EMISSIONS: EU End-Of-Day Carbon Summary: EUAs Track Weekly Losses, UKAs Rise

{EUEUAs Dec25 are trending lower today and are on track for marginal weekly losses of around 0.16%, with open interest falling to its lowest level since early July, suggesting a balanced exit by both long and short holders. UKAs Dec25 are trending lower today but remain on track for weekly gains of around 1.6%, following strong gains yesterday after Northern Ireland politicians requested updates on EU CBAM mitigation and EU-UK ETS linkage, setting a 10-day deadline.

- EUA DEC 25 down 1.14% at 80.43 EUR/t CO2e

- UKA DEC 25 down 0.57% at 57.9 GBP/t CO2e

- TTF Gas DEC 25 down 3.2% at 30.175 EUR/MWh

- NBP Gas DEC 25 down 3.8% at 78.4 GBp/therm

- Estoxx 50 down 1.1% at 5507.1

- The latest Germany ETS CAP3 auction cleared at €80.47/ton CO2e, down 0.47% compared with the previous Germany auction at €80.85/ton CO2e according to EEX.

- EUA Dec25 options implied volatility fell to 22.45% on 20 November, while the put/call volatility skew tightened to -0.53% from -0.89% on 16 October, signalling modestly eased downside perception. However, put open interest rose 22% and the put/call OI ratio rose to 0.94 from 0.76, reflecting continued downside hedging demand.

- UKA Dec25 options implied volatility as of 20 Nov was at 35.62%, remaining stable from the level at early November when the price hit the highest level since June 2023. Call and put open interest remained at a similar level, while the call-put volatility skew widened, signalling stable demand for downside protection.

- TTF front month had fallen to its lowest since May 2024 under pressure from news of a Ukraine / Russia peace plan and gradual warming temperatures forecast through next week.

- Norway’s Energy Minister Terje Aasland said that Norway is developing a national mechanism to price carbon removal and reaffirmed the country’s support on carbon removals integration in the EU ETS, he said during the EU-Norway Energy Conference.

- Brazilian Cop presidency has released a new draft COP30 decision text that removes all references to developing a global plan to transition away from fossil fuels, despite strong opposition from supporting nations, according to Reuters.

- ORLEN announced at COP30 that it has joined the taskforce on Nature-related Financial Disclosures (TNFD) initiative, becoming one of the first Polish companies to implement the framework, it said.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: EGBS-GILTS CASH CLOSE: Soft UK CPI Provides The Latest Boost To Gilts

Gilts easily outperformed peers Wednesday.

- The UK September CPI report came in softer than expectations, triggering a sizeable bull steepening of the Gilt curve as a further 25bp BoE cut by year-end became priced as more likely than not (closing at about 70% priced vs closer to 40% at Tuesday's close).

- The inflation data built upon other recent dovish developments in the UK including on the labor market data and public sector finance fronts.

- In contrast, EGBs gained slightly but were relatively stable following the UK CPI release.

- For the day, the German curve bear steepened slightly, with the UK's closing bull steeper.

- Periphery/semi-core EGB spreads tightened modestly.

- The highlight for the remainder of the week remains Friday's flash October PMIs, with US CPI that day also in focus.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.1bps at 1.909%, 5-Yr is up 0.5bps at 2.16%, 10-Yr is up 1.1bps at 2.563%, and 30-Yr is up 1.9bps at 3.147%.

- UK: The 2-Yr yield is down 9.1bps at 3.767%, 5-Yr is down 7.2bps at 3.872%, 10-Yr is down 6.1bps at 4.417%, and 30-Yr is down 4.5bps at 5.221%.

- Italian BTP spread down 0.7bps at 78.5bps / French OAT down 0.3bps at 78.9bps

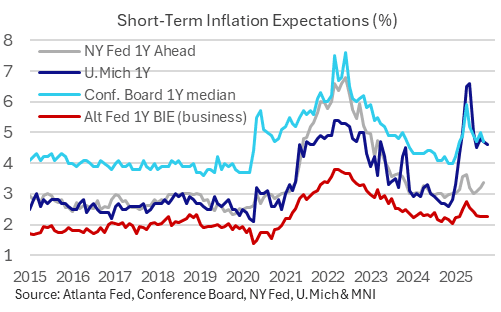

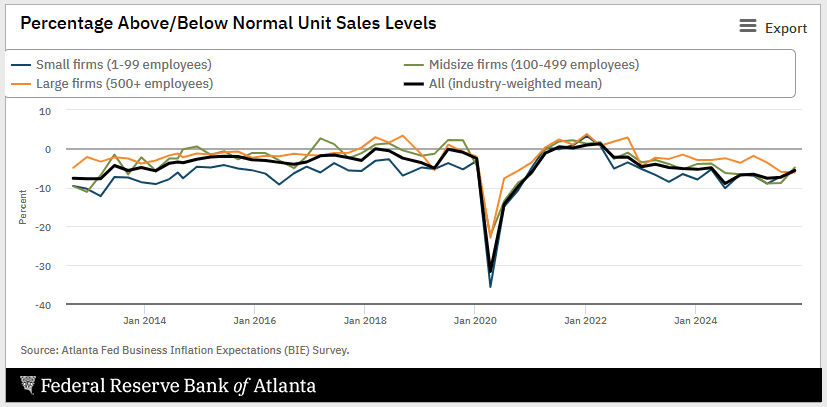

US DATA: Firms’ Unit Cost Expectations Extend Plateau – Atlanta Fed

The Atlanta Fed’s Business Inflation Expectations survey saw 1Y ahead expectations keep to a narrow range, having pared but not fully reversed the tariff-driven increase. Unit sale comparisons to “normal” levels were less pessimistic than recent quarters.

- 1Y ahead inflation expectations from the regular monthly survey, defined as the mean expected change in unit costs, was essentially unchanged in October at 2.27% after two months at 2.26% and before that 2.29% in July.

- It consolidates an easing from a recent peak of 2.76% in April but remains a little above the 2.04% seen in December or the 1.94% averaged in 2019.

- A separate quarterly question showed a slight relative improvement in firms’ unit sales levels, interestingly led by medium and small firms whereas large firms reported their largest decline in unit sales relative to “normal” since July 2020.

- We say a relative improvement as the average industry-weighted response saw sales being -5.5% below “normal”, its least negative since Apr 2024. The chart below shows a persistent bias to negative readings here, even if they were smaller (-2% averaged in the three years ahead of the pandemic).

ITALY AUCTION RESULTS: Day 3 books for the Oct-32 BTP Valore Total E3.3bln

- Day 3 books for the Oct-32 BTP Valore (ISIN: IT0005672016) totalled E3.3bln. Total books now stand at E13.0bln.

- This will be the fifth BTP Valore issued (but the first of 2025) and have the longest maturity to date. Since launching in 2023, BTP Valore volumes have ranged from E11.2-18.3bln with maturities ranging from 4-6 years.

- The last BTP Valore issued in May 2024 (maturity May 2030) saw day 3 books total E2.1bln, and cumulative books after three days total E8.7bln. Cumulative books for the Feb 2024 Valore issue (maturity March 2030) were E14.7bln

- So far in 2025 there have been two Italian retail offerings: the 9-year BTP Piu in February for E14.9bln and the 7- year BTP Italian in May with a retail takeup of E8.8bln.

- Books for the Oct-32 Valore opened on Monday, and will close at 1300CET on Friday (October 24). The guaranteed minimum coupon rates will be 2.60% for years 1-3, 3.10% for years 4-5 and 4.00% for years 6-7.