EMISSIONS: EU Mid-Day Carbon Summary: EUAs/UKAs Rangebound This Week

Sep-12 11:27

EUAs/UKAs Dec25 are on track for a 0.29% weekly loss and 0.23% weekly gains, remaining rangebound as most gains were erased by Thursday’s sharp decline. EUAs/UKAs Dec25 are edging higher today, supported by gains in EU gas, with TTF rising amid ongoing supply disruption risks.

- EUA DEC 25 up 0.21% at 75.7 EUR/t CO2e

- UKA DEC 25 up 0.38% at 56.2 GBP/t CO2e

- TTF Gas OCT 25 up 0.1% at 32.34 EUR/MWh

- NBP Gas OCT 25 up 0.2% at 79.39 GBp/therm

- Estoxx 50 down 0.3% at 5372.26

- FTSE 100 SEP 25 up 0.4% at 9343.5

- The latest Germany ETS CAP3 auction cleared at €75.02/ton CO2e, down 0.56% compared with the previous Germany auction at €75.44/ton CO2e according to EEX.

- EUA Auction Calendar Week Ahead (Calendar Week 38) - A total of 20.2mn EUAs will be auctioned next week, with 5 auction sessions will be held. The latest EU ETS auction cleared at €75.02/ton CO2e, down -0.56% w/w, above the 10, 50 and 100-day averages.

- EUA Sep25 is seeing balanced positioning as traders weigh modest downside risk amid rising implied volatility and widened volatility skew. The put/call ratio is marginally above parity at 1.01, while the delta call-put volatility skew widened to -1.26, suggesting downside protection has become relatively more expensive.

- TTF front month is steady today but near its low for the week after falling back from a high of €33.44/MWh on Sep.10. Seasonal maintenance in Norway is set against strong wind forecasts next week amid ongoing Russia sanctions uncertainty.

- Lead MEPs from the European People’s Party (EPP) proposed allowing EU member states to use limited international carbon offsets in EU ETS from 2031, according to the leak amendments proposals.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

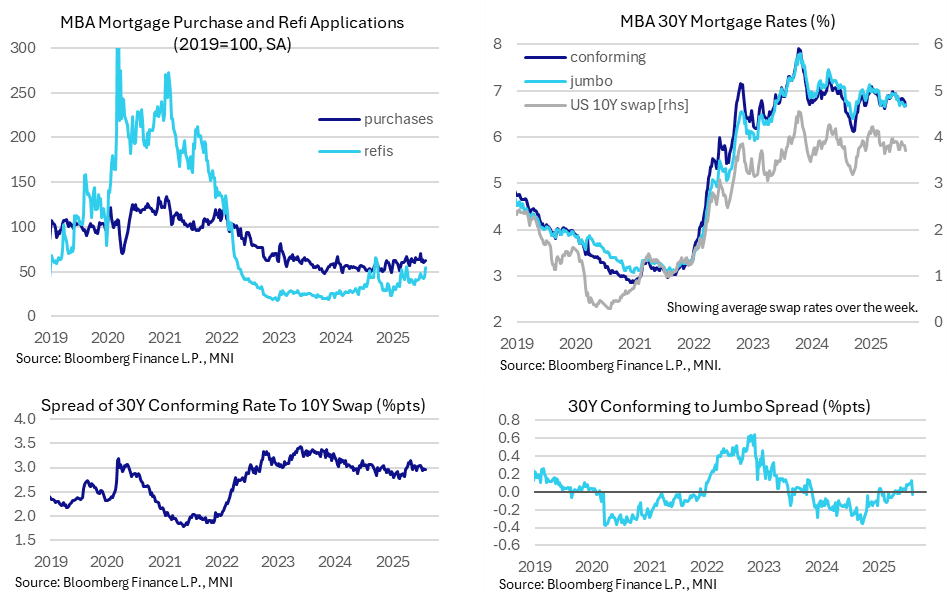

US DATA: Refis Lead An Uptick In Mortgage Applications

Aug-13 11:14

MBA mortgage applications increased to recent highs last week on the back of a rise in volatile refinance applications. Overall levels remains subdued however and new purchase applications continue to point an anemic trend for housing activity.

- MBA composite mortgage applications increased 10.9% sa last week after trending sideways in recent weeks, for their highest since single weeks in July and April and before that Sep 2024.

- It was however driven by a 23% increase in refis after 5.2% as new purchase applications once again saw relative underperformance with just a 1.4% increase after 1.5%.

- Comparison with 2019 averages: composite applications at 59.5%, new purchases at 62% and refis at 55%.

- These refis are reacting to a recent decline in mortgage rates, with the 30Y conforming rate falling 10bps to 6.67% after a 6bp decline the week prior. It leaves the conforming rate at its lowest since early April.

- 30Y mortgage rate to 10Y swap rate spreads remain at the low end of the 300 +/- 5bp range mostly seen since reciprocal tariffs were first detailed in early April, still wider than the 285bp averaged in Q1.

- Within the mortgage rate details, 30Y jumbo mortgage rates saw a relative correction as they increased 5bps to 6.70%. It saw the regular-jumbo spread slide from +12bp (highest since Oct 2023) to -3bp (lowest since mid-April), tentatively ending what had been a sign of some relative loosening in conditions or perhaps borrowers with higher FICO scores.

MNI: US MBA: MARKET COMPOSITE +10.9% SA THRU AUG 08 WK

Aug-13 11:00

- MNI: US MBA: MARKET COMPOSITE +10.9% SA THRU AUG 08 WK

US TSYS: Back Close To Post-CPI Highs, Fedspeak and Trump Watched

Aug-13 10:54

- Treasuries have steadily firmed throughout London hours as they push back towards post-CPI highs, reversing the EGB-led post-data retracement that was hard to square away at the time.

- Treasuries underperform EGBs but outperform Gilts.

- Today sees focus on further FOMC reaction to yesterday’s CPI release whilst Trump headlines can as always have an impact, especially with such a light data calendar today.

- Trump makes an announcement at The Kennedy Center at 1115ET, which we believe should be focused on announcing Honors recipients but we’ll monitor for any surprises.

- Cash yields are 2.5-4bp lower, with the front end lagging declines.

- The modest flattening sees curves ease away from post-CPI steeps. That includes 5s30s at 105.4bps (-0.4bp) after yesterday’s 107.6bps came close to ytd highs of 108.5bps.

- TYU5 has lifted to 112-02 (+ 08) at typing but remains within yesterday’s CPI-induced range of 111-19+ to 112-06. Cumulative volumes are higher than recent overnight sessions but still limited at 250k.

- The contracts hold its ground from a technical perspective, with resistance at 112-15+ (Aug 4/5 high depending on timezone) and support at 110-10+ (Jul 24 low).

- Data: MBA mortgage applications (0700ET).

- Fedspeak: Barkin (0800ET), Goolsbee (1300ET) and Bostic (1330ET) – see STIR bullet

- Bill issuance: US Tsy to sell $65B 17-W bills (1130ET)

- Politics: Trump visits The Kennedy Center and makes announcement (1115ET), Trump signs executive orders (1600ET)