US STOCKS: Equities Roundup: Bouncing Off Four Week Lows

Jan-21 16:28

- Stocks rebounded after falling to new 4 week lows this morning after Pres Trump said he would not use force to secure a "piece of ice" - meaning Greenland as he orated at length at the World Economic Forum in Davos this morning.

- Nevertheless, Denmark officials said the US challenge over Greenland sovereignty "is still there" while European Parliament formally suspended the trade deal process (Turnberry Deal) after Trump's Greenland threats. Geopolitical risk remains fluid.

- Currently, the DJIA trades up 428.44 points (0.88%) at 48914.64, S&P E-Mini Futures up 67.5 points (0.99%) at 6896.75, Nasdaq up 260 points (1.1%) at 23212.94.

- A mix of Information Technology, Energy and Financials sector shares led advances in the first half: Intel Corp +10.33%, Teledyne +8.53, Advanced Micro Devices +8.01%, Western Digital +7.81%, Citizens Financial Group +6.35%, Micron Technology +6.29%, Generac Holdings +6.10%, Sandisk Corp +5.19%, ON Semiconductor +4.83%, Invesco +4.62%, Texas Pacific Land Corp +4.51% and Devon Energy +4.38%.

- Another standout was Moderna, surging +9.14% on upgrades and positive headlines on it’s cancer vaccine.

- Conversely, Consumer Staples and Utilities underperformed in the first half: Kraft Heinz Co -5.20%, Philip Morris -1.94%, Keurig Dr Pepper -1.82% and Hershey Co -1.78% buoyed Staples while Sempra -3.06%, Consolidated Edison -1.30%, FirstEnergy Corp -0.87% and American Electric Power -0.76% weighed on the Utilities sector.

- Reminder, a handful of stocks expected to announce earnings after the close include: Prologis Inc, Knight-Swift Transportation, Pinnacle Financial and Kinder Morgan.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Latest Census Bureau Release Dates Imply Pushing Back Of GDP/PCE

Dec-22 16:21

[A correction to the summary, with retail sales set for Jan 14 and not the Jan 21 initially mentioned]

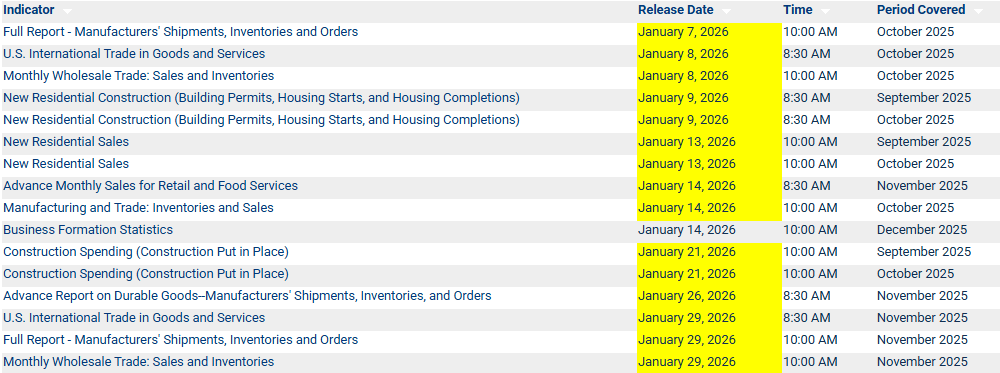

The Census Bureau has announced the next schedule for a raft of data releases, with the highlight being November retail sales set for Jan 14 in a combination of release dates that will push back potential timing for GDP/PCE updates. We had thought PPI (Jan 14)/import prices (Jan 15) might be the stumbling block for a November PCE report, but with retail sales now also a clear limiting factor in the middle of the month.

Highlights of single month updates:

- Retail sales for November to be released on Jan 14, still circa one month late for no improvement relative to the delay of the October report

- Advance durable goods report for November to be released on Jan 26 before the full factory orders report on Jan 29

- International trade in goods & services for Oct (Jan 8) and Nov (Jan 29)

Two-month updates for housing-related data in September and October:

- Housing starts/building permits rescheduled for Jan 9

- New home sales rescheduled for Jan 13

- Construction spending rescheduled for Jan 21

FED: US TSY 13W AUCTION: NON-COMP BIDS $1.768 BLN FROM $86.000 BLN TOTAL

Dec-22 16:15

- US TSY 13W AUCTION: NON-COMP BIDS $1.768 BLN FROM $86.000 BLN TOTAL

FED: US TSY 26W AUCTION: NON-COMP BIDS $1.417 BLN FROM $77.000 BLN TOTAL

Dec-22 16:15

- US TSY 26W AUCTION: NON-COMP BIDS $1.417 BLN FROM $77.000 BLN TOTAL