US DATA: Existing Home Inventories Show Surprising Tightness, But Remain Weak

Dec-19 16:10

Existing home sales picked up sharply in November on a seasonally-adjusted basis, with the 4.8% M/M increase the largest since February, to the highest level since March at 4.15M annualized. That also represented a 6.1% Y/Y gain, the biggest rise since June 2021 (when sales were soaring versus the early pandemic period).

- Notably, inventory did not rise to match the rise in sales, and at 3.8 months it represented a fall from 4.2 in October and was the first sub-4 months reading since May. Median sales prices rose 4.7% Y/Y to $406.1k.

- Existing home sales remain subdued overall, however, both outright (peaking at 6.6M in 2021, with October's 4.15M very close to the pandemic lockdown lows) and relative to new home sales (which while at merely 600k are at least roughly around pre-pandemic levels). Again this is largely related to financing.

- While the NAR press release notes that the rise in existing sales is in part owing to "consumers get[ting] used to a new normal of mortgage rates between 6% and 7%", the broader data suggests housing sales activity remains mired in a deep recession with buyers and sellers at a standoff.

- This is only likely to be resolved by lower rates, allowing buyers greater affordability and sellers to ability to move without incurring a substantially higher mortgage rate, and/or higher unemployment which forces sales.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

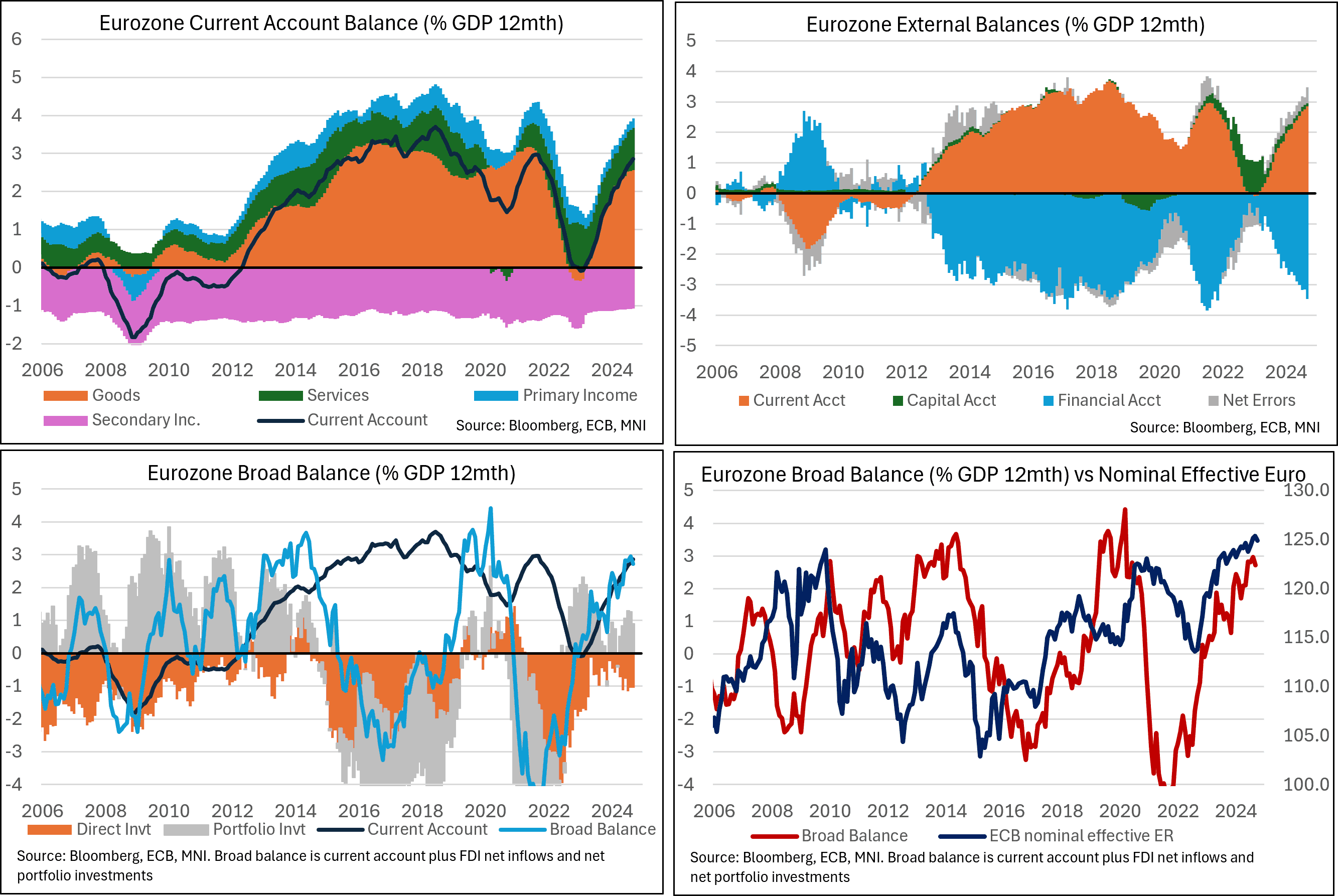

EUROZONE DATA: Another Increase In The 12M Rollling Current Account to GDP

Nov-19 16:10

The Eurozone current account surplus registered a 20th consecutive monthly increase on a 12m rolling basis to GDP in September, rising to 2.9% of GDP (vs 2.8% prior). This was the largest surplus since September 2021.

- In line with September’s monthly goods trade data, the goods surplus rose to 2.6% of GDP (vs 2.5% prior). The primary income surplus ticked up to 0.3% of GDP (vs 0.2% prior), while the services and secondary income balances were steady at 1.1% and -1.1% respectively.

- In the financial account, the net direct investment outflows (again 12M % GDP) fell to 1.0% (vs 1.1% prior) while the net portfolio investment inflows fell to 0.9% (vs 1.3% prior).

- Since June this year, the net direct investment outflow has averaged 1.0% of GDP. This compares to 0.7% of GDP in the first 5 months of this year and 0.9% in 2023.

- We have previously highlighted falling direct investment inflows into the four major Eurozone economies as a drag on aggregate gross fixed capital investment growth (see here).

- Continued weakness in these flows would provide some counter to the post-covid growth in the broad balance (current account + net direct and portfolio investment inflows), which had contributed to an appreciation of the nominal effective euro exchange rate.

PIPELINE: $2.5B Republic of Turkiye +5Y Sukuk Launched

Nov-19 16:02

- Date $MM Issuer (Priced *, Launch #)

- 11/19 $2.5B #Republic of Turkiye +5Y Sukuk 6.55%

- 11/19 $500M Emirates NBD WNG 5Y Reg S +90

- 11/19 $Benchmark Vistra Operations 2Y +115a, 10Y +160a

- 11/19 $Benchmark International Development Assn 5Y SOFR+48a

- 11/19 $Benchmark Lloyds 4NC3 +110a, 4NC3 SOFR, 11NC10 +145a

- 11/19 $Benchmark National Australian Bank (NAB) -3Y +60a, -3Y SOFR

- 11/19 $Benchmark Alibaba investor calls for US$ 5.5Y +90a, 10.5Y +115a, 30Y +130a (additional 4 tranches via CNH backed debt)

UK DATA: MNI UK Inflation Preview - October 2024

Nov-19 15:42

- After reaching its near-term trough in September, UK CPI is expected to increase in October, largely driven by utilities prices, but the main focus will remain on services inflation which is expected to remain broadly unchanged.

- Consensus expects the more important services CPI to print broadly around the same level as in September (MNI median 4.9%, MNI mean 4.91%, Bloomberg consensus 4.9%, BOE 4.97%). We remain wary of upside risks from air fares.

- We also see the potential for moves higher in clothing and second hand car prices within core goods.

- A decent surprise either way in services CPI could move the market, but if the upside risks that we have identified prevail to see a higher-than-consensus print we still think there is scope for cuts at least in February and May (which aren’t quite fully priced by the market yet). We therefore think there is potential for a bigger market move on a downside surprise.