OIL PRODUCTS: EU Diesel Imports Gain on Month

Feb-21 13:57

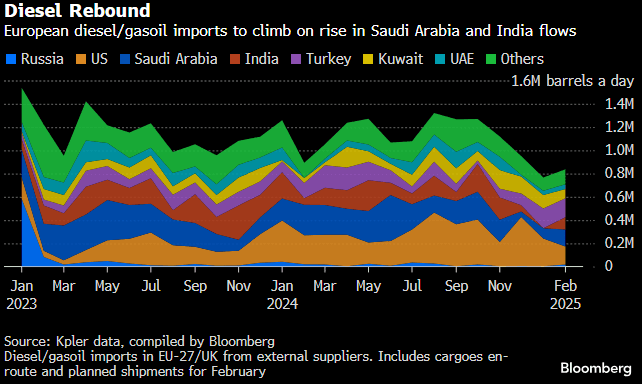

European diesel imports are on track to rebound this month from the multi-year low seen in January, Bloomberg said.

- This comes as a boost in shipments from Saudi Arabia and India have offset a plunge in US arrivals.

- Diesel arrivals into the EU and UK from other regions are expected to be about 837k b/d, Kpler said.

- While some shipments are in transit, it will be a rise of around 9% on the month.

- Europe’s diesel markets are showing signs of tightness due to supply pressures, with the region sensitive to any drop in shipments from the US and the East amid an inability to take Russian barrels.

- Stronger pricing in Europe, fuelled by rising seasonal demand and concerns over refinery closures and outages, is pulling additional cargoes, Kpler analyst George Shaw said.

- Saudi shipments reached a three-month high while flows from India also made a comeback after no flows in Jan.

- US exports have been curbed by stronger domestic demand amid cold snaps.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US REDBOOK: JAN STORE SALES +4.2% V YR AGO MO

Jan-22 13:55

- MNI: US REDBOOK: JAN STORE SALES +4.2% V YR AGO MO

- US REDBOOK: STORE SALES +4.5% WK ENDED JAN 18 V YR AGO WK

STIR: SOFR Option Update, Early Call Adds

Jan-22 13:53

- +5,000 SFRN5 94.87/95.25 put spds, 4.5 vs. 95.95/0.10%

- +3,000 SFRM5 95.62/95.75 put spds, 3.75 vs. 95.895/0.10%

- +5,000 0QN5 94.87/95.25 put spds, 4.5 vs. 95.99/0.10%

- +7,000 SFRU5 96.06/96.31 call spds 7.25 ref 95.98

- +4,000 0QM5 96.31/96.56 call spds vs. SFRM5 96.00/96.25 call spds 1.5 net flattener

- +2,500 2QM5 97.00/SFRM5 96.56 call spd, 0.5 flattener

CANADA: CAD Assets Look Through Further Climb In Y/Y Cost Pressures

Jan-22 13:44

- The industrial product and raw materials price report didn’t have a discernible impact on Canadian asset prices although it nevertheless shows a further acceleration in cost pressures in Y/Y terms.

- BoC-dated OIS has ~21bp of cuts priced for next Wednesday’s BoC decision.

- Not linked to the data, USDCAD has since stepped higher to session highs of 1.4370 on the back of a leg higher in the BBDXY index. It remains within particularly wide recent ranges (key support at 1.4261 from Jan 20 low vs resistance at 1.4516 from Jan 21 high).

- Details: IPPI was admittedly softer than expected at 0.2% M/M (cons 0.6) after 0.6% M/M in Nov and 1.2% in Oct, although IPPI ex-petroleum has seen a more consistent recent trend with 0.4% M/M in Dec after 0.5% in Nov and 1.0% in Oct.

- That leaves IPPI ex-petroleum inflation at 5.1% Y/Y (fastest since Nov 2022) whilst raw materials inflation stands at 9.1% Y/Y or 12.1% Y/Y ex-petroleum (fastest since May 2022).

Related bullets

Related by topic

Gasoil

Marine Oil

Oil Positioning (del)

OPEC

Freight

Jet Fuel

Gasoline

Fuel Oil

Diesel

Oil Options

Energy Data

European Union

UK