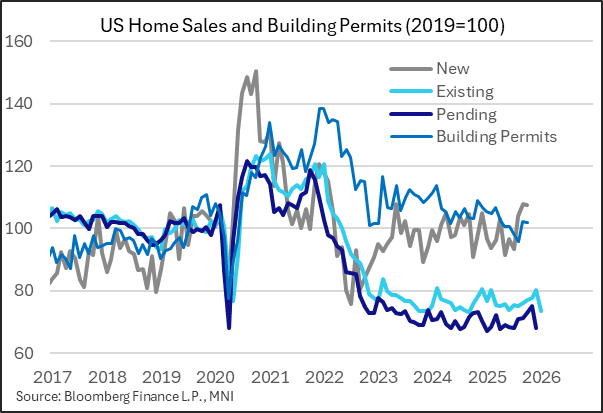

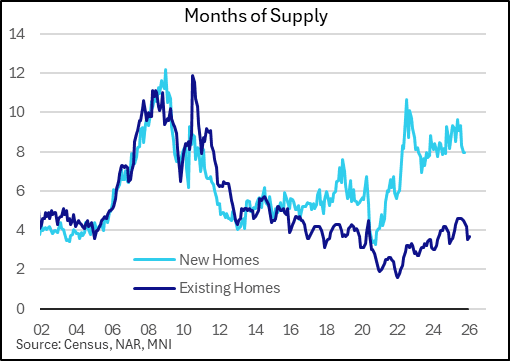

US DATA: Existing Home Sales Pull Back, Activity Still Thawing Slowly

Weakness in existing home sales in January look to have been partly driven by bad weather, but it's not totally unexpected given that the drop was presaged by a pullback in pending sales. Sales came in at 3.91M SAAR, down from 4.27M in December and below the 4.15M expected for the worst monthly figure since September 2024.

- Per the NAR's Chief Economist Lawrence Yun, "“The decrease in sales is disappointing. The below-normal temperatures and above-normal precipitation this January make it harder than usual to assess the underlying driver of the decrease and determine if this month’s numbers are an aberration".

- Bad weather was a problem in January but the 8.4% M/M drop shouldn't have been a major surprise given that the previously reported pending sales (representing signed contracts) fell 9.3% in December - and that usually leads existing sales (representing closings) by a month or two.

- We would also add that affordability and supply remain issues. Despite a recent pullback in mortgage rates to post-September 2024 lows, which helped spur a jump in pending sales, the descent has stalled in recent weeks, meaning absent price pullbacks (median prices rose 0.9% Y/Y in January), affordability will remain low.

- While inventory is low on a historical basis, at 3.7 months' equivalent of sales, this is above the norm for the Januarys of 2020-2024 as it's not a prevalent time for moving homes, and it's trending higher overall. So the market is thawing, but only very slowly, and will require a catalyst (lower rates/a jump in unemployment) to get things moving.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Clears Resistance

- RES 4: 186.73 Bull channel top drawn from the Feb 28 low

- RES 3: 186.41 2.618 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 2: 185.77 2.500 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 1: 185.54 High Jan 13

- PRICE: 185.20 @ 16:11 GMT Jan 13

- SUP 1: 183.32/182.64 20-day EMA / Low Jan 8

- SUP 2: 182.25 Low Dec 19

- SUP 3: 181.59 50-day EMA

- SUP 4: 180.50 Low Dec 8

The trend needle in EURJPY continues to point north. The cross has traded to a fresh cycle high, clearing resistance at 184.92, the Dec 22 high. The move higher confirms a recent bull flag on the daily chart and confirms a resumption of the uptrend. This signals scope for a climb towards 186.73, the top of a bull channel drawn from the Feb 28 low. Key support to watch lies at 181.59, the 50-day EMA.

COMMODITIES: Crude Spikes Amid Geopolitical Concerns, Silver At Record High

- Crude prices have spiked on Tuesday amid mounting geopolitical concerns in the middle east as President Trump said it was a good idea for US citizens evacuate from Iran.

- WTI Feb 26 is currently up by 2.7% at $61.1/bbl.

- Trump told Iranians to keep protesting and that “help is on its way” in a social media post today, the clearest indication yet of possible US intervention.

- Iran has vowed to respond to any US strikes which could sew disruption around production and flow hubs in the Persian Gulf, the site of 20% of global oil supply.

- Despite today’s move, the trend structure in WTI futures remains bearish and recent gains still appear corrective - for now.

- However, note that resistance at the 50-day EMA, at $58.48, has been breached. This signals scope for a stronger corrective phase.

- Key resistance at $61.25, the Oct 24 high, has also been pierced. Clearance of this level would highlight a stronger reversal, opening $64.97, the Sep 26 high.

- Elsewhere, silver also rallied sharply to a fresh record high amid haven demand on Tuesday, with price currently up 2.8% at $87.5/oz.

- The move has seen price pierce $87.355, a Fibonacci projection, a clear break of which would open $90 round number resistance.

- Gold also rose to an all-time high of $4,634.55/oz earlier in the session, before unwinding today’s gains to trade broadly unchanged around $4,595.

US TSYS: Late SOFR/Treasury Option Roundup

SOFR & Treasury options flow remained mixed Monday but tended toward better downside put flow with few exceptions. Note late buying of Jun'26 and Sep'26 SOFR call structures. Underlying futures holding modest gains in late trade - still well off this morning's knee-jerk post-CPI rally. Projected rate cut pricing vs. late Monday levels (*): Jan'26 steady at -1.2bp, Mar'26 at -6.3bp (-6.6bp), Apr'26 at -10.7bp (-11.2bp), Jun'26 at -22.5bp (-23.6bp).

- SOFR Options:

- +23,000 SFRU6 96.75/96.70/97.25/97.50 call condors 6.0 ref 96.76

- +7,500 SFRM6 96.43 puts 0.0 over 0QM6 96.37 puts

- Block, 13,100 SFRU6 96.25/96.50 put spds 4.25 net vs. 96.76/0.18%

- -10,000 2HQ6 96.25/96.43/96.62 put trees, 5.5 ref 96.655

- +8,000 3QU6 96.00/96.37 put spds, 14.5

- +4,000 SFRM6 96.50/96.62/96.75 call flys, 1.75

- -10,000 SFRM6 96.18/96.37/96.56 put flys, 8.0-7.75 ref 96.59

- Block/pit, over 17,500 SFRM6 96.31/96.37 put spds, 1.0 net vs. 96.585/0.10%

- +6,500 0QH6 97.00 calls vs. 2QH6 97.06/97.25 call spds, 1.0 net

- +5,000 SFRH6 96.56/96.68 call spds, 0.5

- over 13,500 SFRM6 96.43/96.56/96.62/96.75 call condors ref 96.57

- Block, 2,500 SFRU6 96.75/97.00/97.75 2x3x1 broken call flys, 8.0 net vs. 96.745

- 3,000 0QH6 96.68/96.75/96.87/96.93 put condors ref 96.805

- Block, 5,000 SFRH6 96.37/96.43 call spds, 1.5 ref 96.39

- Treasury Options:

- +25,000 TYH6/TYK6 110.5 put spds, 20 net vs. 112-08.5/0.14%

- 6,277 FVG6 108.75/109.25 put spds, 12.5 net ref 109-03.5

- +20,000 TYK6 114.5 call, 20 vs. 112-05.5/0.16%

- +50,000 wk1 TY 117 calls, 1

- +10,000 TUM6 103.75/104.12/14.37 broken put flys, 1.0

- 5,000 TYH6 111/113 call spds

- Block, -20,000 TYH6 111 puts, 10 vs. +25,0000 TYK6 114.5 calls, 19

- paper -11,000 TYH6 111 puts 10 separately

- +25,000 TYK6 115 calls, 15 ref 112-07, appr vol 4.82%

- +13,000 wk3 FV 109 straddles, 17-17.5

- over 23,100 TYG6 111.75 puts, 9 last

- 3,250 FVG6 108.75/109 put spds ref 108-31 to -31.25

- over 7,500 TYG6 111.75 puts, 9 last ref 112-02

- 3,300 TYG6 111 puts ref 112-02.5

- 1,500 TYG6 111.25/111.5/112 broken put flys ref 112-05.5