US: Donald Trump's Approval Dips Further Amid Iran War Fallout

After a relatively static period, President Donald Trump's approval rating has slumped to a new low,...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURUSD TECHS: Pierces Resistance At The 20-Day EMA

- RES 4: 1.1825 61.8% retracement of the Jan 27 - Mar 13 bear leg

- RES 3: 1.1796 High Mar 2

- RES 2: 1.1746 50.0% retracement of the Jan 27 - Mar 13 bear leg

- RES 1: 1.1682 50-day EMA

- PRICE: 1.1600 @ 17:09 GMT Mar 23

- SUP 1: 1.1411 Low Mar 13 and 16 and the bear trigger

- SUP 2: 1.1373 1.764 proj of the Jan 27 - Feb 6 - 10 price swing

- SUP 3: 1.1340 38.2% retracement of the Feb 3 ‘25 - Jan 27 bull cycle

- SUP 4: 1.1299 2.000 proj of the Jan 27 - Feb 6 - 10 price swing

Monday’s volatile price action in EURUSD has resulted in a test of resistance at the 20-day EMA, at 1.1611. Short-term gains are considered corrective, however, a clear break of the average would expose resistance at the 50-day EMA, at 1.1682. A clear breach of both averages is required to signal a stronger reversal. On the downside, the bear trigger is 1.141 the Mar 13 and 16 low. A breach of this support would resume the downtrend.

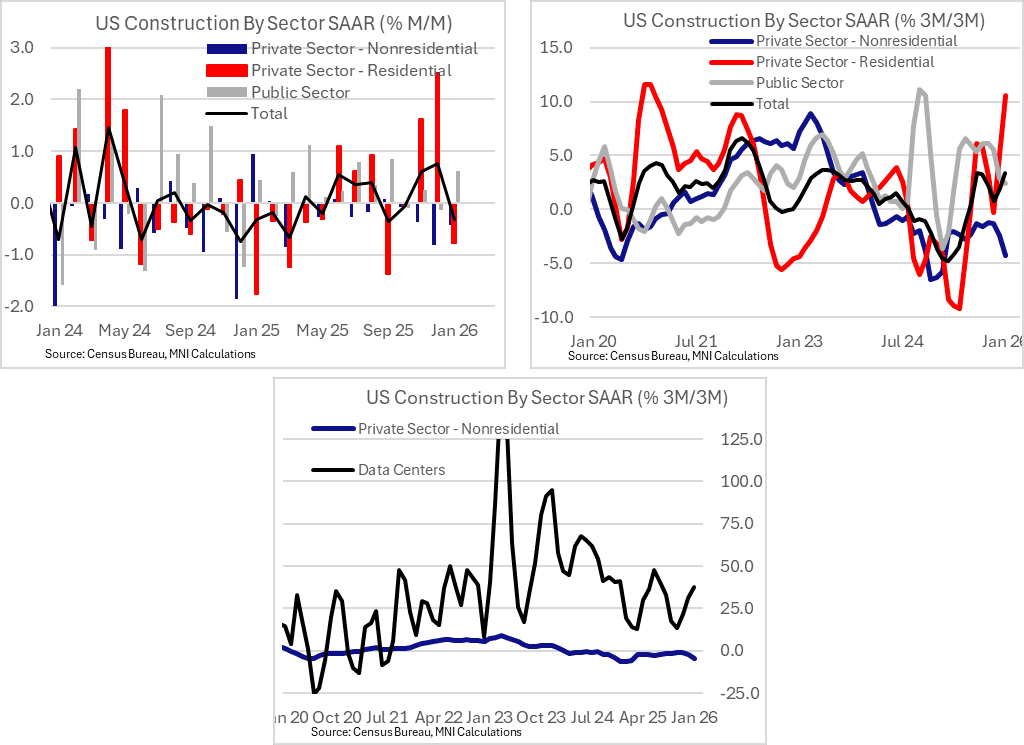

US DATA: Construction Spending Dips In January, Led By Housing/Manufacturing

Construction spending unexpectedly fell in January (-0.3% M/M, +0.1% consensus, all on a nominal, seasonally-adjusted annual rate basis) for the first time since October, and by the most since September. This largely reflected a reversion in private sector construction spending growth from an unusually strong 1.0% M/M in December, a 20-month high now that it has been upwardly revised from 0.5%. Overall, residential construction looked solid at the turn of the year in value terms, at least, though forward looking indicators including homebuilders confidence and building permitting point to weakness ahead.

- For the moment though, the upward revision to prior in overall construction spending was driven by residential construction spending, originally reported at 1.5% in December but now up 2.5%. In January this category, which is about 43% of total construction spending, saw a pullback of 0.8% (led by multifamily construction).

- Residential has still grown 10.6% on a 3M/3M annualized basis after two strong months, even though this looks like a temporary 3-month bump. We know that housing starts jumped in January from previously-released data, but permits pulled back sharply.

- Far weaker in any case is nonresidential spending for which momentum appears to be slowing further: 3M/3M annualized growth fell to -4.3%, slowest in 11 months, after 4 consecutive contractions; manufacturing construction (10% of overall construction) is now down 25% 3M/3M ann., a new series worst and bringing the level down to March 2023 levels.

- Indeed illustrating the degree to which manufacturing is weighing, nonresidential ex-manufacturing momentum is actually decent, up 5.0% 3M/3M ann.

- Data Centers weren't to blame: they saw 37% 3M/3M annualized growth after a 2.3% M/M growth performance in January, and are now soundly picking up momentum after a brief lull late last year.

- It will be a while before we get the next data: Feb/Mar construction spending reports are combined and set for release on May 7.

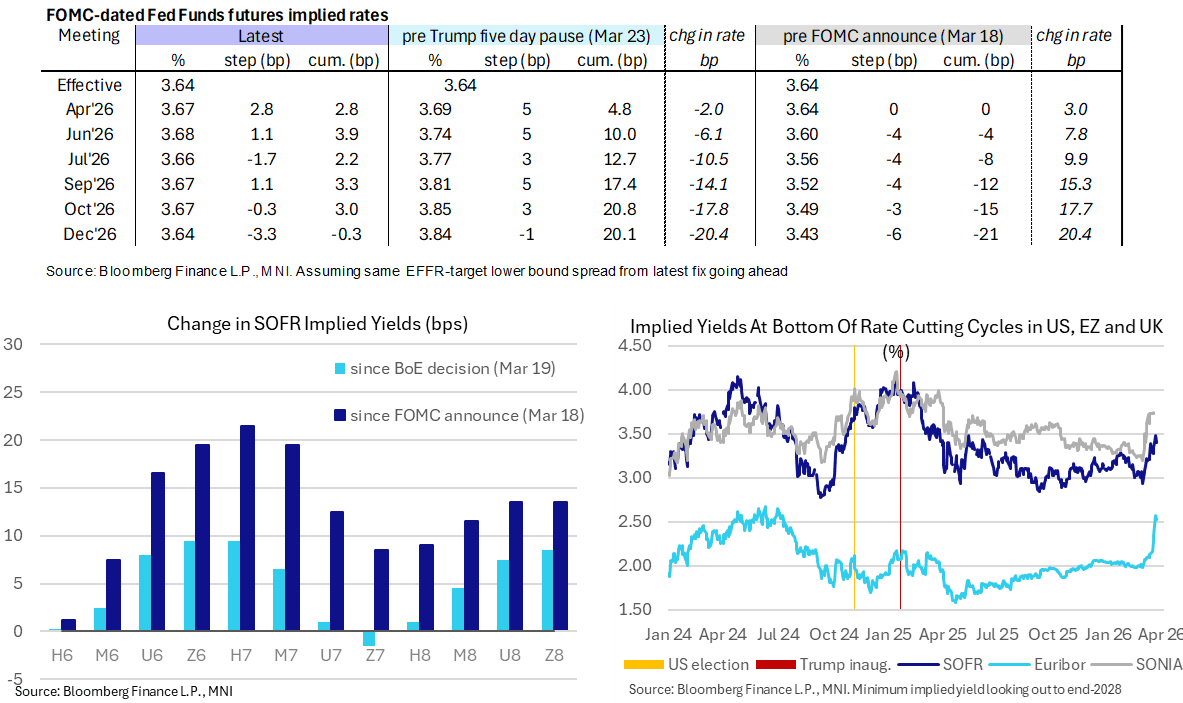

STIR: US Rates Back Near Earlier Highs With Only Mild Hiking Bias Seen In 2026

- US rates have pushed higher over the past hour to push a little closer to earlier highs compared to a more muted recent uptick for equities futures.

- Both see large gains for day in what have been extremely wide ranges as US and Iranian sources continue to contradict the status of negotiations.

- Fed Funds futures point to a cumulative 4bp of hikes in 2026 (peaking in June) vs 23bp for the Oct meeting before Trump’s initial Truth Social post this morning via 0bp in the interim.

- FF cumulative hikes from 3.64% effective: 3bp Apr, 4bp Jun, 2bp Jul, 3.5bp Sep, 3bp Oct, -0.5bp Dec.

- SOFR futures see the largest gains in the SFRH7 (+0.095), an area where inflation fear-driven losses have been most concentrated since the start of the US-Israel-Iran conflict.

- That said, the terminal implied yield of 3.395% (Z7, -8.5bp) still sees a sizeable decline today to fully reverse Friday’s push higher. It had earlier cleared 3.50% for highs since early Apr 2025.