EU CREDIT UPDATE: CREDIT UPDATE: EUR Market Wrap

Apr-18 10:23

- 2y/10y bunds are flat/-1bp with our DM team earlier flagging a modest pullback in market-based EUR inflation expectations - in part due to softening energy prices – as working against any pullback in safe haven demand that would be implied by reports that Israel will delay retaliation on Iran until after the Passover period.

- Main/XO are -1bp/-2bp while FICM shows €IG/€HY at -0.7bp each with swap spreads flat – Energy looks the best performing sector while Comms, Cons Disc and Sub Fins are slightly worse.

- Curve movers include Thames Water (up to 19bps wider), Sartorius (3-4bps wider on earnings), General Mills (up to 7bps wider on new supply) and Mizuho (3-4bps tighter).

- SXXP is +0.2% with Utils +1.1% and Energy -1%. Notable €IG movers include Sartorius -10%, CPI +7%, Tele2 +6%, PostNL -6%. EQT AB -6% and ABB +5%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Housing Data & 20Y Supply

Mar-19 10:16

* US Data/Speaker Calendar (prior, estimate). Times in ET

Mar-19 0830 Building permits (1489k, 1496k)

Mar-19 0830 Housing starts (1331k, 1440k)

Mar-19 1130 US Tsy to sell $46B 52-W bills, $75B 42-D CMB

Mar-19 1300 US Tsy to sell $13B 20-Y reopen (912810TZ1)

Mar-19 1600 Total Net TIC Flows ($139.8b, --)

EURIBOR: EURIBOR FIX - 19/03/24

Mar-19 10:16

EURIBOR FIX - EMMI/Bloomberg:

- EUR001W 3.8750 0.0040

- EUR001M 3.8620 0.0070

- EUR003M 3.9350 0.0070

- EUR006M 3.9090 -0.0060

- EUR012M 3.7560 0.0060

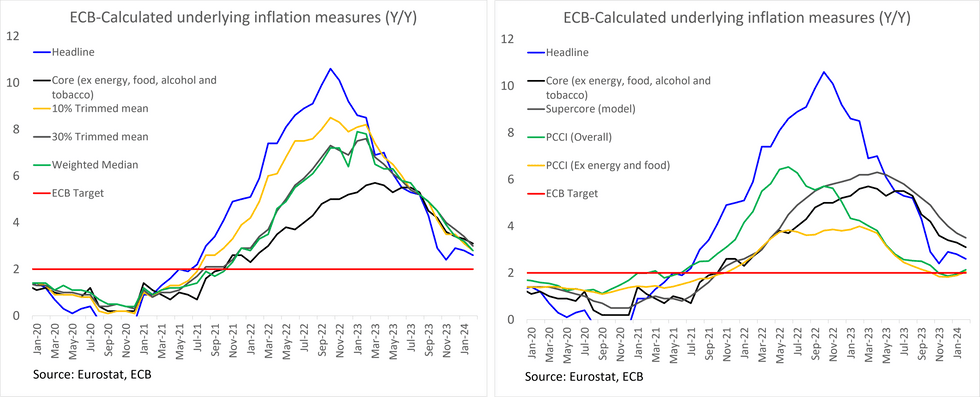

EUROZONE DATA: PCCI Uptick Underscores Need For "More Confidence" In Return To 2%

Mar-19 10:16

The ECB's favoured underlying inflation metric saw a second consecutive uptick in February.

- Overall PCCI (persistent/common component) was 2.13% Y/Y (vs 1.94% prior), while PCCI ex-energy/food was 2.05% Y/Y (vs 1.89% prior).

- It is still too early to tell whether the Jan/Feb PCCI data signifies a reversal in underlying inflation momentum. Prior to the last two upticks, the PCCI ex-energy/food measure declined for 10 consecutive months from a peak of 4.00% Y/Y.

- Nonetheless, the data will be viewed alongside similar rises in core/services inflation momentum in February, underscoring the ECB's need for "more confidence" that inflation is sustainably on its way to the 2% target before easing policy rates.

- This supports the apparent Governing Council consensus eyeing a first cut not before the June meeting, by when significantly more data on price pressures will be available.

- Other ECB-calculated underlying inflation metrics nonetheless decelerated in February, with the 10% trimmed mean and weighted median measured printing below 3% for the first time in 28 and 25 months respectively.

Trending Top

Apr-03 08:04

Apr-02 19:04