HUF: EURHUF Trend Condition Remains Bullish, Local Markets Remain Shut

A firmer course for the HUF over the Christmas period has seen USDHUF pull back over 1.5% from cycle highs in the past week. Still, the pair remains above the 20-day EMA with the forint close to 12% weaker versus the greenback on a year-to-date basis – putting it among the weakest performing EM currencies globally (with only RUB and TRY performing worse across EMEA).

- The broader trend condition for EURHUF remains bullish following the brief rally above resistance at 415.54, the Nov 29 high, earlier this month. A clear break would set sights on 418.50, a retracement level. Global risk sentiment and year-end flows will likely be the primary drivers amid the quiet economic calendar. December manufacturing PMI and November unemployment rate and trade balance figures are all due next week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Core PCE Seen On Track To Overshoot Median FOMC Forecast - 1000ET

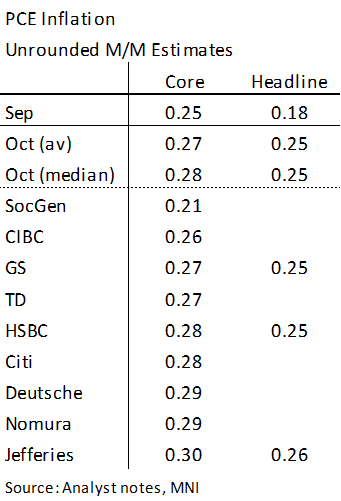

- Released today at the unusual time of 1000ET, Bloomberg consensus sees core PCE inflation at 0.3% M/M in October after the 0.25% M/M in September.

- We see unrounded estimates looking for a slightly ‘low’ 0.3%, with a median of 0.28% in the below table.

- From some of the more detailed estimates, Nomura expect small downward revisions of only 1bp to both Aug and Sept readings, whilst TD Securities see their estimate of 0.27% M/M for core PCE including a 0.39% M/M increase for supercore.

- Powell on Nov 14: “Estimates based on the consumer price index and other data released this week indicate that total PCE prices rose 2.3 percent over the 12 months ending in October and that, excluding the volatile food and energy categories, core PCE prices rose 2.8 percent.”

- Revisions do indeed look like they’re expected to be small then, seeing as a 0.28% M/M increase without any revisions would translate to 2.80% Y/Y after the 2.65% in September.

- We'll have a crude idea of revisions in the Q3 release that follows shortly beforehand at 0830ET as part of the second Q2 national accounts release.

- Importantly, whilst these upward base effects into year-end were already known, recent run rates would have continued to firm. A 0.28% M/M (again, assuming no revisions for a basic illustration) would see a three-month run rate of 2.8% after 2.3% in Sept and recent lows of 1.9% in Jul-Aug. Alternatively, and smoothing some recent noise, the six-month would inch a tenth higher to 2.4%.

- The latest trends are also, notably, leaving core PCE inflation on track to overshoot the median FOMC forecast of 2.6% for Q4 from the Sept SEP, revised down from June’s 2.8%. For a purely indicative exercise, a 0.28% M/M increase in Oct followed by two 0.20% readings would see 2.9% Y/Y in Q4, in line with the (presumably) most hawkish members considering the FOMC range of 2.4-2.9% for Q4.

US DATA: GDP Revisions And Scope For Core PCE Rounding Surprise – 0830ET

The second release for Q3 national accounts comes at 0830ET along with jobless claims and preliminary durable goods amongst others. It will include revisions for real GDP growth and its breakdown along with the first estimate for GDI.

- Bloomberg consensus doesn’t see a reason to diverge from the 2.8% annualized for real GDP growth flagged in the advance release, another robust quarter after the 3.0% in Q2.

- The advance release indicated that domestic demand played a greater role than was the case in Q2 (adding 3.6pps to quarterly GDP growth vs 2.8pps in Q2) and we’ll look to see if that’s still the case after revisions. Private consumption (seen unrevised at 3.7%) can give a quick idea here with what’s currently estimated to have been its strongest quarter since 1Q23.

- We also watch for the first release of Gross Domestic Income in Q3. Recall that GDI growth had been notably lagging GDP growth before a large shift higher in the comprehensive revisions in September, something that multiple FOMC members have since noted.

- The quarterly data will also show revisions for core PCE inflation. No material revisions are expected (seen staying at 2.2% annualized after 2.8% in Q2) although it can easily round lower with the latest rate actually 2.16%. We’ll touch more on the subsequent monthly PCE released, unusually released at 1000ET today, in the following re-upped bullet.

FINLAND AUCTION PREVIEW: ORI Facility Tomorrow

Finland has announced it will be looking to sell up to a combined E300mln of the following RFGBs at its ORI Facility tomorrow, November 28:

- the 0.50% Sep-27 RFGB (ISIN: FI4000278551)

- the 2.95% Apr-55 RFGB (ISIN: FI4000566294)