STIR: Fed Pricing Looks Through Data, Modest Dovish Move On Lower Oil

May-07 12:55

Little net movement in US$ STIRs following the 08:30 NY data as the lower-than-expected initial and ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US REDBOOK: STORE SALES +7.6% WK ENDED APR 04 VS YR AGO WK

Apr-07 12:55

- MNI: US REDBOOK: STORE SALES +7.6% WK ENDED APR 04 VS YR AGO WK

- US REDBOOK: APR STORE SALES +6.8% VS YR AGO MO

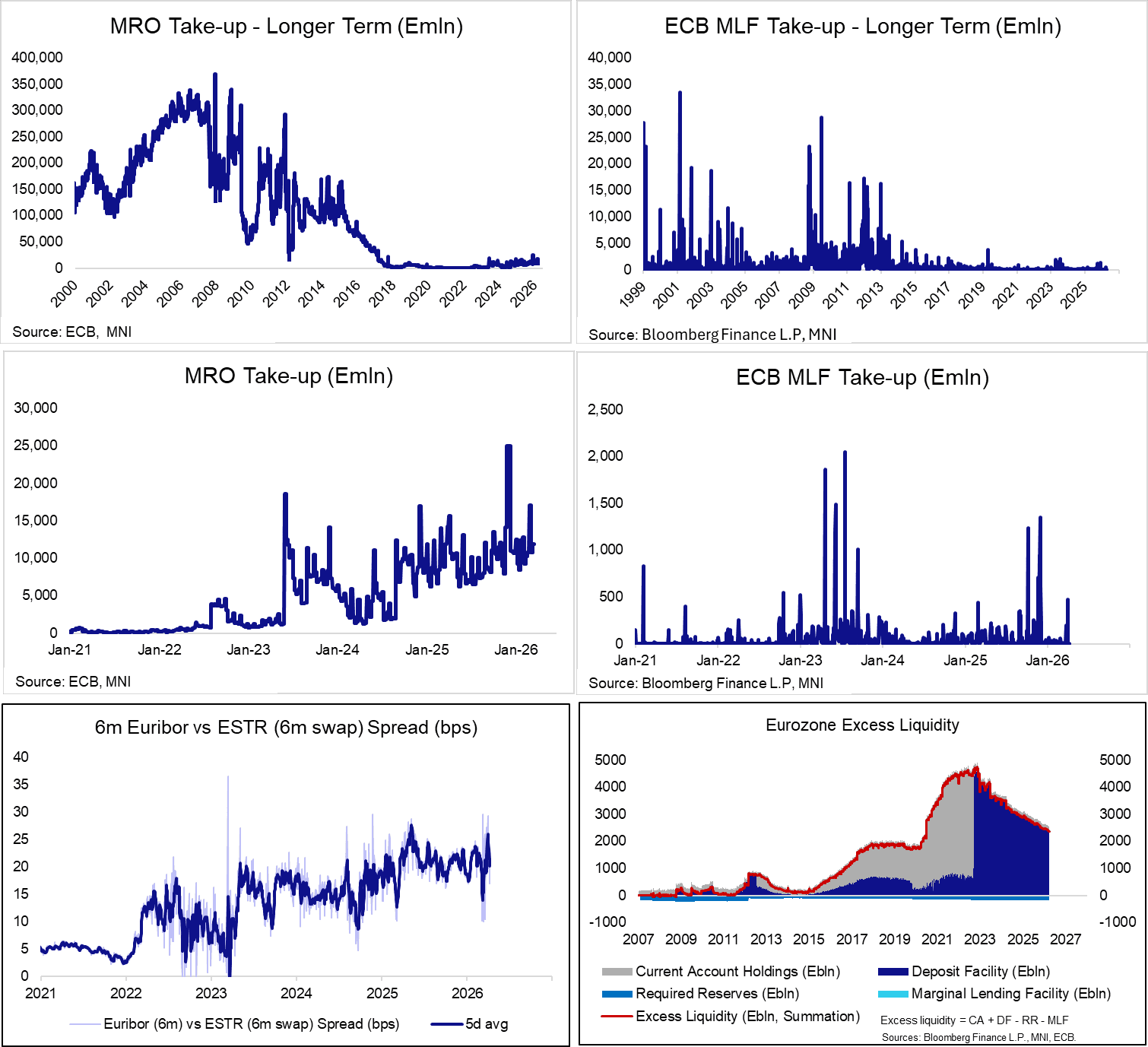

ECB: MRO Take-up Below End-March Levels, ECB Relaxed On Reserve Dynamics

Apr-07 12:47

Take-up at today’s ECB MRO operation was E11.9bln, versus E10.8bln last week at E17.1bln the week prior (ahead of quarter end). Take-up has been rising incrementally since 2024, but remains immaterial on a longer-term basis. Broadly speaking, reserves remain abundant.

ECB staff released a blog post on the development of bank reserves last week. Some highlights below:

- “Banks representing 26% of all euro area banking assets now operate close to what was indicated as their preferred level of reserves, up from 15% a year earlier”.

- Staff observed that “Banks are borrowing and lending in the markets effectively, which is helping redistribute reserves smoothly across banks and countries. There are no signs of fragmentation”.

- “Short-term interest rates, both secured and unsecured, remain close to the ECB’s DFR. Until now, money market funding conditions have been favourable compared with the terms for borrowing through the SROs. Therefore, banks have met almost all their liquidity needs through the money markets. However, as reserves continue to decline it will be important for banks to be ready to use Eurosystem operations as routine tools to manage their liquidity and to support market-making.”

- “The share of overnight repo trades above the DFR has increased to 40%, but this does not reflect funding pressures for banks. In fact, banks – including those with less abundant reserves – are still borrowing at rates just below the DFR on average….Instead, repo rates above the DFR mainly reflect cash demand from hedge funds which are willing to pay the spread to fund their investment strategies in other market segments”.

SONIA OPTIONS: Call Spread buyer

Apr-07 12:44

SFIM7 97.50/98.00cs, bought for 2 in 4.5k.