FED FUNDS FUTURES: FFF6 Lifted

Nov-20 08:02

FFF6 paper paid 96.210 on ~20.3K, 96.215 trade on the follow.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BTP: Short 2yr BTP Block Trade

Oct-21 07:52

Short 2yr BTP Block trade, suggest buyer:

- BTSZ5 ~1.61k at 108.28.

EQUITY OPTIONS: BNP Straddle Trade

Oct-21 07:50

BNP Vol Option Trade:

- BNP (18/12/26) 72^, bought for 16.52 in 1.8k.

ECB: Some Net Dovish Passages In Lane Speech, But Data Dependent Approach Holds

Oct-21 07:45

Lane's speech outlines several channels through which the ECB gauges the transmission of monetary policy. While he concludes that transmission is progressing "smoothly", there are a few net dovish passages to be aware of. Overall though, he stresses that the time-varying strength of monetary transmission and the configuration of domestic/external shocks hitting the economy argues for the familiar data-dependent and meeting-by-meeting approach.

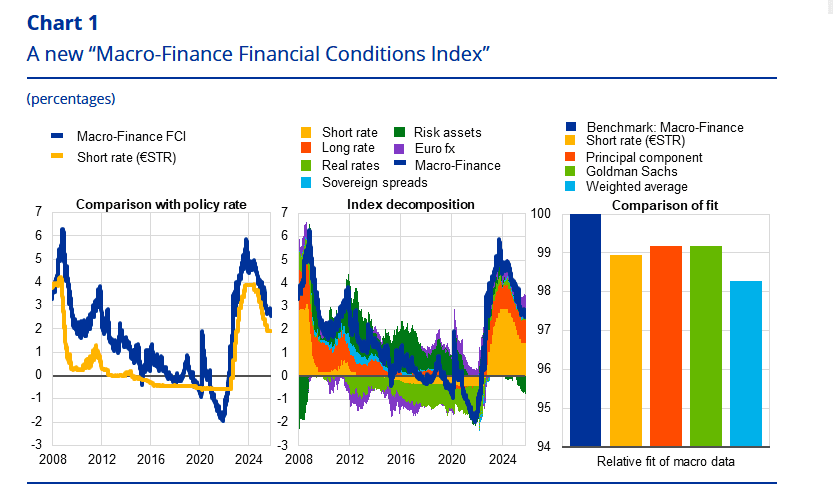

- Lane introduces a new Financial Conditions Index (the “Macro-Finance FCI”) which aims to account for “mutual feedback between macroeconomic and financial dynamics”

- “Since the peak of the tightening cycle, the index has indicated that financial conditions have become noticeably less restrictive"....“Despite this easing, the level of the Macro-Finance FCI remains well above its historical sample average"

- On credit dynamics:

- “The strength of credit dynamics relative to the broader economy can be gauged through a credit-to-GDP gap analysis, which captures the deviation of the credit-to-GDP ratio from historical benchmarks”…” Regardless of the method, the gap remains in negative territory".

- “On net, the ongoing transmission of monetary policy easing to credit volumes has been more gradual than anticipated building on past regularities.”

- On heterogeneity of transmission:

- “The change in borrower composition and the muted risk appetite of banks point towards the risk-taking and balance sheet channels of monetary policy operating less strongly for lower-income households and smaller firms during the easing cycle”.....“Since these groups typically have higher marginal propensities to consume and invest, this heterogeneity in transmission may reduce the effectiveness of recent interest rate cuts in stimulating aggregate demand in the current context of high global uncertainty”

- On the impact of uncertainty:

- Uncertainty "directly lowers credit demand and credit supply. “…”ECB staff also finds that elevated uncertainty diminishes the impact of monetary policy easing on firms’ investment”

- “On its own terms, if uncertainty weakens monetary transmission, this implies that a more powerful monetary intervention is required to deliver a given policy objective. At the same time, monetary policymakers must strike a balance between the incentives to act more powerfully and the incentives to wait and see whether an uncertainty spike self-corrects in a timely manner”

- Finally, Lane notes that “The strength of monetary policy transmission depends on the configuration of the macroeconomic shocks hitting the euro area. Two (interconnected) external shocks are currently shaping euro area macroeconomic dynamics. First, a large portion of the uncertainty highlighted above stems from outside the EU, reflecting unpredictable shifts in foreign economic policies and concerns about the future course of geopolitical tensions. Second, there has been a substantial appreciation of the euro”.