EUR: EUR/USD- Tops Out Above 1.1600 For Now, Can It Challenge Lower Again ?

The EUR/USD range overnight was 1.1555-1.1617, Asia is currently trading around 1.1565, +0.05%%. The...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Curve Bull-Flattens As Investors Buy Value At Long-End

In early 2025, the JGB 2/40 yield curve broke above the well-established range that had been in place since late 2022. Following the initial steepening, the curve reverted to range trading, a pattern that has persisted to the present. It is now testing the lower bound of that range.

- Since late last year, steepening has been most pronounced in the 2/5 segment, with the 5-year sector viewed as relatively unattractive. Expectations of fiscal expansion under a Takaichi administration implied heavier debt issuance, reinforcing pressure on intermediates.

- In recent weeks, however, fiscal concerns appear to have eased following Prime Minister Sanae Takaichi’s historic election victory, prompting long-end buying and a flattening of the curve.

- Recent price action suggests investors have favoured the long end, taking advantage of the curve’s relative steepness. Weekly flow data indicate that offshore investors have returned as net buyers of JGBs in 2026, lending support to that move.

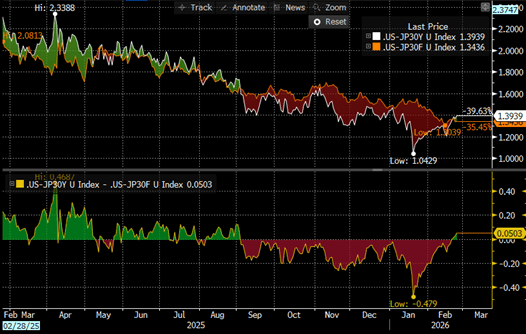

A simple regression of the US–JP 30-year yield differential against the US–JP 1Y3M swap spread — a useful proxy for expected relative policy paths over the coming 12 months — over the past two years suggested the 30-year spread was around 50bps too low in mid-January. That valuation gap has since been largely unwound as investors accumulated 30-year JGBs, with the US–JP 30-year spread now close to fair value (see chart).

Bloomberg Finance LP

JAPAN: Foreign Inflows Could Be Key Driver for JGB Yields in 2026

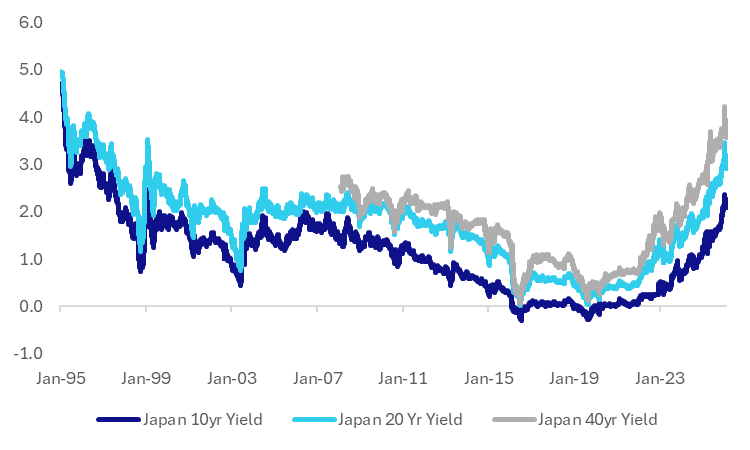

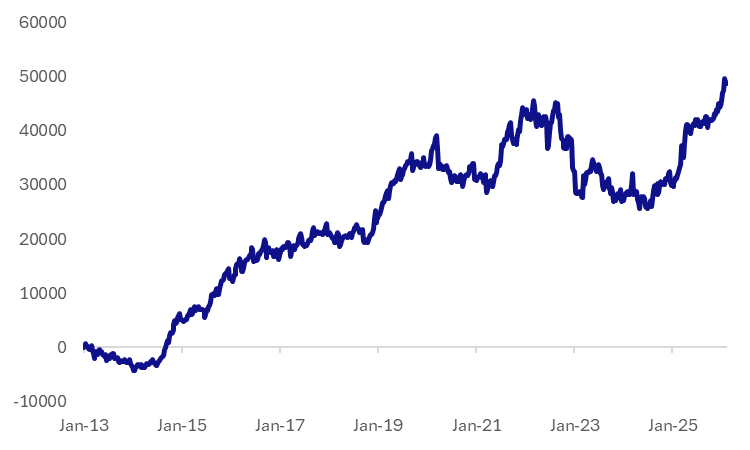

The 2025 to early 2026 surge in JGB yields created levels not seen in a generation. Even with the recent correction off recent highs for longer dated yields, we are still very elevated by historical standards (see the chart below). As a perpetual underweight for global bond investors, valuation has rarely been a driver for JGB investors due to low yields. Now perhaps this tide is close to turning (or has perhaps already begun). Weekly investment flow data shows net offshore inflows returning to JGBs in 2026, but this only brings cumulative inflows to marginally positive versus early 2022 levels, see the second chart below. BBG also notes: "Futures are signaling sustained demand from overseas money managers who account for more than 70% of trading volume. Foreign investors were net buyers of 4,717 JGB futures contracts in the week of Feb. 9, following an even larger 8,626-contract purchase the week before which the most since mid-October, data from the Osaka Exchange show."

- Market pricing in terms of the BoJ outlook, has around 2 rates hiked priced by year end, which would take the policy rate to 1.25%. The IMF sees BoJ neutral rates around 1.50% and expects the central bank to get there by around mid next year.

- Given much of the rate hikes are priced in, easing out of perpetual underweights could be fortuitous to performance in 2026. Moving (at the very least) to a more neutral view on Japan bonds is carry positive for investors.

- The USD/JPY outlook/trend will also be important. The consensus for USD/JPY to end 2026 at 149.00, versus current level around 155.00. The most commonly used global bond indexes had a return profile in 2025 that reflected movements in global government bond markets and the impact of currency translation for international investors.

- US dollar investors with unhedged exposure to these indexes (the largest cohort of users of these indexes) saw a positive returns of 7.5-8.00% during the year, whilst euro-based unhedged investors saw negative returns in the region of -4-5%. 80% of WGBI investors are USD based.

- Currency-hedged results were more tightly clustered across base currencies. The comparison underscores how, in a year marked by shifting rate expectations and active currency markets, the decision to hedge or remain unhedged was a meaningful driver of realized performance outcomes across different investor perspectives.

Fig 1: JGB Yields, Long Run Trends

Source: Bloomberg Finance L.P./MNI

Fig 2: Cumulative Offshore Net Inflows To Japan Bonds - JPY Bn

Source: Bloomberg Finance L.P./MNI

CHINA PRESS: China A-Shares Likely To Rise After New Year Festival

Hong Kong equities’ strong performance on the final day of the Lunar New Year holiday has reinforced institutional expectations of a “strong opening” for mainland A-shares in the Year of the Horse, Yicai reports. On February 23, the Hang Seng Index rose 2.53% to close at 27,081.91 points, while the Hang Seng Tech Index climbed 3.34% to 5,385.35 points. Yang Chao, chief strategy analyst at Galaxy Securities, told Yicai that the prominence of technological themes — including robots, drones, and AI cloud systems — in this year’s Spring Festival Gala TV show may generate short-term sentiment support for markets. Over the past 20 years, the Shanghai Composite Index has averaged a 1.2% gain in the five trading days following the Spring Festival. The return of pre-holiday risk-averse funds, together with supportive policy conditions, was expected to help revive trading activity quickly after mainland markets reopen, Yicai said.