250p/share, which was rejected out of hand by Direct Line management. The bid was only slightly higher than a 236p bid management rejected in March. Both the bonds and equity are nonetheless pricing a high likelihood of a deal. https://mni.marketnews.com/498FdCJ

Meanwhile in Spain, positive ratings momentum continues with Cajamar getting a ratings upgrade at S&P.Its senior preferred rating climbs to BBB- and promotes it to investment grade. NPA's in the bank have fallen from 12% at the peak in 2019 to 4% now and further improvements looks possible. https://mni.marketnews.com/3B16la4

Bank of Ireland and Allied Irish Bank were both placed on positive outlook by S&P, reflecting collectively improved digital footprints, cost of risk and capital ratios.

Nationwide reported H1 results showing reduced profits, and falling rates put pressure on NIM. Volume growth was solid however and capital ratios remain extremely strong

Issuance was light this week, with DNB Bank issuing a 6NC5 SNP at MS+90 and Abanca issuing a 12NC7 Tier 2 at MS+245. Both deals have performed well.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CROSS ASSET: Bund and EUR falls

- Bund is seeing a push back towards the intraday low, following a decent beat in the US ADP, that was also revised higher.

- Despite the move, initial support seen at the September high in Yield remains untested, equates to 132.37 today.

- The EURUSD is back at session low on the broader USD bid.

US TSYS: Post-ADP React

Treasury futures reverse gains after much higher than expected ADP jobs gain. The Dec'24 10Y contract trades down to 110-26.5 (+2.5) from 111-01.5 prior to release. Technical support well below at 110-09+ (Low Oct 29). 10Y yield climbs to 4.2582% high, curves flatter: 2s10s -2.467 at 12.908. Next up: GDP and Personal consumption data not to mention the UK budget release at 0830ET.

BTP: 10-year Spread To Bunds 4.5bps Wider At 127bps

European equity weakness and hawkish ECB repricing sees the 10-year BTP/Bund spread 4.5bps wider today at 127bps.

- ECB-dated OIS continue to price 31bps of easing through the December meeting, down from 35bps before this morning’s stronger-than-expected German GDP and state-level inflation data.

- Meanwhile, Italian flash Q3 GDP was weaker-than-expected at 0.0% Q/Q (vs 0.2% cons).

- A further increase in EUR 3m10y swaption vol (now at its highest since mid-August) will have also added widening pressure.

- BTP futures are -34 ticks at 120.19, with key support at 119.97, the Oct 11 low. Clearance of this level would undermine the recent uptrend and signal scope for a deeper retracement.