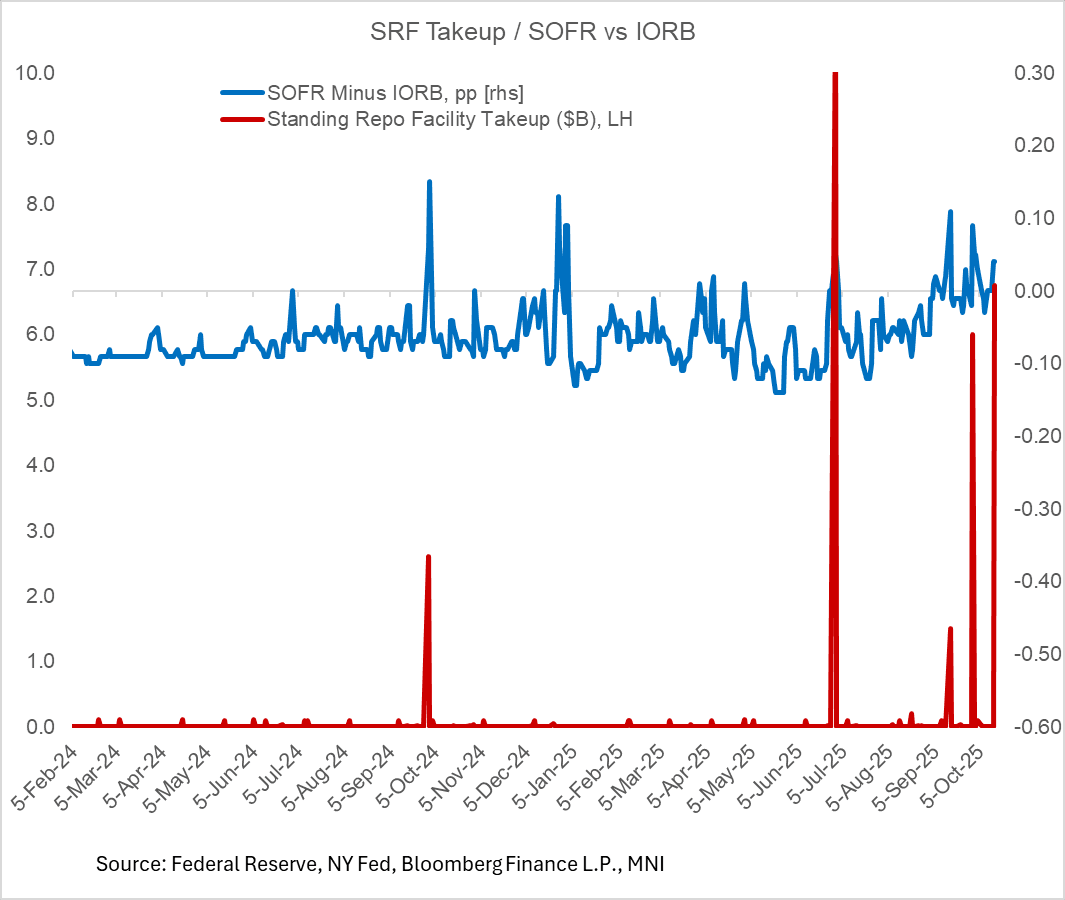

US TSYS/OVERNIGHT REPO: Fed Standing Repo Takeup Jump Part Of Wider Pressure

The Fed's Standing Repo Facility (SRF) saw its highest takeup this morning since the quarter-/month-end date of June 30.

- The $6.8B usage of the facility comes as SOFR printed 4bp above IORB (4.19% vs 4.15%) yesterday, with a variety of other indicators suggesting mounting funding market pressures. It compares with the $6.0B takeup at the last month-/quarter end date of September, and is the 2rd-highest takeup (after June 30) since Q2 2020. (The SRF was made permanent in 2021).

- Even so this rise should be put into perspective; takeup was many times larger in 2019 during a previous episode of funding pressures that led to the Fed restarting asset purchases. And per the September meeting minutes, "a few participants noted that the SRF would help keep the federal funds rate within its target range and ensure that temporary pressures in money markets would not disrupt the ongoing reduction in Federal Reserve securities holdings to the level needed to implement monetary policy efficiently and effectively in the Committee’s ample-reserves regime"

- Even so, there's a variety of factors contributing to the rise in takeup. Based on various measures we (and the Fed) look at, some funding market pressure has been building up for a few weeks now as reserves fell below $3T - the pressures are still on the light side but enough to get the Fed thinking about slowing runoff (as evidenced by Chair Powell's speech Tuesday in which he suggested QT could end in the coming months).

- Today's pressures may be related to a tax date and decently large coupon settlements (just under $40B, sandwiched between $52B in bills combined over Tuesday and Thursday) removing reserves from the system.

- SOFR was 4.19% Tuesday so it wouldn't be surprising if it weren't far below the 4.25% SRF rate today, making it a closer-than-usual tradeoff.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

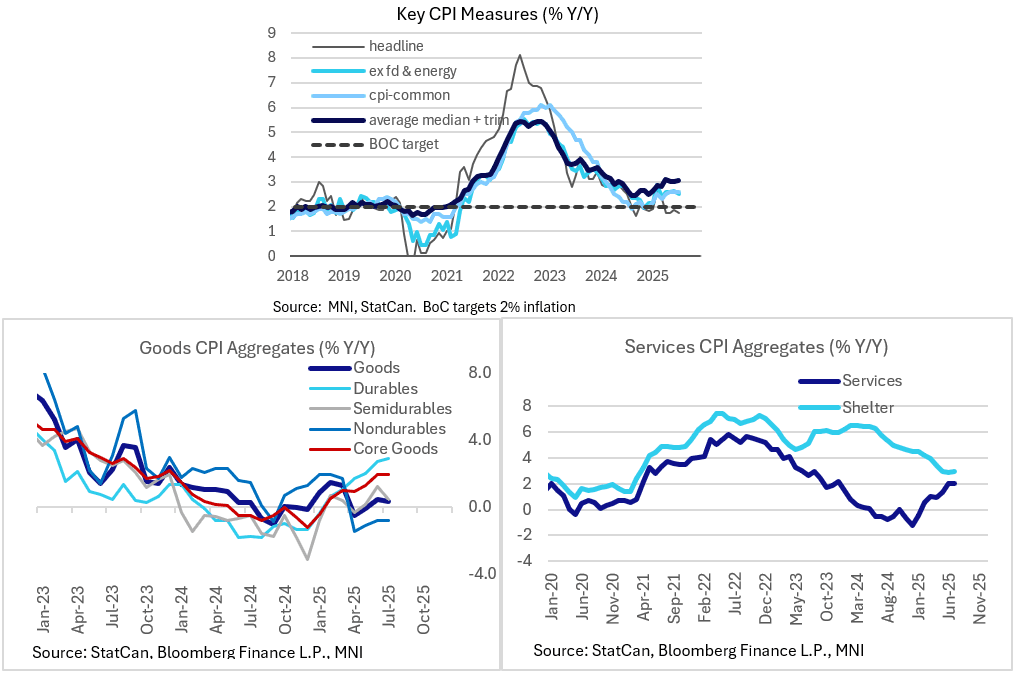

CANADA: Analysts Unsure CPI Would Impact BOC Decision (3/3)

Some analyst expectations for the August inflation report. While analysts aren't convinced that the report will have much bearing on the BOC decision on Wednesday, due in large part to the fact that the rate deliberations will have all but concluded by Tuesday, a few have noted that there may be an impact if there is a significant surprise.

- BofA - "expect downside pressure from transportation (gasoline) inflation and from household operations, furnishings & equipment".

- BMO: " In recent days, pump prices have somehow climbed above year-ago levels nationally, even with the consumer carbon tax having been axed and world oil prices down about 10% y/y. While the Bank typically looks past swings in gasoline, it’s no help to inflation expectations with pump prices suddenly flaring for no obvious reason."

- CIBC: "Inflation likely heated up slightly in August, albeit not by enough to prevent the Bank of Canada restarting interest rate cuts the next day. The expected acceleration in headline inflation, to 1.9% y/y from 1.7%, will be driven largely by base effects, with the 0.0% monthly reading (0.2% SA) looking very unthreatening. Rent inflation is expected to decelerate, bringing the series a little more in line with figures showing declining asking rents. However, air transportation inflation could look stronger, as prices return closer to seasonal norms following a summer that saw more staycations rather than vacations. Core measures of prices (CPI-X, Trim and Median) are expected to post 0.2% m/m increases, which will keep their year-over-year rates broadly stable."

- Desjardins - "the removal of most counter-tariffs this month has reduced the upside risks to inflation. Barring any major surprises in the August CPI data, we expect the Bank of Canada to cut rates the following day."

- RBC: " Year-over-year CPI growth is still being biased lower by a drop in energy prices, in large part due to the removal of the consumer carbon tax from gasoline prices in most provinces in April. But, we expect headline price growth to tick up to 2.1% from 1.7% in July, and for price growth, excluding food and energy products, to rise to 2.8%. The BoC’s own preferred median and trim core CPI measures are expected to have held around 3% (the top end of the central bank’s inflation target), extending the trend seen over the summer."

- Scotia - "In terms of the NSA reading, August is typically a month in which there is low average seasonality in price swings. Gasoline prices may contribute up to 0.1% to CPI given an estimated 1½% m/m NSA rise. Food is likely to be a minimal influence. Shelter is estimated to be up to a 0.1% addition. There is high uncertainty around much of the rest of the basket...Some shops are holding off on their rate calls until seeing CPI. We feel we have enough information to merit not waiting as data dependency shifts down the list of considerations relative to the forward-looking considerations explained in the Bank of Canada section of this report."

USDJPY TECHS: Monitoring Support

- RES 4: 151.62 61.8% retracement of the Jan 10 - Apr 22 bear leg

- RES 3: 150.92 High Aug 1 and a key resistance

- RES 2: 149.81 76.4% retracement of the Aug 1 - 14 bear leg

- RES 1: 148.58/149.14 High Sep 8 / High Sep 3

- PRICE: 147.32 @ 20:20 BST Sep 15

- SUP 1: 146.21 Low Aug 14

- SUP 2: 145.86 Low Jul 24

- SUP 3: 145.69 Trendline drawn from the Apr 22 low

- SUP 4: 145.40 50% retracement of the Apr - Aug upleg

USDJPY continues to trade inside a range. Key short-term support to watch is 146.21, the Aug 14 low and a bear trigger. A break of this level would highlight a stronger bearish threat and highlight a range breakout. This would expose 145.40, a Fibonacci retracement. On the upside, clearance of 149.14, the Sep 3 high is required to reinstate a bullish theme. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend.

CANADA: Core Goods, Non-Shelter Services Eyed (2/3)

Recent trends within CPI categories:

- Overall goods inflation ticked lower to 0.3% Y/Y in July from 0.5% prior.

- Core goods are seen remaining relatively steady, having printed 2.0% Y/Y in both June and July in a steadying out after a 1.1pp rise in the previous 2 months. Durable goods prices (2.9% Y/Y after 2.7% for a 30-month high) have been picking up (motor vehicles, and household durables such as furniture were culprits in July, pointing to tariff effects), but conversely semi-durables inflation has flattened out (apparel prices decelerated).

- Services inflation dipped to 2.8% Y/Y in July from 3.0% prior, led by non-shelter services (multiple volatile categories were responsible here, including airfares/traavel services).

- Shelter costs picked surprisingly picked up despite a continued dip in mortgage interest costs, due to a pickup in rent prices (5.1% Y/Y, up 0.4pp from prior) and utility costs. This is probably less worrying to the BOC due to the long-standing deceleration of shelter prices with more expected in the pipeline, though further stubbornness in disinflation could pique interest.

- In headline, Y/Y energy prices are seen being less of a drag going forward as the year-on-year effects wear off from the removal of the consumer carbon tax in April. Food prices have been worryingly high through the summer (though not necessarily tariff related, with weather conditions contributing, per StatCan), as grocery inflation rose to 3.4% in July from 2.8% in June.