STIR: Euro Rates Holding Retreat Off Highs, Still 85% Odds Of April ECB Cut

- European rates have pared a large portion of the day’s sharp rally seen at the US crossover this morning with ECB April cut developments and China trade retaliation.

- It trims Euribor contracts to 3.5-6 ticks higher on the day (gains led by H6).

- The move off highs is on US gyrations first after a solid payrolls report before a greater move on some optimism of a softening in tariff stance from Trump’s Vietnam discussions and Fox’s Gasparino’s “scoop” on Bessent giving some pushback on Trump’s “hard line stance” and finally Powell’s patient remarks.

- Euribor terminal implied yields at 1.79% are 15bp below levels prior to Trump’s “Liberation Day” tariffs although that compares with a 42bp slide to 2.98% for SOFR.

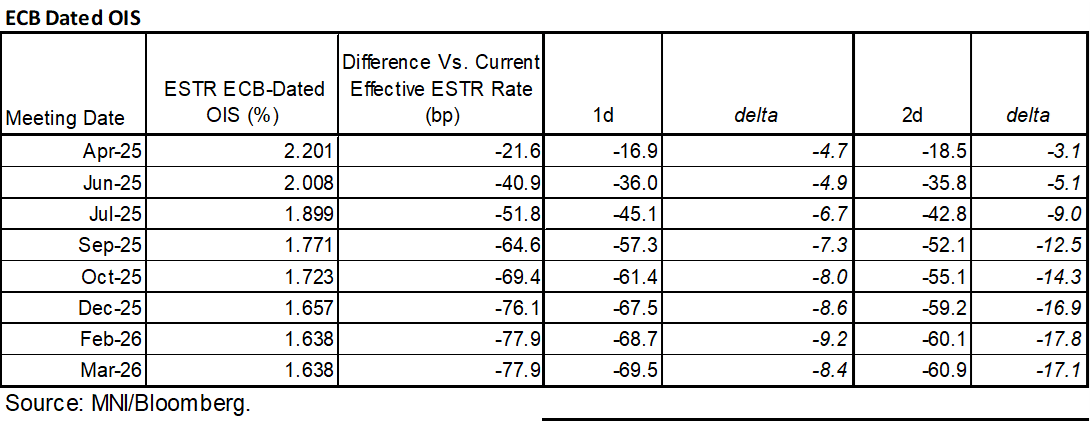

- ECB-dated OIS shows ~85% odds of an April cut with today’s dovish MNI exclusive countering a more hawkish paywalled think tank piece yesterday.

- It builds to a cumulative 76bp of cuts from current levels to year-end.

- ECB comments in the wake of the tariffs haven’t added much to the debate: Nagel (hawk) said they will threaten global economic stability but also put monetary policy progress to the test with the ECB having to reassess the situation; Kazimir (hawk) said they will “weaken economic growth, dent positive sentiment in the labor market, and indeed have some impact on prices. Tariffs primarily affect prices”; and Stournaras (dove) said US tariffs are no obstacle to an April rate cut.

- Exec Board member Cipollone is up next but could see limited mon pol discussions, talking on the interplay between tax and financial regulations on Monday (no text). Tariff deliberations will remain the key driving force although EZ retail sales for Feb and Germany IP and trade for Feb offer data interest.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Update: $26B Mars 8Pt Jumbo, 8th Largest on Record

- Date $MM Issuer (Priced *, Launch #)

- 03/05 $26B Mars $2B 2Y +50, $3.25B 3Y +60, $4.5B 5Y +75, $2.75B 7Y +85, $5B 10Y +95, $2.75B 20Y +110, $4.75B 30Y +117, $1B 40Y +127

- 03/05 $1.5B Axon 5NC2, 8NC3

- 03/05 $1B *KommuneKredit WNG 5Y SOFR+44

- 03/05 $750M #Republic of Armenia 10Y 7.1%

- 03/05 $500M Acadia Health 8NC3

- 03/05 $500M Forestar Group 8NC3

GERMANY: Defence & Infrastructure Stimulus-Analyst Views

Download Full Article Here

The German government has signalled perhaps the most significant step change in decades in its thinking about the country’s role in European security and regarding its long-standing commitment to fiscal prudence. Late on 4 March, the parties set to form the next governing coalition announced an agreement that will see a major increase in federal and state government funding on defence and infrastructure.

Below, we outline the nature of the proposals put forward and provide a round-up of analyst views on the impact of the announcement.

US 10YR FUTURE TECHS: (M5) Overbought But Remains Bullish

- RES 4: 112-23+1.618 proj of the Jan 13 - Feb 7 - Feb 12 price swing

- RES 3: 112-18 2.0% 10-dma envelope

- RES 2: 112-13 1.500 proj of the Jan 13 - Feb 7 - Feb 12 price swing

- RES 1: 112-01/02 High Mar 4 / 1.382 proj of Jan 13-Feb 7-12 swing

- PRICE: 111-06 @ 16:34 GMT Mar 5

- SUP 1: 110-23/110-00 Low Feb 28 / High Feb 7

- SUP 2: 109-21 50-day EMA and a key near-term support

- SUP 3: 108-21 Low Feb 19

- SUP 4: 108-03+ Low Dec 12 and a bear trigger

Treasury futures traded to a fresh cycle high Tuesday, reinforcing current bullish conditions. The contract has pierced resistance at 111-22+, Dec 3 ‘24 high. A clear break of this level would strengthen a bullish theme and open 112-02 and 112-13, Fibonacci projection points. Note that the daily trend condition is overbought, a pullback would be considered corrective and allow the overbought set-up to unwind. Firm support is at 110-00, the Feb 7 high.