US TSYS: Early SOFR/Treasury Option Roundup

Better put trade on net coming into the session, if overall volumes remain subdued after the BOE 25bp hike (expected). Focus turns to S&P Global US Services/Composite PMIs at 0945ET, ISMs at 1000ET. Little change in rate hike projections through year end, Sep 20 FOMC is 17% w/ implied rate change of +4.3bp to 5.371%. November cumulative of +9bp at 5.419, December cumulative of 6bp at 5.389%. Fed terminal holding at 5.42% in Nov'23.

- SOFR Options:

- 3,700 SFRZ3 94.00/94.75 put spds vs. 97.00/98.00 call spds

- 12,000 SFRV3 94.50 puts, ref 94.63 to -.625

- 4,000 SFRX3 94.87 calls ref 94.63

- 1,000 2QQ3 96.00/96.18 3x2 put spds ref 96.32

- 2,000 2QQ3 96.00 puts, 2.5 ref 96.33

- Treasury Options:

- Block, 21,000 TYU3 107/108.5 put spds, 11-12 ref 110-13

- 1,250 FVU3 107.25/108.25 call spds ref 106-13.5

- 6,000 TYU3 107/108.5 put spds, 12 ref 110-13

- over 10,500 TYU3 109.5 puts, 31-34 ref 110-12.5 to -11.5

- 1,500 USU3 114/117 put spds ref 120-29

- 1,800 USU3 116/119 put spds ref 121-26

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

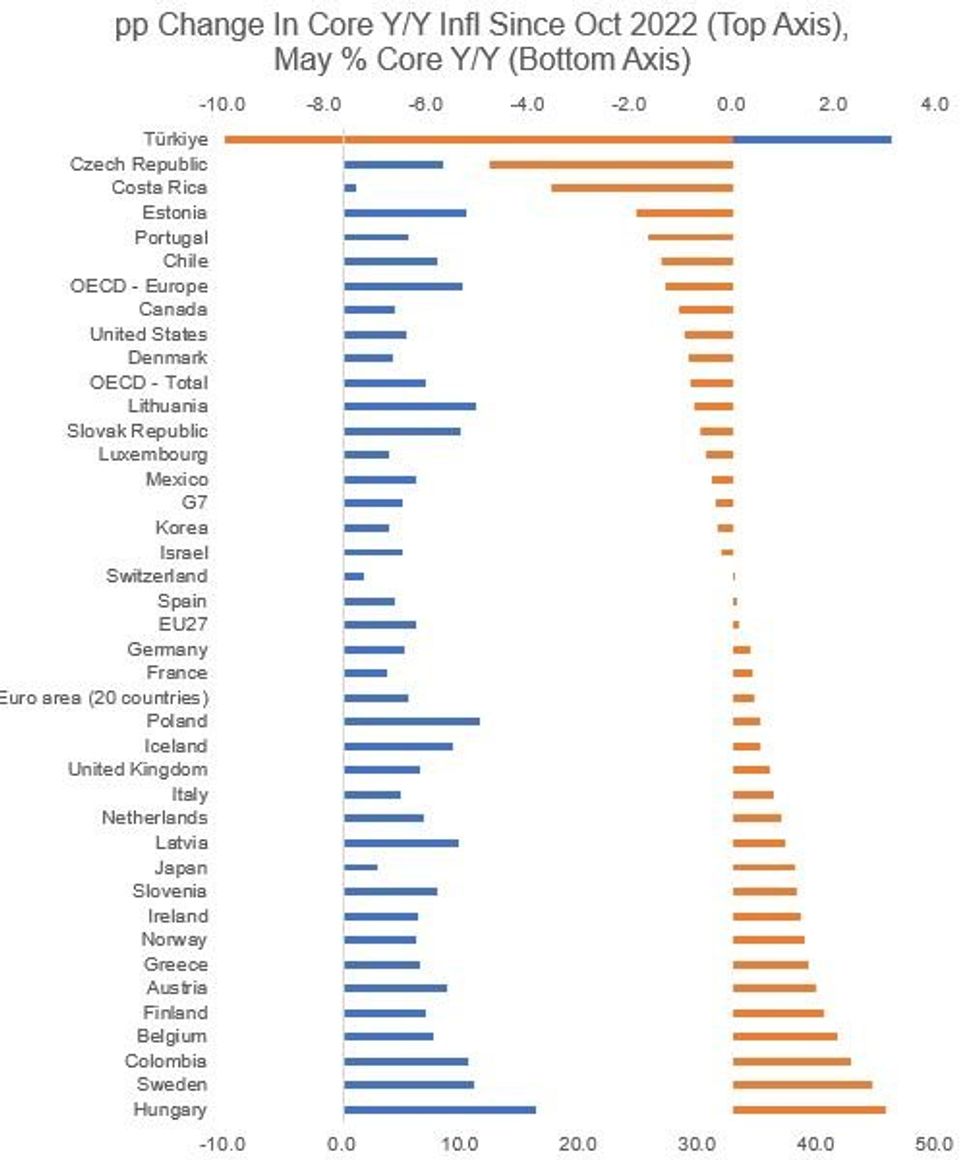

GLOBAL: Divergence In Core Inflation Progress Since Global Peak (2/2)

Since the October 2022 OECD inflation peak, there has been only mixed progress on core inflation, with the US making noticeable strides, and Western Europe lagging.

- The OECD report showed headline inflation declining Y/Y in May in all countries except the Netherlands, Norway, and the UK - but on core a total of 9 countries saw an uptick Y/Y (including Japan, but the UK and Sweden saw the biggest, up 0.3/0.4pp).

- The highest OECD inflation rates in May were observed in Hungary and Turkiye (20+%), with the lowest (<3%) including Denmark, Greece, and Costa Rica.

- On core: Turkiye and Hungary still lead the pack (46.2% and 16.2% respectively in May), one key divergence being that the former is down the most since the OECD core peak in Oct 2022 (-25pp), while the latter has seen the biggest rise (3pp) in that period. Sweden (+2.7pp), Colombia (+2.3pp), Belgium (+2.0pp), and Finland (+1.8pp) round out the biggest increases in core.

- Switzerland and Costa Rica were the only OECD members registering below 2% core in May (1.6% and 1.1% respectively).

- Looking at the G7, all countries came in below the OECD CPI core inflation aggregate of 6.9% in April, with the closest call being the UK which was the only G7 country to see core inflation tick up in May (to 6.5%) vs April.

- With flash June data in hand we know the eurozone core Y/Y figure ticked higher slightly last month, but that's largely due to base effects from June 2022. EZ core momentum is slowing but perhaps not quickly enough for comfort.

Source: OECD, MNI Calculations

Source: OECD, MNI Calculations

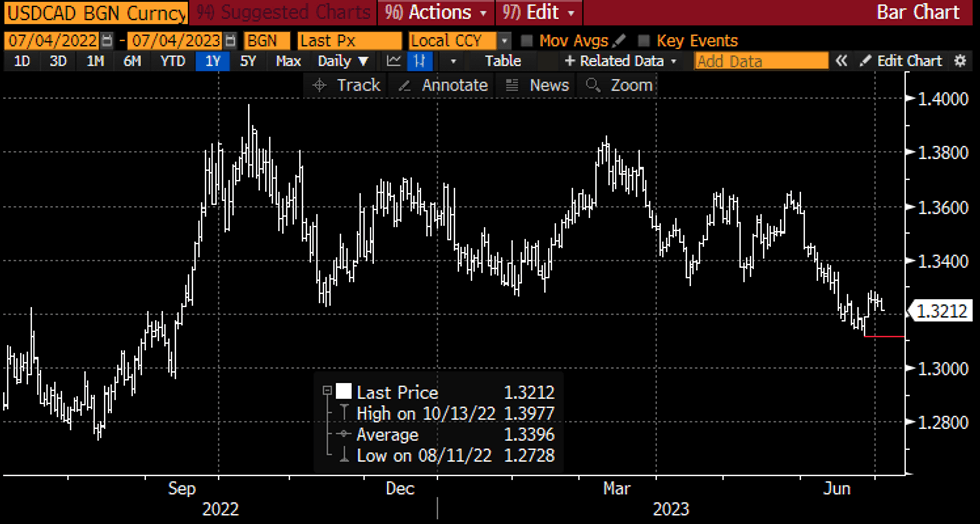

CANADA: USDCAD Resumes Bearish Trend

- USDCAD pushes new session lows with a latest 1.3212, as CAD lags NOK and NZD but generally outperforms other majors with WTI gaining.

- Holiday-thinned trade risks reading too much into it, but the -0.3% dip on the day supports the view that the prior rise was corrective going against a bearish trend.

- It approaches support at 1.3190 (Jun 28 low), with a stronger run at it potentially opening the key 1.3117 (Jun 27 low).

- The mfg PMI lands at 0930ET today but the next key domestic data release is the employment report on Friday, with focus in the meantime on the US with the FOMC minutes and the usual data releases building to payrolls.

Source: Bloomberg

Source: Bloomberg

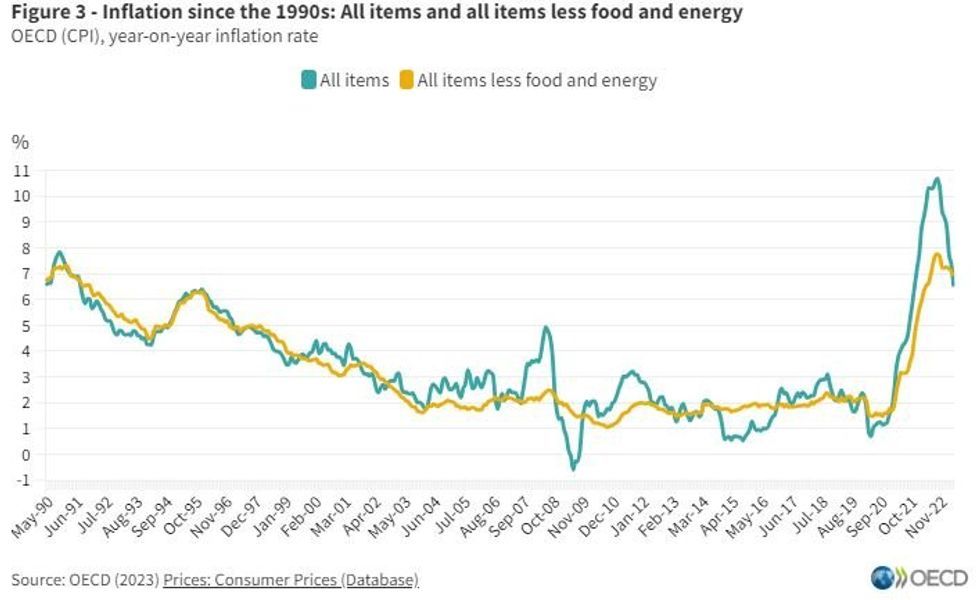

GLOBAL: OECD Inflation Slowing, But Core Progress Very Limited (1/2)

The OECD's aggregate inflation indices for May were published today - while that's a bit of a delay vs some of the prelim readings we've gotten for June already, they offer a helpful like-for-like comparison across geographies and show a post-2021 low for headline OECD CPI at 6.5% Y/Y (vs 7.4% in April).

- But that headline decline was largely energy driven (that inflation category was -5.1% Y/Y, and negative in 16 OECD countries with major exceptions including Italy and others which posted +10% Y/Y).

- Food inflation slowed to 11.0% Y/Y from 12.1%.

- That meant aggregate OECD core inflation progress was more stubborn than for headline, at 6.9% Y/Y (just 0.2pp lower than April), with services prices rising 5.7% Y/Y (0.3pp below April's reading).

- That's below the OECD core peak of 7.8% Y/Y in Oct 2022 (when headline was 10.7%), but significantly above the pre-pandemic period in which core inflation struggled to move above 2%.

- It's difficult to gauge the "momentum" of core disinflation vs Y/Y base effects as the OECD only publishes seasonally-adjusted monthly data for a few countries. But 0.9pp of annual inflation progress over 7 months from the peak is a disinflation rate of just over 0.1pp a month. At that pace it would take years to bring inflation down to even close to pre-pandemic levels.