LOOK AHEAD: Eurozone Final PMIs After Further Improvement In Flash

Aug-29 19:30

- The Eurozone final PMI surveys for August are due for manufacturing on Monday and services on Wednesday.

- The flash PMIs were surprisingly robust as the composite increased to 51.1 for another 0.2pt improvement, up from the 50.4 averaged in 1H25 and its highest since May 2024.

- Drivers were mixed however, with manufacturing leading the monthly improvement to 50.5 whilst services cooled to 50.7 as the two closed what has been sizeable divergence.

- This week's final readings should confirm that countries other than Germany and France have still been outperforming but by less than previous months.

- Since the flash PMI release, the European Commission's economic confidence index was softer than expected in August as it shifted back close to levels averaged in 1H25 and is comfortably below its long-term average.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (U5) Fades on Fed

Jul-30 19:24

- RES 4: 112-15 61.8% retracement of the Apr 7 - 11 sell-off

- RES 3: 112-12+ High Jul 1 and a bull trigger

- RES 2: 111-28 High Jul 3

- RES 1: 111-14+ High Jul 22 & Jul 30

- PRICE: 110-31+ @ 20:21 BST Jul 30

- SUP 1: 110-19+/08+ Low Jul 24 / Low Jul 14 & 16

- SUP 2: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 3: 109-28 Low Jun 6 and 11

- SUP 4: 109.25 Low May 27

Treasury futures traded higher Tuesday, but faltered into the Wednesday close on the Fed decision. Recent gains resulted in a break of the 20-day EMA, strengthening the recovery that began mid-July. Note too that resistance at 111-13+, the Jul 10 high, has been pierced. A clear break of it would highlight a stronger reversal and open 111-28, the Jul 3 high. Key support is 110-08+, the Jul 14 and 16 low. Clearance of this level would reinstate a bearish theme. First support is at 110-19+, the Jul 24 low.

FED: Rough Transcript of Chair Powell's July Press Conference

Jul-30 19:22

Rough Transcript of Fed Chair Powell's post-July FOMC press conference is here(PDF)

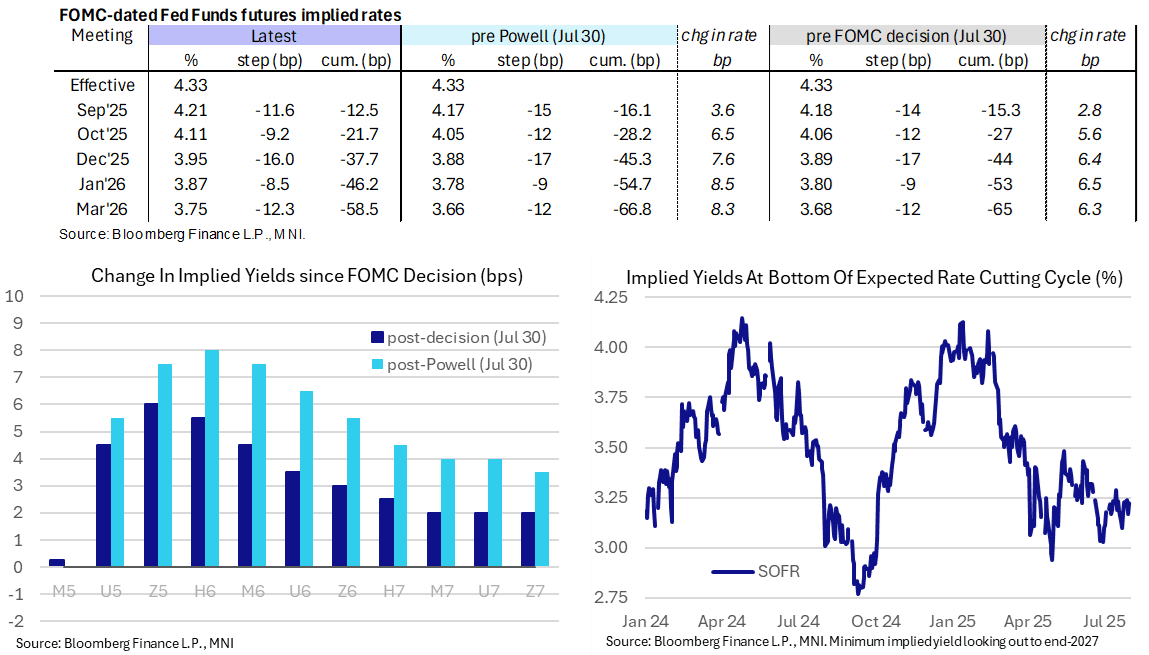

STIR: Hawkish Adjustment Extended Through Presser, 50/50 Sept Cut Odds

Jul-30 19:20

- The hawkish reaction in Fed rates extended throughout Powell’s conference, comfortably more than reversing the small dovish reaction to the initial decision statement.

- Fed Funds cumulative cuts from 4.33% effective: 12.5bp Sep (vs 16bp pre-Powell and 15.5bp pre decision), 21.5bp Oct, 37.5bp Dec (vs 44bp per decision), 46bp Jan and 58bp Mar (vs 65bp pre decision)

- Largest increases in SOFR implied yields through Powell’s press conference are in the H6, +8bp for the same move on the day and +5.5bp since the FOMC decision.

- The terminal implied yield remains in the H7, at 3.225% (+5.5bp on the day) but still easily within the 3.1-3.3% range seen through July.

- The moves were initially driven by Powell seeing modestly restrictive policy as appropriate, saying we have made no decisions about the September meeting and we’re still a ways from seeing where things settle down. Adding to this rhetoric, he later said it’s really hard to say whether will have enough information to cut in September.