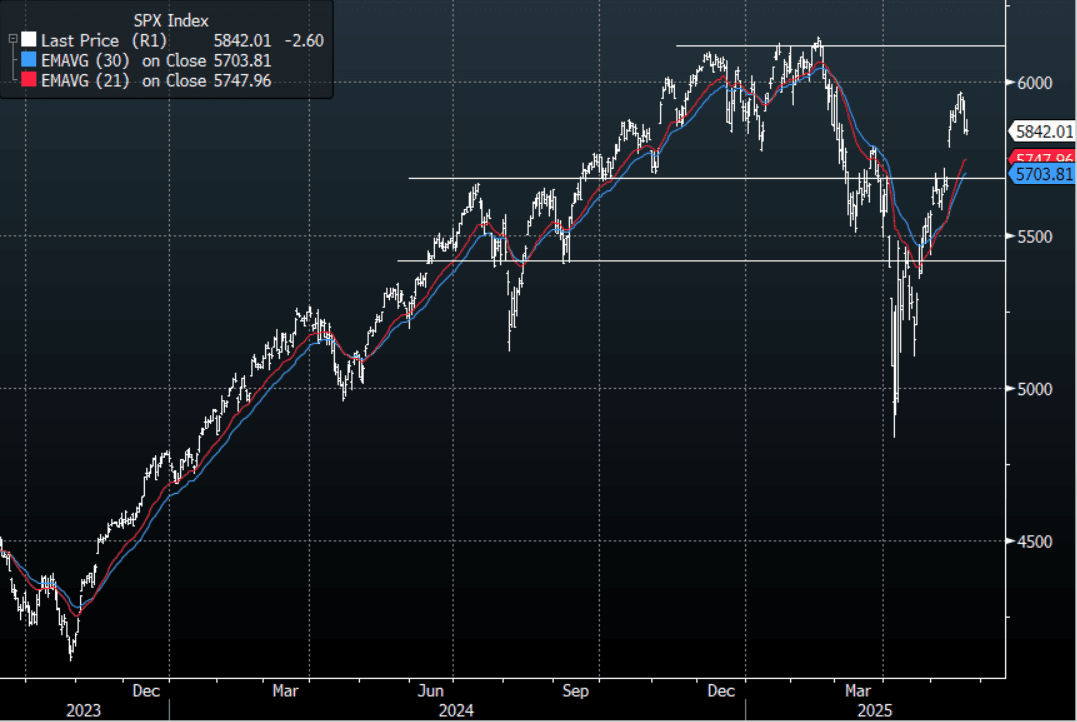

US STOCKS: Ends Flat Overnight, The Pullback Could Have More To Go

The ESM5 Overnight range was 5828.75 - 5895.00, Asia is currently trading around 5862. A quiet open for stocks this morning, overnight has seen some paring back of positions in the short USD and short US Bond trades into the weekend.

- MNI US: House Passes GOP Megabill In Major Win For Speaker Johnson And Trump - The House of Representatives has passed the GOP tax and spending bill in a 215-214 vote, with two Republicans voting 'no'. The bill’s passage is a major win for House Speaker Mike Johnson (R-LA) and President Donald Trump, who have consistently outperformed expectations in Congress. The new revised ‘Big Beautiful Bill’ includes a raft of sweeteners for conservatives. It accelerates work requirements for Medicaid, kicking them in at the end of 2026, rather than the start of 2029.

- Bloomberg - “High long-bond yields are bad for stocks, but what may be more worrying is the rise in real yields. The drivers of higher real yields are things like expectations for higher government borrowing requirements in the future, and with yet more debt-funded fiscal stimulus working its way through Congress, that’s likely to keep pushing real yields higher.

- “BYD beat Tesla in Europe EV sales for the first time in April, vaulting the Chinese automaker into the top 10 brands. Registrations jumped 169% from a year earlier while Tesla’s plunged 49%, Jato Dynamics said.’(BBG)

In the short-term the move higher in global yields particularly in the long-end is starting to matter, providing headwinds to stocks that had already lost their momentum. This pullback feels like it has more go in the short-term, looking for demand to materialize once more back towards the 5600/5700 area.

Fig 1: SPX Daily Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: USD/CNH Back Sub 7.3000, Trump States China Final Tariff To Be Lower

USD/CNH tracks under 7.3000 in early Wednesday dealings, up around 0.25% in CNH terms versus end Tuesday levels in NY. Headlines crossed from US President Trump earlier that the final tariff on China wouldn't be at 145%. Broader USD sentiment is firmer, with yen off 0.80% against the USD, but so far CNH is outperforming these trends.

- Spot USD/CNY finished up at 7.3074 on Tuesday, while the CNY CFETS basket tracker ended at 95.70, down a further 0.28%. If current early Wednesday trends persist, with CNH outperforming this broader USD rebound, should see higher basket levels though.

- For USD/CNH technicals, not much has changed. Downside focus is likely to rest with the 50-day EMA, near 7.2885. We haven't been able to sustain breaches of this level in recent weeks. Beyond that lies the 100-day EMA near 7.2740. Highs from last week in the pair rest close to 7.3350.

- Trump's remarks that the final tariff on China wouldn't be at 145% followed earlier remarks from US Tsy Secretary on Tuesday, who privately told investors the tariff standoff is unsustainable and he expects de-escalation with China.

- The tariff outlook is likely to remain key for CNH sentiment. Earlier on Tuesday the IMF stated its 2025 growth projections for China were cut to 4%. This didn't take into account the full recent tariff escalation though.

- The local data calendar is empty today.

OIL: Crude Rallies As US Iran Sanctions Increase & Trump Comments On Fed & China

Oil rallied on Tuesday following increased US sanctions on Iran and better risk sentiment and has continued to trade higher in early APAC trading today following comments from President Trump that he wouldn’t replace Fed Chair Powell and that China’s tariffs wouldn’t finish at the current 145%. The US dollar recovered somewhat from Monday’s fall with the USD index up 0.5%.

- WTI rose 1.8% to $63.54/bbl after reaching $64.36, below initial resistance at $64.49. The benchmark is up another 1.1% to $64.34 today but is still down over 9% this month. The bear trigger is at $54.67.

- Brent is up 2.4% to $67.82/bbl following a high of $68.04 but the move above $68.00 was short lived. The benchmark approached initial resistance at $68.14, 17 April high, but fell short. It continues to trade above the April 9 low though maintaining a more positive short-term tone but the rally remains corrective as the oversold position unwinds. Initial support is at $62.00 and the bear trigger at $58.40. It is now down 9.3% in April.

- Bloomberg reported that there was a significant US crude stock drawdown of 4.57mn barrels last week, according to people familiar with the API data. Products continued their decline with gasoline down 2.18mn and distillate 1.64mn suggesting that demand is robust. The official EIA data is out later today.

- Despite ongoing talks between the US and Iran on its nuclear programme, US actions on Tuesday were tougher against the oil producer with President Trump supporting Israel’s stance on Iran and new US sanctions on an Iranian LPG businessmen and his shipping network for allowing oil exports to avoid sanctions. There will also be stricter enforcement.

- Trump is due to travel to Saudi Arabia, Qatar and UAE in May.

JPY: Big Bounce Off 140.00 Area

The range on Tuesday was 139.89 - 141.67, price opened very bid and has raced to print a high of 143.22 so far. A big bounce in US stock futures and then a second leg higher in Asia as Tesla shares rally up to 7% during its earning call as Elon Musk says he is to pull back significantly from DOGE.

- Treasury Secretary Bessent Tuesday privately told investors the tariff standoff is unsustainable and he expects de-escalation with China. Trump added with comments later from the White House stating that final tariffs on China would not be 145%, while also stating he has no intention of firing Fed Chair Powell (which has been a worry for markets in recent weeks).

- (Bloomberg) -- “Nomura Holdings Inc. is telling clients to stay invested through the turmoil that’s pervaded financial markets during the escalating trade tensions. With its $1.8 billion acquisition of an asset management business, the Japanese brokerage is putting its money where its mouth is.”

- Risk has managed a significant bounce and the follow through in Tesla after the close has seen USD/JPY shorts quickly pared back after its failure to sustain a break sub 140.00.

- The consensus view has quickly changed now to a short USD bias, should risk actually manage a decent rally these holdings will be challenged.

- On the day sellers should emerge first up around 143, then more importantly the 145/146 area should once more offer good levels for shorts to reengage.

- CFTC data shows Asset managers continuing to add to JPY longs, while leveraged are only just starting to get long, they will be waiting for a decent bounce to add.

- USD/JPY: upcoming notable strikes, 140.00($1.61b), 145.00($1.38b) Exp Apr 24 NY cut(Source DTCC)

- Data : Jibun Bank Japan Mfg, Services PMI, US S&P Global Services & Manufacturing PMI

Fig 1 : USD/JPY Daily Chart

Source: MNI - Market News/Bloomberg