EUROZONE ISSUANCE: EGB Supply

Belgium, Italy and Germany have all come to the market this week. We pencil in gross nominal issuance of E22.1bln, down from E31.1bln last week.

For more on this week's issuance and a look ahead to next week's supply see the PDF here:

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BTP TECHS: (U3) Uptrend Remains Intact

- RES 4: 118.41 1.00 projection of May 26 - Jun 2 - Jun 8 price swing

- RES 3: 118.18 High Feb 2 (cont)

- RES 2: 118.00 Round number resistance

- RES 1: 117.60 High Jun 26

- PRICE: 116.97 @ Close Jun 27

- SUP 1: 115.89/114.61 20-day EMA / Low Jun 15

- SUP 2: 113.83 Low Jun 8 and key short-term support

- SUP 3: 112.48 Low May 29

- SUP 4: 111.78 Low May 26 and a key support

BTP futures traded to a fresh cycle high on Monday. Price has breached resistance at 117.16, the Jun 16 high and a short-term bull trigger. This reinforces a bullish condition and signals scope for a climb towards the 118.00 handle next. Note that moving average studies remain in a bull mode condition. On the downside, key short-term support has been defined at 114.61, the Jun 15 low. A break would highlight a potential reversal.

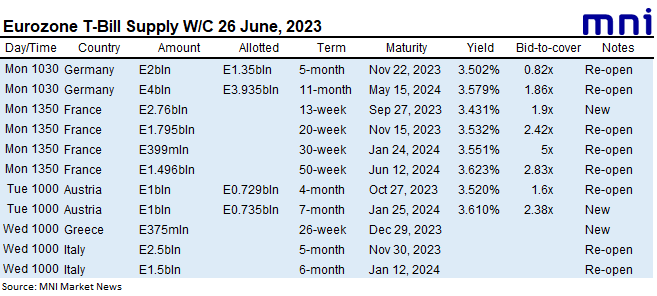

EUROZONE T-BILL ISSUANCE: W/C 26 June, 2023

Greece and Italy both look to sell bills today while Germany, France and Austria have already come to the market this week. We look for issuance at first round operations of E18.8bln, up from last week's E17.0bln

- Greece will come to the market today, with E375mln of the new 26-week Dec 29, 2023 GTB on offer.

- Italy will also come to the market this morning to sell a combined E4.0bln of 5/6-month BOTS: E2.5bln of the 5-month Nov 30, 2023 BOT and E1.5bln of the 5-month Jan 12, 2024 BOT.

For more on future auctions see the full MNI Eurozone/UK T-bill auction calendar.

RIKSBANK: MNI Riksbank Preview - June 2023: 25bp hike expected but upside risks

- The big question ahead of this week’s Riksbank meeting is whether there will be another hawkish central bank surprise. Every analyst preview that we have read and every respondent to the SEB investor survey expects a 25bp hike this week to 3.75%.

- We think there is a greater chance of a hawkish surprise than most analysts would suggest despite there having been two dissenters to the 50bp hike at the last meeting in April.

- A step up in the pace of QT is also expected. Most analysts expect an increase in pace from SEK3.5bln/month to somewhere between SEK5-6bln/month, while the median expectation in the SEB investor survey was for a SEK5.75bln/month pace.

- In terms of the rate profile, the median of the analyst previews we have read look for a peak around 3.85-3.90%. However, an increasing number of analysts look for a further 25bp hike in September, in order to keep up to some extent with the ECB and to support the krona.