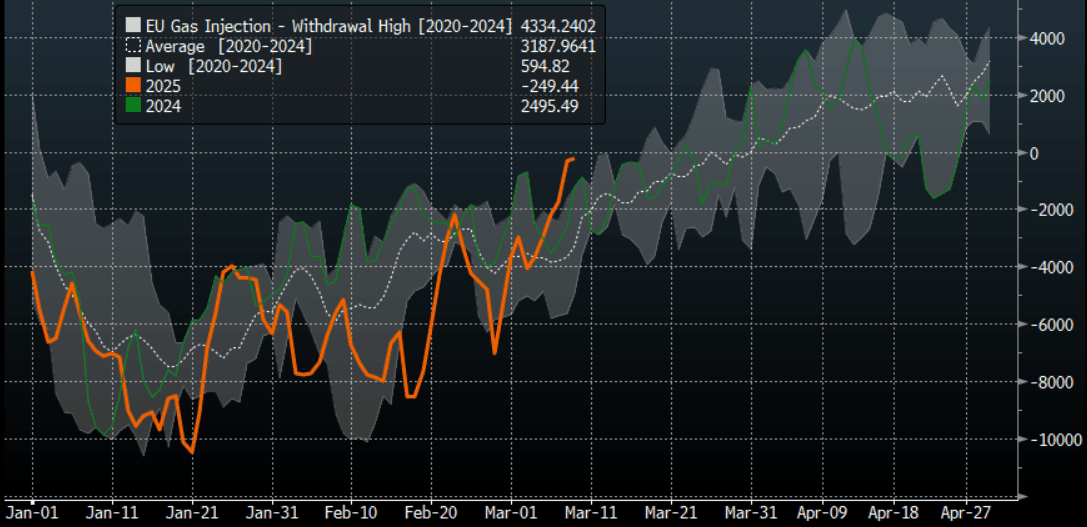

NATGAS: EU Gas Storage Withdrawal Rates Fall Towards Zero

GIE data shows EU gas storage withdrawal rates falling so far this month down to just above zero and well below seasonal normal levels amid mild weather across NW Europe in recent days.

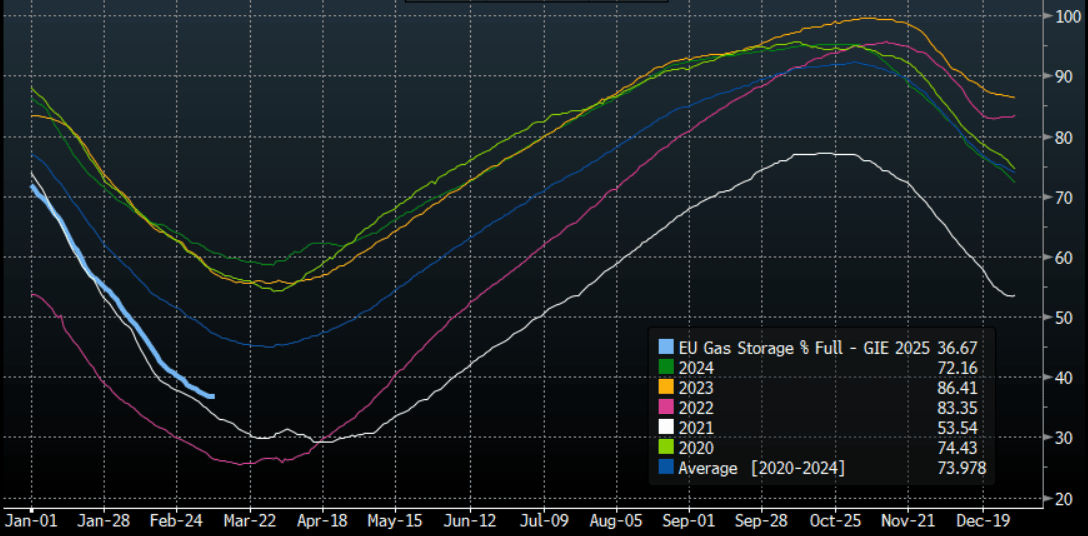

- European gas stores were at 36.67% full on Mar. 9, according to GIE, compared to the previous five year average of 47.1%.

- Temperatures in NW Europe are forecast below normal this week and likely to boost heating demand, but warmer weather is expected to return into next week and through the second week of the forecast.

- The net withdrawal rate in the week to Mar. 9 fell to 40% below normal at 2,175GWh/d from 25.5% above normal at 4,379GWh/d the previous week. Withdrawals dropped to the lowest since Nov. 2 at 249GWh/d.

- Based on the withdrawal rates from the last ten years from now until the end of March the EU storage level would fall to an average of 34.08% of capacity at the end of the season with a range between 31.2% and 36.9%.

- Storage in Germany is at 80.4Wh (32.1% full), Italy at 95.5TWh (47.7%), Netherlands at 35.7TWh (24.8%), France at 30.3TWh (22.5%) and Austria at 48.0TWh (47.3%).

- TTF APR 25 up 0.2% at 41.3€/MWh

- TTF SUM 25 up 0.2% at 41.3€/MWh

- TTF WIN 25 up 0.2% at 39.9€/MWh

Source: Bloomberg / GIE

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (H5) Resistance Remains Intact

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.665/851 - High Feb 5 / High Dec 11

- PRICE: 95.575 @ 16:37 GMT Feb 7

- SUP 1: 95.275 - Low Nov 14 (cont) and a key support

- SUP 2: 94.477 - 1.000 proj of the Dec 11 - 23 - 31 price swing

- SUP 3: 94.495 - 1.0% 10-dma envelope

The Aussie 10-yr futures contract continues to trade below the Dec 11 high of 95.851. A stronger bearish theme would expose 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish theme. For bulls, a confirmed reversal and a breach of 95.851, the Dec 11 high, would instead reinstate a bull cycle and refocus attention on resistance at 96.207, a Fibonacci retracement point.

FED: Gov Kugler: "Prudent" To Hold Rates "For Some Time"

Gov Kugler (permanent voter, leans dovish) said Friday that rates were likely to be held for "some time" - making her the latest FOMC participant to express little impetus for a cut in the near-term.

- "The cautious and the prudent step is to hold the federal funds rate where it is for some time, given that combination of factors, given that the economy is solid, given the fact that we haven't achieved our 2% target, and given the fact that we may have uncertainties and other factors that may be pushing up inflation or maybe reducing output and growth into the future."

- "We reduced our policy rate 100 basis points through December, but the recent progress on inflation has been slow and uneven, and inflation remains elevated. There is also considerable uncertainty about the economic effects of proposals of new policies." She noted in a Q&A that inflation has recently "firmed a little bit."

- She noted that the January jobs report is "consistent with a healthy labor market that is neither weakening nor showing signs of overheating,"

FED: Federal Reserve "Earnings" Briefly Go Positive, But Hole Is Still Large

The Federal Reserve posted positive net earnings in the week to Feb 5, the first time it has done so since September 2022. The $0.4B uptick compares with an average of negative $1.3B over the preceding 6 months.

- Technically, this was a less negative "deferred asset". When the Fed "earns" money on its asset holdings after netting out expenses, it remits this money to the Treasury. With the Fed posting negative earnings for the past 2+ years, it is falling in to deeper and deeper cumulative negative earnings, a "deferred asset" which means that until the figure goes back into a positive balance, no remittances are made to Treasury.

- The "deferred asset" is currently $220.8B.

- The variability of earnings is due to the relationship between rates paid on Fed liabilities versus those paid on its assets.

- The post-GFC rise in the balance sheet saw ZIRP policy and a large set of Treasury and MBS holdings, meaning Fed remittances to the Treasury rose from 0.2% of GDP and 1.3% of government receipts in 2007 to 0.6% and 3.4%, respectively, in 2015, per St Louis Fed calculations. The 2015-18 tightening cycle saw a pullback in remittances, with about $900B remitted to the Treasury over the course of the 2011-20 period.

- The pandemic balance sheet expansion and return to ZIRP saw remittances pick up strongly again, but they have since pulled back. The 52-week average of weekly remittances has shifted, from showing about $10B in monthly "losses" in late 2023/early 2024, to around $6B on a monthly basis now.

- This reflects first the inversion of the yield curve amid the Fed's tightening cycle, and the slow normalizing of the curve since then.

- Unless the Fed easing goes much further, the Fed is unlikely to transmit cash to Treasury for some time.