EMISSIONS: EU Issues Guidance on Social Climate Fund Ahead of ETS 2 Launch

Oct-09 15:39

The European Commission has issued guidance to member states on implementing the Social Climate Fund (SCF) ahead of EU ETS2, it said.

- The SCF, worth up to €87bn including national co-financing, aims to mitigate the social impact of carbon pricing on vulnerable households, transport users, and micro-enterprises.

- Member states are instructed to submit Social Climate Plans detailing how revenues from ETS II will be used to support income, energy efficiency, and cleaner transport measures.

- The guidance is intended to ensure that carbon pricing under ETS 2 is implemented fairly and protects the most affected groups.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

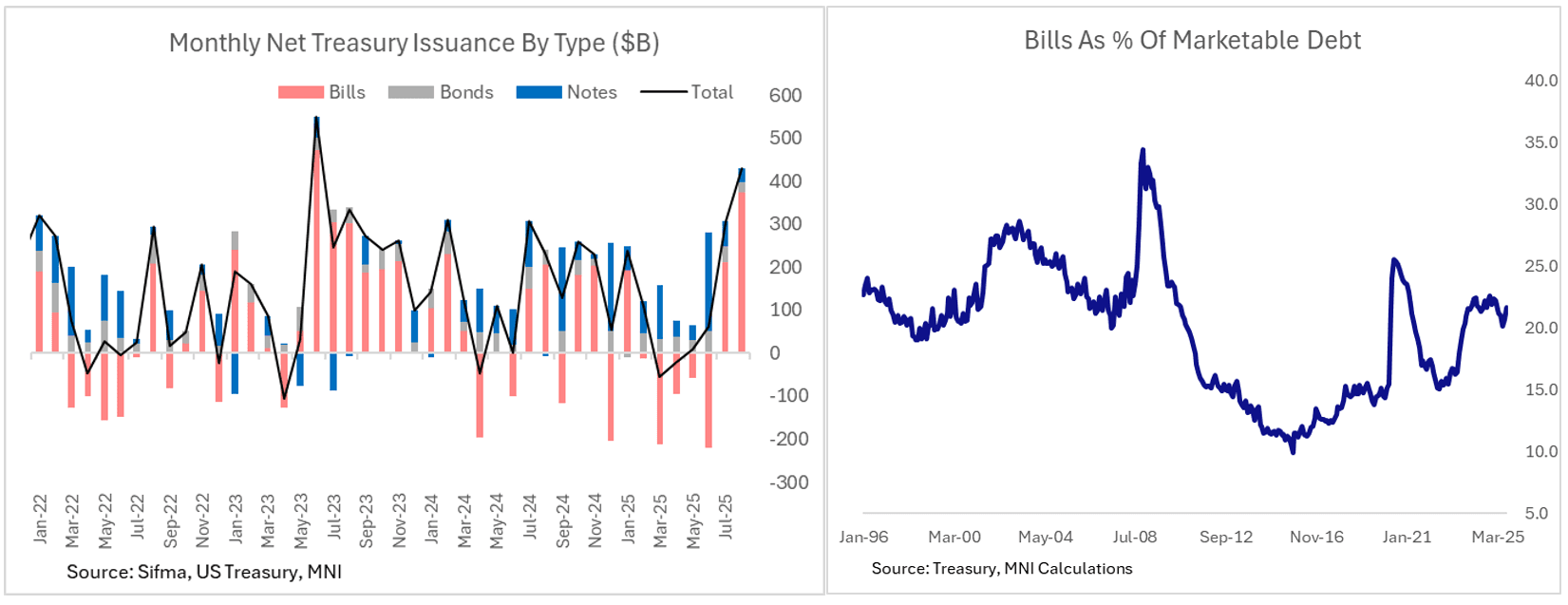

US TSYS/SUPPLY: Issuance Deep Dive: Bills Take Center Stage (1/2)

Sep-09 15:37

Ahead of the first Treasury auction of the month, our latest UST Issuance Deep Dive out Monday (link) recaps August's supply and looks forward to September.

- Supply in the refunding month of August wasn’t entirely smooth, opening with tails in the 3-/10-/30Y auctions and concluding with a pair of tails for the 5Y and 7Y sales. Of 7 nominal auctions, two traded through with the other five tailing, with some of these the weakest sales in a year. We recap August’s auctions in the next note.

- That said, coupon auctions have taken something of a back seat, as shifts in issuance the last couple of months have been dominated by bills in the wake of the debt limit increase in early July.

- Of total net issuance of $739B in July and August, $585B was in bills, basically reversing the $596B negative net bill issuance in February through June under the debt limit.

August is likely to be the high watermark in terms of net bill issuance this year ($373B), but recently-increased bill sizes are set to remain elevated through the first half of September, with Treasury still around $250B shy of its targeted $850B cash balance by end-month. However, net issuance will tail off in starting in the second half of the month, amid large cash management bill paydowns, a mid-month tax date, and smaller auction sizes. - Of course, nominal Treasury auction sizes haven’t been upsized since the May-Jul 2024 quarter, and current expectations are for no change until well into 2026. For the time being, bills will continue to take up the slack. They currently make up around 22% of marketable debt, not far from the longer-term 22.4% historical average, and with most expectations being that there is continued market appetite for more.

US STOCKS: Narrowly Mixed, Lithium Miners Underperforming

Sep-09 15:26

- Stocks trade mixed, fluctuating in narrow ranges early Tuesday after sharply lower (more negative) than expected BLS payrolls annual revision. Near-term data risk is also keeping traders sidelined ahead of CPI and PPI scheduled Wednesday and Thursday.

- Currently, the DJIA trades up 97.2 points (0.21%) at 45611.61, S&P E-Minis down 4.5 points (-0.07%) at 6501.5, Nasdaq down 19.4 points (-0.1%) at 21779.68.

- Materials and Industrials sector shares underperformed in the first half: reports over Chinese lithium miner extending output weighing on Albemarle Corp -11.26%, Freeport-McMoRan -5.10%, Sherwin-Williams -3.12% and Steel Dynamics -2.40%.

- THe Industrials sector weighed by: Builders FirstSource -4.63%, Lennox International -4.21%, Carrier Global -3.95% and A O Smith -3.18%.

- On the positive side, Energy and Communication Services shares led gainers in the first half, a rebound in crude prices (WTI +1.14 at 63.40) helping oil and gas shares: Valero Energy +3.21%, Phillips 66 +2.66%, Marathon Petroleum +2.58% and ConocoPhillips +2.33%.

- Meanwhile, AT&T +1.87%, Paramount Skydance +1.32%, Alphabet +1.30% and Meta Platforms +1.12% buoyed the Communication Services sector in the first half.

US TSYS: Extending Lows

Sep-09 15:07

- Treasuries are extending lows at the moment, no particular headline or Block driver as many ply the sidelines ahead of CPI/PPI data next two sessions.

- Currently, the Dec'25 10Y trades -10 at 113-07.5 (yld 4.0856 +.0458) -- Initial firm support to watch is 112-11+, the 20-day EMA.

- Curves bear flattening: 2s10s -0.971 at 54.171, 5s30s -0.249 at 112.703.

- US$ gaining, BBG index BBDXY currently +1.51 at 1200.06 vs. 1196.69 post data low.