UK DATA: Feb Flash PMI Will Make For Difficult Reading For the MPC

Feb-21 09:38

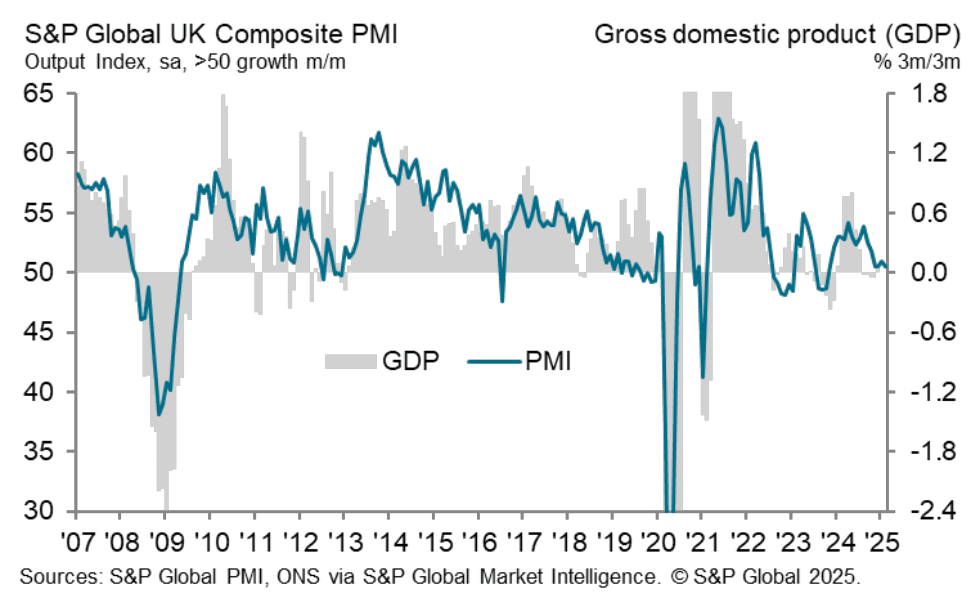

The UK February flash manufacturing PMI dipped to 46.4 (vs 48.5 cons, 48.3 prior), while services was a touch stronger than expected at 51.1 (vs 50.8 cons and prior). This was the weakest manufacturing PMI since December 2023.

The survey will make for difficult reading for the BOE MPC, with demand weakness weighing on orders and employment and input cost increases being passed onto output charges.

Key notes from the release:

- “Private sector firms indicated a further steep decline in staffing numbers, largely in response to higher payroll costs and weak demand”

- “Anecdotal evidence often cited a lack of new work to replace completed projects and cautious spending among clients in response to general concerns about UK economic prospects. Some service providers also noted that heightened global business uncertainty had weighed on growth in February”.

- In manufacturing, “lower production was attributed to falling sales in both domestic and overseas markets, alongside a lack of confidence regarding the near-term demand outlook”.

- “Moderate reduction in total new business received by UK private sector firms”…” respondents widely commented on cutbacks to clients’ budgets and lacklustre business investment spending”.

- “Input cost inflation accelerated for the fourth month running”… “. Intense cost pressures were mainly linked to higher salary payments and the impact of suppliers seeking to pass on forthcoming increases in employers’ National Insurance”…”The latest survey also pointed to robust increases in prices charged by both manufacturers and service providers”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: Estoxx call spread seller

Jan-22 09:36

SX5E (21st Feb) 5200/5300cs, sold at 44.60 in 12k.

EGB SYNDICATION: Spain 10-year Obli: Revised guidance

Jan-22 09:32

- Guidance: 3.45% Oct-34 Obli (mid) +6bp area (+/1bp WPIR) (Guidance was +8bp area)

- Size: EUR benchmark (MNI expects E10-15bln)

- Books in excess of E150bln

- Maturity: 30 April 2035

- Coupon: Short first

- ISIN: ES0000012O67

- Settlement: 29 January 2025 (T+5)

- Bookrunners: BBVA, CACIB, DB (B&D/DM), JPM, MS, SANTANDER

- Timing: Books open, today's business

From market source

EGBS: Spreads Continue Recent Tightening, Some Near Key Levels

Jan-22 09:31

Zooming out, the general theme of spread tightening seen over the last week or so has been driven by several factors:

- Notable demand at the early round of ’25 EGB syndications (which included long end OAT supply).

- Continued narrowing of ASW spreads in Germany (linked to German fiscal/supply risk, as well as increasing free float).

- Dovish ECB repricing countering some of the early January hawkish adjustment

- Fresh record highs across some of the major European equity indices.

- An associated move lower in EUR implied FI vol. metrics.

- Some of the major EGB/Bund spreads trade near key levels.

- OAT/Bunds once again struggles to trade meaningfully below 75bp, with French fiscal and political risks continuing to limit spread tightening below that level, at least for now.

- BTP/Bunds near multi-year lows, last ~107bp.