EU CREDIT UPDATE: CREDIT UPDATE: EUR Market Wrap

Aug-30 11:20

- 2y/10y bunds are +1bp/-1bp – DM team flagged Eurozone flash headline and core inflation was in line with initial consensus at 2.2% Y/Y and 2.8% Y/Y. EZ services inflation accelerated to 4.2% Y/Y (vs 4.0% prior), underscoring cautious commentary from ECB Schnabel, who advocated for a gradual policy easing cycle in a speech today.

- Main/XO are +0.4bp/+4bp at 52.3bp/289bp while €IG/€HY looks flat/-1bp. Primary closed. Curve movers include Castellum 26s (-18bp on tender), Intermediate Capital Group (up to 5bp wider), Aroundtown (up to 6bp tighter).

- SXXP is +0.4% as are SPX futures. €IG movers include Aroundtown +4%, Inmobiliaria Colonial Socimi SA +3%, Kohamo +3%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: EU Bank call buyer

Jul-31 11:11

SX7E (16th aug) 150c, bought for 0.55 in 6k.

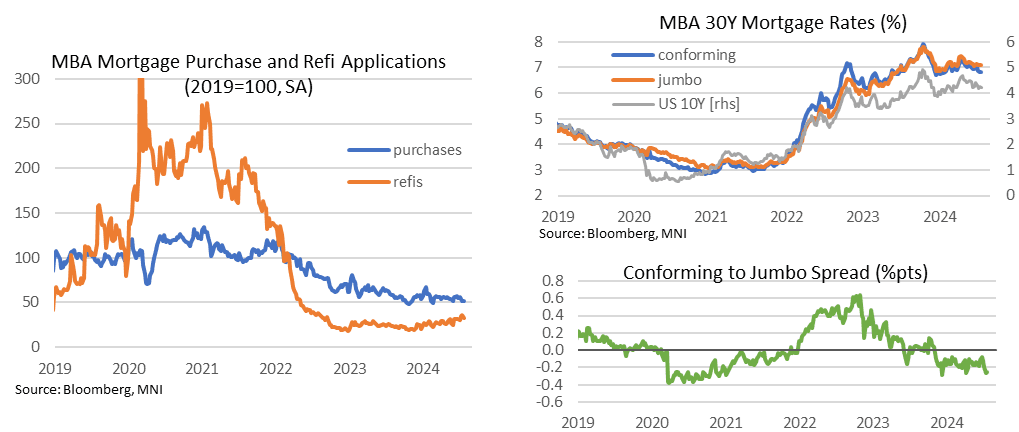

US DATA: Refi Mortgage Applications Pull Back From Highest In Two Years

Jul-31 11:09

- MBA mortgage applications fell a seasonally adjusted 3.9% last week and have now fully reversed a 16% jump back in early June.

- Purchase applications fell further (-1.5% after -4.0%) but refinance applications saw a greater decline with -7.2% after 0.3% the week prior and a particularly strong 15.2% the week before that had left refi activity at its highest since Aug 2022.

- Purchase applications continue to have seen little relief from the 30Y mortgage rate pulling back off recent highs, unchanged at 6.82% for its lowest since February.

- This recent rate easing still hasn’t really been reflected in jumbo loans though, where the rate of 7.07% (-2bps after +2bps) sees a regular-jumbo spread of -25bps remain at one of the most negative readings since late 2020/early 2021 in a potential sign of a tightening in lending conditions.

US MBA: REFIS -7% SA; PURCH INDEX -2% SA THRU JULY 26 WK

Jul-31 11:00

- US MBA: REFIS -7% SA; PURCH INDEX -2% SA THRU JULY 26 WK

- US MBA: UNADJ PURCHASE INDEX -14% VS YEAR-EARLIER LEVEL

- US MBA: 30-YR CONFORMING MORTGAGE RATE UNCHANGED AT 6.82%